Excerpts from analysts' reports

OSK-DMG highlights Nam Cheong's entry into lucrative Indonesian charter market

Analysts: Lee Yue Jer & Jason Saw

OSK-DMG highlights Nam Cheong's entry into lucrative Indonesian charter market

Analysts: Lee Yue Jer & Jason Saw

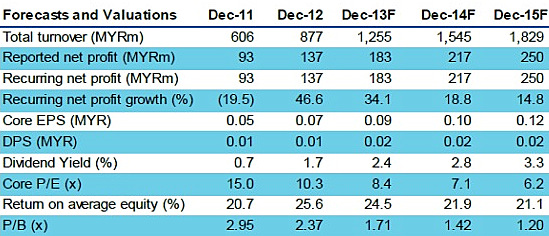

Nam Cheong Limited (NCL) said it has entered into a JV with PT Bahtera Niaga Internasional to own and operate OSVs in the lucrative Indonesian market.

This will boost its high-margin recurring charter income, thus providing a new source of orders and shipbuilding profits. NCL remains one of our Top Picks in the O&G sector, which we have upgraded to OVERWEIGHT.

Maintain BUY, with a higher SGD0.38 TP.

This will boost its high-margin recurring charter income, thus providing a new source of orders and shipbuilding profits. NCL remains one of our Top Picks in the O&G sector, which we have upgraded to OVERWEIGHT.

Maintain BUY, with a higher SGD0.38 TP.

The JV will allow NCL to charter vessels in Indonesia, where the enforcement of cabotage law has led to charter rates spiking up 33% last year.

We calculate that a 5,150bhp anchor handling tug supply (AHTS) vessel in Indonesia today can fetch net margins of 41% net margins.

At 30% equity financing, the ROE on each vessel is 44%.

Recent story: NAM CHEONG: Likely beneficiary of Malaysia’s oil and gas capex plans

We calculate that a 5,150bhp anchor handling tug supply (AHTS) vessel in Indonesia today can fetch net margins of 41% net margins.

At 30% equity financing, the ROE on each vessel is 44%.

Recent story: NAM CHEONG: Likely beneficiary of Malaysia’s oil and gas capex plans

Daiwa keeps target price of $2.01 for Suntec REIT

Analyst: David Lum, CFA

Phase 1 of the Suntec City Mall refurbishment (193,000 sq ft) is completed and 100% leased. It has achieved a passing rent of SGD13.09/sq ft. Phase 2 (380,000 sq ft and scheduled for completion in 4Q13) is about 70% pre-committed (as at 30 June 2013).We met with the management (CEO Yeo See Kiat) of Suntec REIT (Suntec) on 18 September 2013 for an update of the business.

Phase 1 of the Suntec City Mall refurbishment (193,000 sq ft) is completed and 100% leased. It has achieved a passing rent of SGD13.09/sq ft. Phase 2 (380,000 sq ft and scheduled for completion in 4Q13) is about 70% pre-committed (as at 30 June 2013).We met with the management (CEO Yeo See Kiat) of Suntec REIT (Suntec) on 18 September 2013 for an update of the business.

We maintain our Buy (1) rating and DDM-derived target price of SGD2.01.

Analyst: David Lum, CFA

Phase 1 of the Suntec City Mall refurbishment (193,000 sq ft) is completed and 100% leased. It has achieved a passing rent of SGD13.09/sq ft. Phase 2 (380,000 sq ft and scheduled for completion in 4Q13) is about 70% pre-committed (as at 30 June 2013).We met with the management (CEO Yeo See Kiat) of Suntec REIT (Suntec) on 18 September 2013 for an update of the business.We maintain our Buy (1) rating and DDM-derived target price of SGD2.01.

We believe Suntec offers the best value in the S-REIT sector, trading at a 21% discount to book value (as at 30 June).

We believe a positive catalyst could come from upward revisions to DPU forecasts as the market gains more confidence in the tangible benefits (to DPU and NAV) of the Suntec City refurbishment.

A risk to our call could be poor execution in the Suntec City refurbishment, but we believe this risk is receding.

We believe a positive catalyst could come from upward revisions to DPU forecasts as the market gains more confidence in the tangible benefits (to DPU and NAV) of the Suntec City refurbishment.

A risk to our call could be poor execution in the Suntec City refurbishment, but we believe this risk is receding.

■ How we differ. Our DPU forecasts from 2014 are considerably higher than those of the Bloomberg consensus, as the market could be underestimating the resilience of its office assets and the DPU and NAV potential of the refurbishment.