|

Lum Chang Creations (LCC) has moved swiftly from a strong IPO debut on the SGX Catalist board to a Mainboard listing soon. Following a robust financial performance in 1HFY2026 (ended Dec 2025), reports from three brokers highlight a positive outlook for the company, driven by its asset-light model, exceptional margin expansions, and a solid project pipeline. |

Recommendations, Target Prices, and Valuations

|

Feature |

CGS Int'l |

DBS Bank |

RHB |

|

|

Add (Reiterated) |

Not Rated |

Buy (Initiation) |

|

Target Price / Fair Value |

SGD 0.93 (Prev: SGD 0.90) |

SGD 1.07 |

SGD 1.13 |

|

Valuation |

12x P/E Multiple |

13x P/E Multiple |

15x blended P/E |

|

Basis of Valuation |

FY27F Earnings |

FY27F Earnings |

FY26F-27F Earnings |

|

Premium Reason |

Superior profit margins over sector average. |

Structurally higher margins and unique market positioning. |

Specialised skill set, asset-light model, and high growth (31% CAGR). |

CGS International analysts Li Jialin and Lock Mun Yee have reiterated an "Add" recommendation for LCC, raising its target price to SGD0.93 from SGD0.90.

This target is based on a 12x price-to-earnings (P/E) multiple applied to FY27F earnings, which includes a premium over the sector average to reflect LCC’s superior profit margins.

Meanwhile, DBS analysts Ling Lee Keng LING and Ng Jia Hui issued an Equity Explorer report with a fair value of SGD1.07.

DBS derived this valuation by applying a 13x P/E to FY27F earnings.

This 20% premium over the peer group average is justified by LCC’s structurally higher margins and its differentiated market positioning across the refurbishment value chain.

Earnings Forecasts and Margin Expansion

Aanalysts underscore LCC’s stellar profitability.

RHB analyst Alfie Yeo was particularly bullish: "We expect margins to remain consistent going forward, with orderbook to driving 31% earnings growth CAGR projection for FY25-28F. Balance sheet is in net cash of 14 SG cents/share. We like LUCC for its cash generative business, high ROE, margins and good DPS payout."

CGS International revised its FY26F PATMI (Profit After Tax and Minority Interests) estimate upward by 25% to SGD22.6m, and its FY27F estimate by 4% to SGD24.5m.

DBS forecasts similar figures, projecting FY26F net profit at SGD23m and FY27F at SGD26m.

The driving force behind these optimistic forecasts is a significant expansion in margins.

In 1HFY26, LCC's net profit doubled year-over-year to S$11m.

Its PATMI margin expanded by over 9 percentage points to 20.5%.

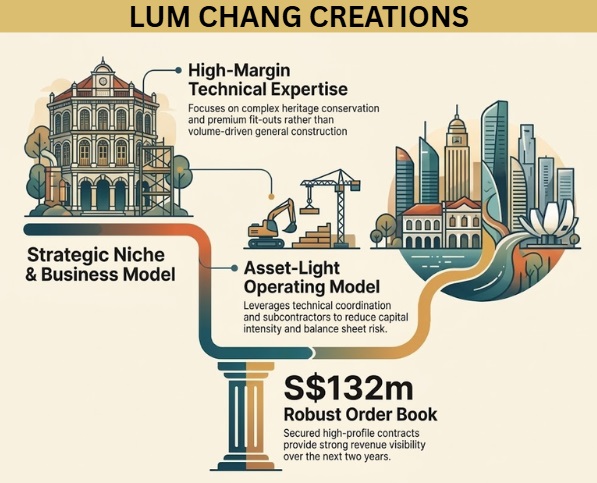

Analysts attribute this to superior cost management, improved resource utilisation, scale efficiencies, and LCC’s asset-light business model, which leverages subcontractors rather than capital-intensive heavy equipment.

Additionally, CGS highlights that LCC's upcoming inclusion in the MSCI Global Micro Cap Singapore Index could enhance trading liquidity, while its strategic expansion into Malaysia presents further upside. |

Risks to the Outlook

Despite the strong catalysts, analysts caution against several headwinds.

Key downside risks include margin pressures from rising labour and material costs, potentially exacerbated by geopolitical risks.

Furthermore, the business remains sensitive to broader construction cycle volatility and unexpected disruptions to ongoing construction works. → See also: LUM CHANG CREATIONS: Gets Post-IPO Surge, What's The Story?

→ See also: LUM CHANG CREATIONS: Gets Post-IPO Surge, What's The Story?