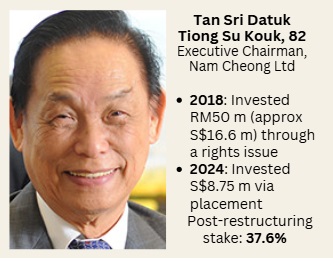

| After 4 unusually long years of negotiations with its creditors, Nam Cheong Limited received a new lease of life in March 2024. (Nam Cheong's Singapore legal counsel has a blog post on how the debt was restructured for the second time, the first having taken place in 2018).  SourceWhile similarly indebted well-known peers have sunk into liquidation, like Ezra and Ezion, one factor likely played a key role in Nam Cheong's survival as a charterer of vessels that support offshore activities of the oil & gas industry in Malaysian waters. SourceWhile similarly indebted well-known peers have sunk into liquidation, like Ezra and Ezion, one factor likely played a key role in Nam Cheong's survival as a charterer of vessels that support offshore activities of the oil & gas industry in Malaysian waters.It was the ability and willingness of its executive chairman to put large amounts of personal funds on the table to signal that he wasn't giving up on the company. Tan Sri Datuk Tiong Su Kouk is 82. He could have, citing his age, closed the book on Singapore-listed Nam Cheong. But he is a self-made, never-say-die entrepreneur based in the Malaysian state of Sarawak. And he has had majority control of Nam Cheong for over 20 years. In fact, far from resting on his laurels, he continues to be executive chairman of another company -- Bursa Malaysia-listed CCK Consolidated that he founded. In the 2018 restructuring plan of Nam Cheong, Datuk Tiong invested RM50 million (approximately S$16.6 million) through a rights issue that provided working capital and partially repaid creditors. His subscription accounted for the majority of the S$22 million in net proceeds of the rights issue.  But subsequently the Covid pandemic and oil slump once again undermined the company's debt repayment capability. But subsequently the Covid pandemic and oil slump once again undermined the company's debt repayment capability.But he would not give up on the company. Under the restructuring plan finalised in 2024, Datuk Tiong's shareholding (along with all other shareholders) was virtually wiped out by a 100-to-1 consolidation. His 2.26 billion shares (direct & deemed interests) shrank to 22.6 million. As part of the 2024 plan, Datuk Tiong invested S$8.75 million through a private placement: He received 125,507,689 Nam Cheong shares at an issue price of 6.97 Singapore cents per share, bringing his total direct & deemed interests to 37.6%. The issue price looks to be an incentive, as it is significantly lower than the 40 Singapore cents at which shares were issued to creditors. |

Nam Cheong's CEO Leong Seng Keat and CFO Chong Chung Fen met with analysts, fund managers and investors last week. Photo: Lily Lu

Nam Cheong's CEO Leong Seng Keat and CFO Chong Chung Fen met with analysts, fund managers and investors last week. Photo: Lily Lu

| Happy days again for offshore support vessel sector |

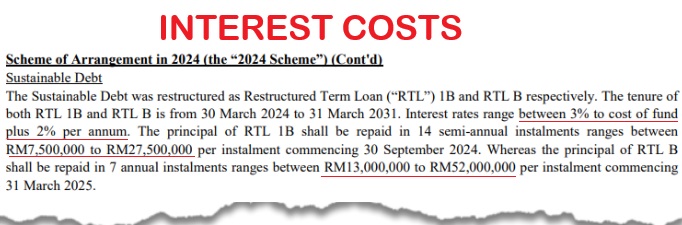

So the repayment terms for the adjusted debt of ~RM500 million, including a 7-year repayment schedule, have been finalised.

Every interested party, including Nam Cheong's management which has an incentive plan, want and hope that the company will ride it out this time.

The question is: How is its business -- which has 32 vessels serving oil majors, including Petronas -- doing? What's the outlook for the sector?

The answers are pretty positive which, on top of Datuk Tiong's confident capital infusion, would have influenced the creditors' agreement to restructure the debt.

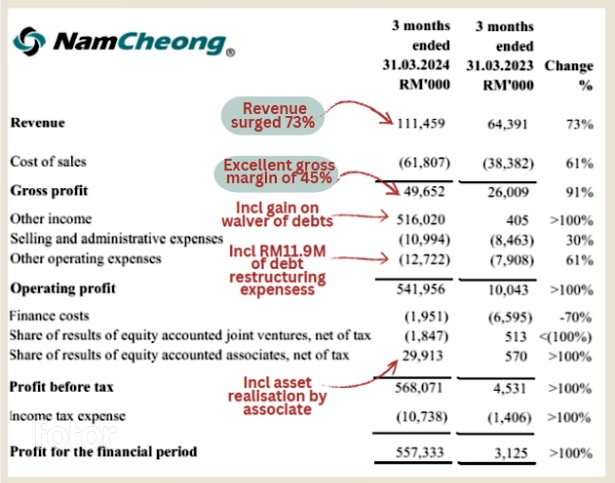

In 1Q2024, Nam Cheong's revenue surged and the gross margin of 45% was excellent (see table below).

Nam Cheong cited improved daily charter rates and higher utilisation of its larger vessels.

"The increasing offshore activities have driven up day rates for offshore support vessels (“OSV”)," it said.

After adjusting for one-offs (highlighted in the table above), the 1Q net profit was approximately RM25 million.

Take note that the 1Q performance was affected by the monsoon season crimping offshore activities. Things typically normalise in 2Q and 3Q before slowing down at year-end.

Thus, a back-of-the-envelope estimate: Considering that Nam Cheong starts paying interest on its outstanding debt from 2Q2024 (see screenshot below), FY24 may see net profit of RM100 million (exclusive of one-off items).

If so, the FY24 PE is about 2-3X.

Compare that to the average of 15 among 10 of its Malaysian-listed peers which are covered by stockbroker Kenanga (table below). Note that many of these companies have other businesses aside from OSVs.

Note that many of these companies have other businesses aside from OSVs.

In the cabotage environment where Malaysian-flagged vessels like Nam Cheong's get priority for domestic contracts, charter rates continue to be bouyant.

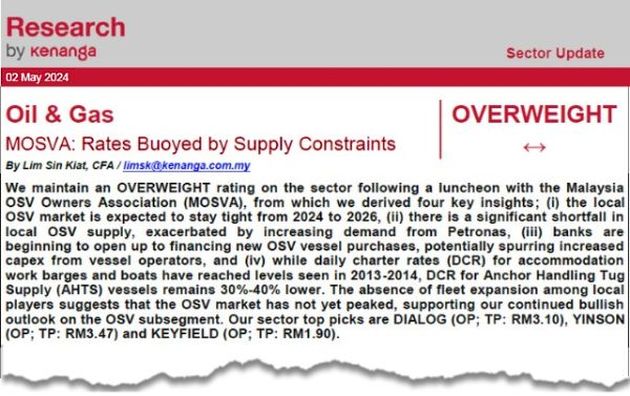

An analyst report dated 2 May 2024 by Kenanga provides insights:

Excerpts from the Kenanga report:

We hosted a luncheon with the Malaysia OSV Owners Association (MOSVA) and the key takeaways are as follows:-

1. The Malaysian OSV market is anticipated to remain tight from 2024 to 2026, with increasing demand from Petronas positioning it as a market favourable to vessel owners in the near to medium-term. Since the peak of the cycle in 2014, many local OSV owners have been in survival mode, primarily due to a drop in DCR (day charter rates) driven by declining Brent crude prices. Since then, MOSVA noted that there has been a noticeable absence of new vessel additions among Malaysian listed players, as the industry focused on deleveraging their balance sheets. Since 2014, local OSV operators have minimized spending on fleet renewals and expansions, keeping the overall Malaysian fleet size similar to what it was nearly a decade ago. This restraint in investment reflects the sector's response to volatile oil prices and lower charter rates.

2. Petronas, to sustain its production levels, requires a minimum of 200 vessels for support. With the expected increase in demand, this number could rise to 300 vessels operating in Malaysian waters in 2024 and onwards. However, the current fleet under the MOSVA totals only 270 vessels, and it's unclear how many of these are currently cold-stacked and potentially not viable for service return. This situation points to a significant shortfall in available OSV capacity, underscoring the tightness of the market and the potential for upward pressure on charter rates. Hence, MOSVA anticipates a robust DCR outlook in the general OSV market in 2024 and 2025, particularly for the locally-flagged vessels. |

See also: NAM CHEONG: Plunged on re-listing in March. But this stock is now up 50% in 2 weeks