• For quite a while, ISDN Holdings didn't gain market favour, its stock staying below the 40-cent level for the better part of the past three years. This was in part because unrealised foreign exchange loss weighing on its reported earnings even as its core profit strengthened. • It FY2025 core profit rose 25.9% year-on-year to S$9.7 million, the second straight year of growth for the company and it was supported by steady performance across its main business segments and markets. • Today, a bullish analyst report by CGS International, the only house covering ISDN, has driven the stock 24% higher to 60 cents. • Analyst William Tng, who put out the highest target price of $10.15 for AEM Holdings last week, has sharply revised the way he values ISDN -- at 24x FY27F P/E from 13.5x. |

Excerpts from CGS report

Analyst: William Tng, CFA

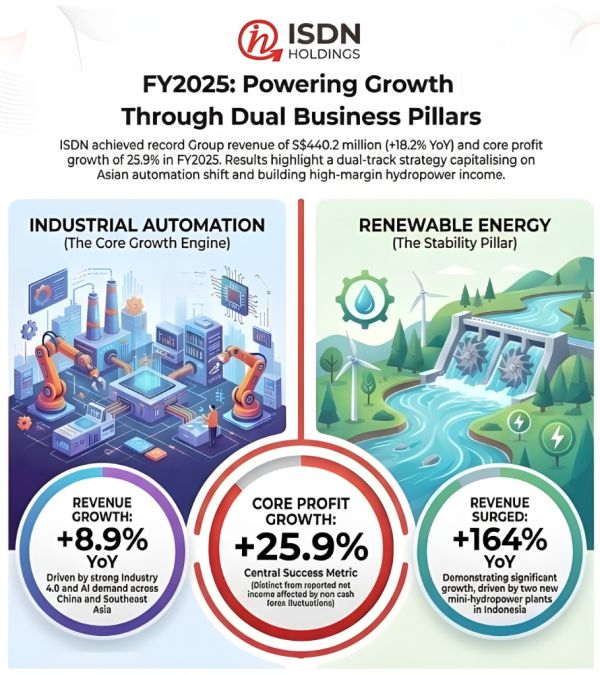

■ FY25 revenue (S$440, +18% yoy) was 6% above our forecast due to recognition of construction revenue from its mini-hydropower plants.

The decline was due to S$4.5m of unrealised foreign exchange loss. ■ With demand for its key Industrial Automation business still resilient, we lift FY26-27F EPS by 22-36%. Reiterate Add with a higher S$0.96 TP. |

|||||

| Core net profit grew 26% yoy in FY25 |

ISDN reported FY25 revenue of S$440m (+18% yoy).

This was driven by its Industrial Automation (IA) business in China (64% of FY25 revenue) which grew 5% yoy on the back of spending on automation to improve productivity and S$49m in construction revenue from its two new mini-hydropower plants in Indonesia.

In local currency terms, its IA revenue in China grew a stronger 7% in FY25.

Gross margin for the key IA business was relatively stable at 24.3% in FY25 versus 24.2% in FY24.

ISDN incurred S$4.5m of unrealised, noncash foreign exchange revaluation losses arising from its mini-hydropower plants in Indonesia in FY25 as the US$ weakened against the S$.

ISDN’s renewable energy business generates recurring revenue and profits from long-term contracts of up to 25 years.

Under this arrangement, ISDN’s recognises long-term receivables and payables which are revalued for each reporting each period, resulting in non-cash, unrealised foreign exchange gains or losses.

A final DPS of 0.53 Scts was declared.

| IA demand resilient, further progress in mini-hydropower business |

ISDN continues to see broad-based demand for its IA business as factories continue to enhance their capabilities via advanced IA solutions.

The group has also expanded its presence across Asia to capture emerging opportunities from Malaysia and Taiwan amid ongoing global supply chain diversification.

ISDN intends to leverage its extensive sales network and regional footprint to advance the group’s growth trajectory.

ISDN also continues to grow its renewable energy business, with two additional mini hydropower plants scheduled for completion in 2026.

William Tng, CFA, analystWe value ISDN at 24x FY27F P/E, 1 s,d. above its 10-year (FY17-26F) average. William Tng, CFA, analystWe value ISDN at 24x FY27F P/E, 1 s,d. above its 10-year (FY17-26F) average.Our previous valuation was 13.5x, its then 10-year (FY16-25) average P/E. Our FY26-27F EPS forecasts rise by 22-36% as we raise our revenue forecasts by 10% to reflect resilient demand for its IA solutions. Reiterate Add as we expect earnings growth to resume over FY26-28F. We think the stock could also attract buying interest from Equity Market Development Programme (EQDP) funds. Re-rating catalysts: higher-than-expected net profit contribution from its hydropower business segment, a faster pace of economic growth in China as it stimulates its economy, and a stronger global semicon recovery. Downside risks: weak customer demand if the global economy continues to slow, and potential bad debts as economic conditions worsen. |

→ See also: ISDN: Core Profits Surge 26% In Second Year of Turnaround, Future Drivers Include Data Centres

→ See also: ISDN: Core Profits Surge 26% In Second Year of Turnaround, Future Drivers Include Data Centres