• Just two years ago, Wee Hur Holdings traded at around 20 cents, so it's hard to believe it has shot up 4X since, inclusive of dividends. • Key reasons for performance:

• DBS Research has just initiated coverage with a 90 cent target price, joining CGS which has ongoing coverage with a target price of 95 cents. Read more ..... |

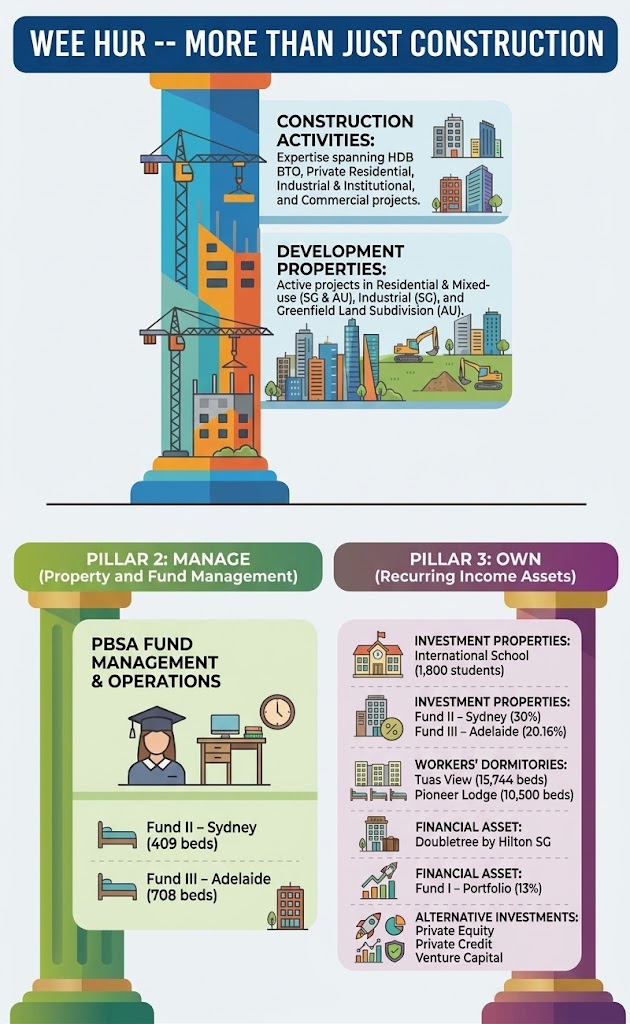

Wee Hur has evolved from a construction company to a diversifed business:

Excerpts from DBS report

Analysts: Jia Hui NG, Derek TAN & Geraldine WONG

• Scalable fund platform fueling PBSA growth • Growth will be driven by newly completed 10,500-bed workers’ dormitory, representing a 67% increase in bed count • Proxy for construction growth in Singapore, underpinned by its construction and workers’ accomdation segments • Initiate with BUY and TP SGD 0.90 |

Investment Thesis: Diversifying from its roots in construction.

Wee Hur began as a construction company in 1980 and has since transformed into an investment holding company with diversified operations in construction, property development, workers’ accommodation and purpose-built student accommodation (PBSA).

The Group operates a massive portfolio of 6,779 student housing beds under the Y-Suites brand across 5 key locations in Australia, and more than 25,000 beds in 2 large scale workers’ dormitories in Singapore.

|

WEE HUR |

|

|

Share price: |

Target: |

Proven track record in fund management.

Wee Hur has built a diversified fund management platform, managing multiple funds to scale its PBSA exposure.

The platform has attracted institutional validation from sovereign wealth fund GIC and Greystar.

As the Group continues to roll out its multi-fund strategy, successful execution and growth are key rerating catalysts.

Workers’ dormitory segment poised for significant revenue uplift.

Wee Hur’s Tuas View Dormitory, Singapore’s largest purpose-built dormitory, achieved 95% occupancy in FY25.

The newly completed Pioneer Lodge adds 10,500 beds, with 67% committed occupancy, and is expected to achieve full occupancy by year-end, contributing SGD 30–40 mn in FY26 and lifting the segment to a record revenue run rate.  DBS expects Pioneer Lodge, whose occupancy is rising to full likely by year-end, to contribute SGD30-40mn in revenue in FY26.

DBS expects Pioneer Lodge, whose occupancy is rising to full likely by year-end, to contribute SGD30-40mn in revenue in FY26.

Our valuation is based on a sum-of-the-parts (SOTP) approach, valuing the dormitory and construction segments at 4x P/E and 8x P/E, respectively. This yields a SOTP valuation of SGD1.06/share, translating to a TP of SGD0.90/share after applying a 15% holding company discount. Key Risks -- Rising construction costs due to Middle East tensions, and changes to Australia’s student visa policies or international enrolment caps. |

→ See the DBS report here

→ See the DBS report here

→ See also: Record Construction Orderbook, New Dorm, Aussie Landbank ... This Company's Growth Drivers Are Multifold