|

Singapore-listed China Aviation Oil (CAO) has given the news on 8 Jan: the Chinese government has approved the merger of its parent company, CNAF, with Chinese global energy giant Sinopec Group. Essentially, Sinopec (also known as China Petrochemical), the world’s largest oil refiner, is absorbing CNAF, the 51% majority owner of CAO. |

Observers say that while CAO has released a filing stating that "business as usual" continues for now, the future reality could be much more positive:

-

Cheaper Money: Being part of the Sinopec family will likely lower CAO’s cost of capital given that Sinopec is a Fortune Global 500 company.

CAO handles massive volumes of fuel trading annually but it doesn't fund every purchase with its own cash — it relies on bank-issued Letters of Credit.

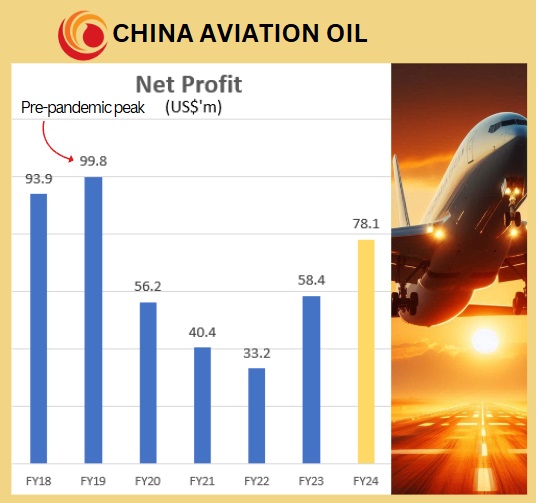

Currently, CAO holds net cash of ~US$500 million as a safety net (seen by the market as overly conservative) because it is a standalone entity in a volatile market.

With Sinopec as a backstop, CAO will no longer need to keep a massive "rainy day fund" and can deploy it for M&A or — more importantly for shareholders— higher dividends.

"Sinopec’s oversight could also support stronger capital discipline and higher dividends, consistent with broader SOE reform objectives aimed at enhancing shareholder returns," said DBS Research in a Nov 2025 note. -

The "Refinery-to-Wing" Advantage: The merger removes middleman markups and streamlines the entire supply chain.

Currently, Sinopec refines the jet fuel and sells it to CNAF, which then manages the storage and refueling at over 250 airports.

Every time fuel changes hands from Sinopec to CNAF, there are administrative, transactional, and profit-margin layers added to the cost.

By merging, these two entities eliminate internal markups, observers say.

This might translate into higher gross margins for CAO as well as savings for its customers (the airlines). -

A "Green" Growth Engine: Sinopec is a leader in Sustainable Aviation Fuel (SAF) technology.

Sinopec owns the proprietary "SRJET" technology to produce green fuel.

Xinhua was reportedly noting that the merger will remove commercialization bottlenecks of SAF and promote large-scale adoption at domestic airports to achieve a green and low-carbon transition.

As the world’s airlines pivot to green energy, CAO is positioned to be the primary distributor for Sinopec’s SAF exports.

That looks like a new revenue stream waiting to happen.

Lim & Tan Securities' take:

|

|||||||||||||||

See also: CHINA AVIATION OIL: DBS Report Sparks Rally with Above-Consensus Earnings Forecasts and Target Price