'Loquat Fan' contributed this article to NextInsight

Garden Fresh's popular loquat juice has helped drive up sales of Garden Fresh, and its parent, Sino Grandness.SINO GRANDNESS has just announced (14 Aug) that it is in discussion with a potential strategic investor which is seeking to invest a "substantial stake" in the company.

Garden Fresh's popular loquat juice has helped drive up sales of Garden Fresh, and its parent, Sino Grandness.SINO GRANDNESS has just announced (14 Aug) that it is in discussion with a potential strategic investor which is seeking to invest a "substantial stake" in the company.

The word 'strategic' suggests that it is unlikely to be a passive investment by, say, private equity. Before speculating on the likely business arrangement between the two parties, it is important to note that Garden Fresh (the beverage brand belonging to Sino Grandness) is a relatively new business.

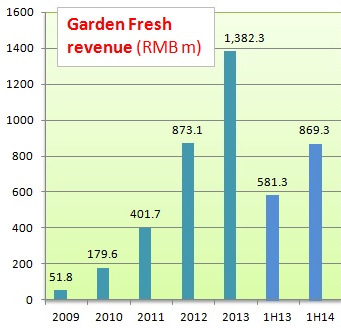

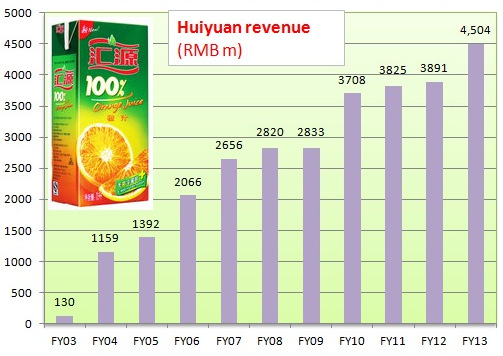

Through mainly its loquat juice drinks, it has grown strongly and by 2013 its sales were roughly one-third of China Huiyuan's, the No.1 orange juice producer in China.

Huiyuan is among a handful of beverage companies in China that have conquered vast tracts of the Chinese market.

Garden Fresh was the first to introduce loquat juice, which caught on among consumers partly for its therapeutic value as loquat is known to soothe the throat.

Before the introduction of loquat juice by Garden Fresh, loquat was available only in paste form or as fresh fruit for a limited period as it is harvested only between March and May.

Loquat juice and other fruit juices are riding on a strong health trend among consumers while carbonated drinks are finding it hard to grow sales. (See also: SINO GRANDNESS: Aiming To Stay No.1 In Loquat Juice Market)

Listed on the HK Stock Exchange, China Huiyuan has enjoyed strong growth for its beverages, especially orange juice.

Listed on the HK Stock Exchange, China Huiyuan has enjoyed strong growth for its beverages, especially orange juice.

In my view, it's especially challenging for any beverage company to try to win a significant share of the loquat juice market from Sino Grandness.

Unlike oranges which can be harvested all-year round and are widely planted, loquats are ripe for the picking only in the March-May period and are less widely planted. In addition, loquat is commercially farmed in China only, not outside.

Thus, the limited supply and the need to store loquat puree for year-round production of the juice are barriers to entry into this business.

It is likely that the potential investor in Sino Grandness is a beverage company enamoured of the dominance of the Garden Fresh brand in China and the extensive distribution network that it has built up.

Following the rapid growth of Garden Fresh, Sino Grandness has apparently set its sights on internationalising the Garden Fresh brand, and is making preparations for this.

In fact, UOB Kay Hian analyst Brandon Ng has alluded to the impending start of Sino Grandness' "export business for its beverage products", in his Aug 14 report.

The strategic investor could be an overseas company which has the resources to introduce Garden Fresh products to its home market.

Any partnership would be even more synergistic if there is scope for Sino Grandness to enable the prospective investor's products to be distributed via Sino Grandness' expansive network in China.

Sino Grandness' announcement did not specify what constitutes a substantial stake. If it is 20%, chairman and CEO Huang Yupeng’s existing 40% stake in Sino Grandness will dwindle to just 32% after the share placement.

For Mr Huang to make such a great sacrifice, the investor must be a large concern with the necessary financial resources and marketing channels to help Sino Grandness expand beyond what it can on its own device.

|

Barely three years later, in early 2013, Kirin’s ambition was dashed when F&N was acquired by Thai tycoon Charoen Sirivadhanabhakdi, who owns Thai Beverage which produces beer, spirits and beverage. In taking stakes in F&N, both Kirin and Sirivadhanabhakdi must have been eyeing F&N's extensive distribution network in Thailand, Malaysia and Singapore to sell their own products, as well as help F&N extend its geographical reach. |

Recent article: SINO GRANDNESS -- $1.02 Target, DMX -- 23 Cents Fair Value

Were there any announcements on the strategic investor from Ferro?

Are you saying that there are no strategic investors for S Grandness?

The rest of the story I don't have to say...