| Nam Cheong Ltd, Malaysia’s biggest owner of offshore support vessels (OSVs), has a string of major contract wins to charter out its vessels to oil majors. Let’s break down what’s happening, why it matters, and highlight the fact that from this year, the Singapore-listed company’s profits are looking strong and stable as now it has contracts worth up to RM1.54 billion.  |

| Latest News: Fresh Contracts Worth RM317.1 Million |

Last night (April), Nam Cheong announced it has landed new multi-year contracts to charter out seven Anchor Handling Tug Supply (AHTS) vessels.

These deals are worth up to RM317.1 million and will see the vessels working in Malaysian and Thai waters for up to two years, with options for extensions.

The clients? Leading regional oil majors—so, big names in the industry.

"These wins reflect their trust in our operational excellence as well as our capable and young fleet," said Nam Cheong CEO Leong Seng Keat.

Nam Cheong now has 21 vessels on long-term contracts, making up about 57% of its fleet.

The company’s goal is to get 70% of its fleet locked into long-term deals, which gives it a nice, steady income while still leaving some ships available for short-term jobs that might pay even more if the market heats up.

With Sarawak (where Nam Cheong is based) becoming a bigger player in the oil and gas world, the company is well-placed to grab more opportunities as the region opens up for more offshore exploration, said CEO Leong.

| Flashback: The November 2024 Mega Deal |

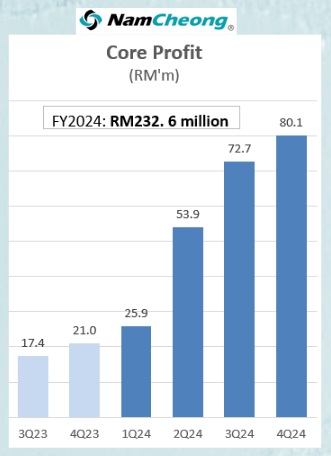

Back in November 2024, the company clinched a massive set of contracts worth up to RM1.22 billion.  Core profit from vessel chartering, excluding "other income and other expenses" and contributions from JVs/associates.

Core profit from vessel chartering, excluding "other income and other expenses" and contributions from JVs/associates.

Ref: NAM CHEONG: Troubled Waters to Smooth Sailing: And the stock trades at just 3X PE and 3X EV/EBITDAThat deal covers 12 vessels—including AHTS, Platform Supply Vessels, Safety Standby Vessels, and Landing Craft—and runs for three years, with options to extend.

These contracts represent about a third of Nam Cheong’s fleet and were awarded by both regional and international oil majors.

The deals kick off in 2025 and gives the company a big boost in revenue visibility for a few years to come.

And there's more opportunity in the offing.

Sarawak is a key oil and gas hub seeking the federal government’s approval to open more offshore areas, particularly off its western coast, for gas exploration, making Nam Cheong’s local presence a major advantage.

| Sustaining Nam Cheong’s Strong Metrics |

Securing these contracts is a game-changer for Nam Cheong’s bottom line.

They will sustain the strong metrics of FY2024:

|

Metric |

FY2024 value |

Notes |

|

Gross margin |

53.1% |

35.5% in FY2023 |

|

Operating Cash Flow |

RM190.2 mn |

Up 682% year-on-year |

|

Free Cash Flow |

RM91.9 mn |

13.3% margin |

|

Total Borrowings |

RM458.4 mn |

Down 56% from FY2023 |

|

Net Gearing Ratio |

0.56x |

Improved post-restructuring |

|

Cash |

RM135.1 mn |

|

|

PE Ratio (core earnings) |

~3x |

Peers average ~10x |

Post-restructuring in early 2024, Nam Cheong's debt has fallen and is scheduled to be repaid over 7 years.

Dividends are not expected as the company rebuilds its balance sheet and prioritises repayment of its debt.

Still, given its low valuation and expected flow of positive quarterly results, a re-rating of its shares that happened in 1Q this year may have room to run.

All of this is happening against a backdrop of a supply-and-demand squeeze in the OSV market:

|

See also: Tariff-Immune: Vessel Supply’s Tight, Charter Rates Look Bright