|

Singapore’s construction sector in 2026 finds itself balancing unprecedented public sector demand against unexpected external cost pressures arising from the Iran war. |

| Government will co-share financial burden |

Recognizing the sector-wide pressure, the Building and Construction Authority (BCA) announced a crucial relief measure in April 2026.

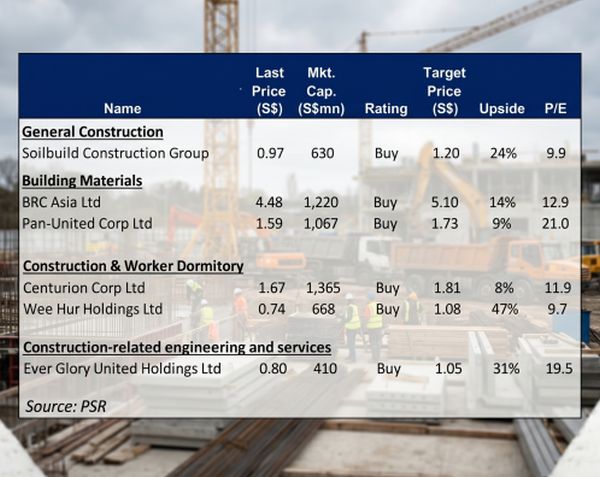

The government will co-share the financial burden by covering 50% of the direct additional costs resulting from diesel and bitumen usage for the period between March 1 and May 31, 2026. Wee Hur has the highest upside potential. "We believe Wee Hur’s 15,744-bed Tuas View Dormitory’s lease could be extended beyond Nov 2026 due to major construction projects’ progress – potentially serving as a share price catalyst."

Wee Hur has the highest upside potential. "We believe Wee Hur’s 15,744-bed Tuas View Dormitory’s lease could be extended beyond Nov 2026 due to major construction projects’ progress – potentially serving as a share price catalyst."

The demand outlook remains bright, effectively buffering the industry.

The BCA projects a massive S$50 billion in contract awards for 2026, which is an impressive 61% higher than the 20-year historical average.

Notable projects slated for the remainder of 2026 include the Changi Airport Terminal 5 development (with a total contract value of S$16–20 billion), the Marina Bay Sands expansion (S$8–10 billion), the Tuas Port Phase 3 expansion (S$2–4 billion), and the new Tengah General and Community Hospital (S$2–3 billion).

The medium-term forecast is equally promising, with the BCA projecting S$39–46 billion in yearly construction demand from 2027 to 2030, a 37% increase over historical averages.

| Relatively insulated |

"We remain OVERWEIGHT on construction-related companies. We believe the Singapore construction sector remains relatively insulated from the Middle East conflict, as labour and raw material supplies remain available." "We remain OVERWEIGHT on construction-related companies. We believe the Singapore construction sector remains relatively insulated from the Middle East conflict, as labour and raw material supplies remain available."-- Ben Yik, analyst |

However, private sector construction demand has softened due to broader market uncertainties—with industry private contracts dropping by 27% year-on-year in the first two months of 2026.

Individual companies are navigating these waters differently based on their operational structures.

For example, building materials players like BRC Asia are expected to face short-term margin impacts, as diesel constitutes roughly 10% of its cost of goods sold, said PhillipCapital.

Conversely, contractors like Soilbuild Construction are less exposed since major ventures like their S$648 million PSA Supply Chain Hub project have already advanced past the diesel-intensive piling stages, said PhillipCapital.

Years ago, several Singapore construction companies chose to list on the HKSE.

Financials are based on reported statements covering the last 12 months. • CTR Holdings (1416.HK): Posted solid growth with TTM revenue at S$248 million and net profit S$11.5 million. • Chuan Holdings (1420.HK): Benefited from strong earthworks demand. |

|||||||||||||||||||||||||||||||||||||

→ See also: At 3.1x P/E, Isn't This Company A Value Play in S'pore Construction Boom?

→ See also: At 3.1x P/E, Isn't This Company A Value Play in S'pore Construction Boom?