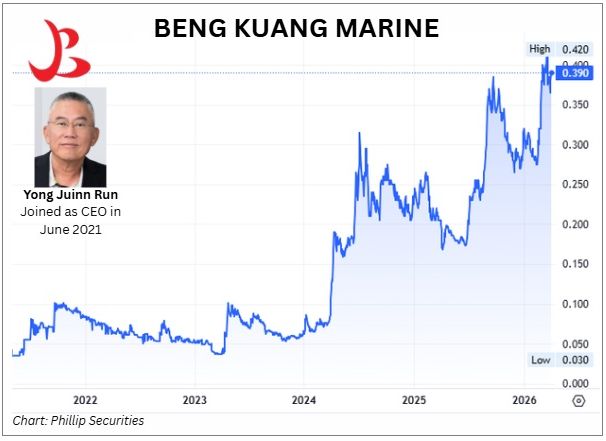

• Beng Kuang Marine has gained about 100% (from 20 cents to 40 cents) in the past year, proving itself a survivor of the 2014 oil slump alongside names like Nam Cheong and Marco Polo Marine. • Its losses deepened around 2021–2022, at which point ex‑banker Yong Jiunn Run stepped in as CEO in June 2021. The company exited ship chartering, divested its Singapore shipyard and began pivoting to an asset‑light model centered on infrastructure engineering, FPSO/FSO module works and recurring asset‑integrity services.  Debt has been significantly reduced through asset sales, cost optimization and tighter project selection. • Also central to its turnaround was its long-standing 51% controlling stake in Asian Sealand Offshore & Marine (ASOM). Now, Beng Kuang is progressing to acquire the rest of ASOM which offers a comprehensive range of services to FPSOs, FSOs and other offshore assets. It usually repairs and maintains them, and also does inspection services. Read an analyst report on this move ..... |

Excerpts from Lim & Tan Research report

Analysts: Nicholas Yon & Chan En Jie

Ever since CEO Yong Jiunn Run took the helm at Beng Kuang Marine in 2021, he has turned a loss-making, leveraged shipyard operator into a profitable, asset-light O&M provider.

As part of this shift, BKM has proposed acquiring the remaining 49% stake in ASOM, which would allow the group to fully consolidate ASOM’s recurring earnings and cash flows. We thus initiate coverage on Beng Kuang Marine with a BUY recommendation and a target price of S$0.535, based on 12x blended FY26F/FY27F P/E. |

|||||

BKM is set to deliver NPAT of $12.1mln and S$18.1mln in FY26F and FY27F respectively.

This valuation approach represents a small discount to its peers and also reflects the timing of earnings consolidation, as full contribution from ASOM will only be reflected from 2HFY26F onwards.

We have the following investment thesis:

1. FPSO servicing remains key in the O&G value chain, as ageing vessels must meet international standards to stay operational, amidst tight FPSO supply.

Middle East conflict is also a net positive in the medium term.

2. Post-acquisition, BKM will fully consolidate ASOM’s earnings, with valuations dropping from FY25 PE of 15.5x to 10.2x and 6.9x in FY26F and FY27F.

On a like for like FY25 EPS of c.2.6 cents would have risen to c.4.8 cents pro-forma (+c.84%yoy).

3. The acquisition is both earnings and valuation accretive.

We see no teething issues given BKM’s initial stake, while the structure of the transaction is sound and current ASOM mgmt. remains incentivised to continue delivering for BKM.

4. Investors can now better understand ASOM’s business, which was previously a black box. This added visibility could support a valuation re-rating as BKM is now essentially a recurring off shore service provider.

ASOM provides predictable, steady and recurring income backed by cash flows.

5. Continued value unlocking by CEO Yong, including growth in the Deck Equipment and Shipbuilding under the IE segment, which secured $14.2mln and $7.8mln of contracts in FY25.  Nicholas Yon, analyst6. BKM operates in structural infrastructure maintenance, not contracting, and thus benefits from rising energy security investments that drive marine compliance, inspection, and corrosion prevention. Nicholas Yon, analyst6. BKM operates in structural infrastructure maintenance, not contracting, and thus benefits from rising energy security investments that drive marine compliance, inspection, and corrosion prevention.7. BKM’s net cash position (32% of mkt cap) provides financial flexibility to pursue asset-backed marine investments through joint ventures, creating additional earnings streams beyond its core engineering services. |

→ See the Lim & Tan report here.

→ See the Lim & Tan report here.

Also: BENG KUANG MARINE: From Crisis to Comeback: Ex-banker joins as CEO and turns company around hard

→