Drums of copper wires as feedstock to produce electrical cables. Tai Sin Electric's MD, Bobby Lim, is in white shirt. Photo by Sim Kih

Drums of copper wires as feedstock to produce electrical cables. Tai Sin Electric's MD, Bobby Lim, is in white shirt. Photo by Sim Kih

A driver transports drum of finished cable. Tai Sin Electric's chief operating officer, Bernard Lim, is in the foreground. Photo by Sim Kih

A driver transports drum of finished cable. Tai Sin Electric's chief operating officer, Bernard Lim, is in the foreground. Photo by Sim Kih

TO MANY INVESTORS, Bobby Lim is a familiar name seen in the top shareholders' list of many a company's annual report.

Mr Lim is what you might call an accumulator of shares -- he just keeps buying. (Read The Edge magazine's excellent profile of Mr Lim here)

In his day job, he is the MD of a listed company, Tai Sin Electric, which manufactures cable & wire -- a long-time business which has defied the label "sunset industry" cast on it by skeptics.

Tai Sin was listed on the stock exchange in 1998 and, in recent times at least, has generated good cashflow and, in turn, has paid out steady dividends.

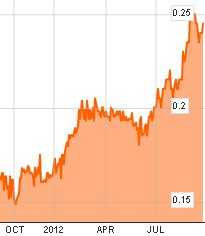

Tai Sin stock has gained 53% in the year to date. Chart: Bloomberg.Dividends -- this is what investors have been hungry for amid the stock market turbulence and economic uncertainty of the past few years.

Tai Sin stock has gained 53% in the year to date. Chart: Bloomberg.Dividends -- this is what investors have been hungry for amid the stock market turbulence and economic uncertainty of the past few years.

Tai Sin's steady dividend payout has seen investors buy up the stock.

The stock is up 53% in the year to date, rising from 16 cents to close at 24.5 cents last Friday. The company currently has a market cap of S$102 million.

Despite the rise, the stock currently has a running yield of 8.57%, thanks in part to the proposed final dividend of 1.5 cents a share for FY12 (FY11: 10 cents).

A dividend of 0.6 cents a share was paid out at half-time in the FY.

With rising investor interest around this stock, a Tai Sin Electric shareholder arranged for us to meet Mr Lim and visit the company's manufacturing facility in Gul Crescent last week.

Here are some key takeaways from our meeting, which was also attended by Tai Sin chief operating officer Bernard Lim and manager for group corporate development, Tan Yong Hwa:

> Contributors to revenue

Cable and wire -- this segment accounted for S$159.7 million in revenue for FY12 (ended June), or 57.2% of total revenue of S$278.9 million.

This was followed by electrical material distribution, which brought in S$94.2 million, or 38.2%.

The cable & wire segment was boosted by a higher sales volume.

Cable & wire grew 11.1% but sales growth for electrical material distribution was basically flat.

Revenue-wise, FY12 was a record year for Tai Sin, with sales of $279 million of which S$12.9 million came from Cast Laboratories Pte Ltd which was acquired on 31 January 2012 as a 52.5% subsidiary.

Q4 sales for the Group hit a new record of $78.7 million, an 18.5% increase y-o-y.

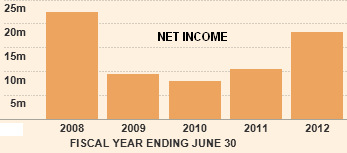

> Net profit up 73%

Net profit for FY12 rose 73% to $18.8 million, boosted by one-offs from insurance claims and an excess of fair value of the NTA of Cast Laboratories over the purchase price.

> Growth drivers

Mr Bobby Lim is only too happy when he learns of en-bloc property sales and new HDB building programmes.

They represent potential business: Whenever a new development comes up, it would need electrical cabling.

Same too for big infrastructure projects such as MRT lines, which would require cabling for tunnels, MRT stations and interchanges.

Big as they seem, such projects don't overwhelm in terms of revenue.

Tai Sin as a group has over 1,000 customers not one of whom accounts for more than 5% of its annual revenue -- and of course, the business is not exposed to the woes of the eurozone.

Mr Lim stressed that Tai Sin has many competitors too.

Still, its FY12 gross profit margin was 18.3%, up from 16.18% in FY11.

Notably, investors should take note of Cast Laboratories, which is in a different business -- it offers independent testing, inspection and certification services as well as heat treatment and specialised geotechnical services.

This is a niche service business with relatively few competitors. But it is in high demand because of the stringent standards of quality required in numerous projects in Singapore, especially.

And with full 12-month contributions in revenue from Cast Laboratories set to happen from this current FY, Cast Laboratories will figure more prominently in its contribution to Tai Sin's topline and bottomline.

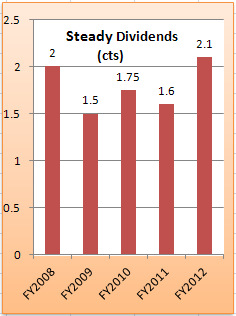

> Track record for dividends.

In the last five years, the dividend has not been less than 1.5 cents a share.

The dividend yield is no less than 6.1% based on current stock price of 24.5 cents.

The year the dividend payout was 1.5 cents was in FY2009, when the net income was slightly less than S$10 million.

FY12 saw net profit soar to S$18.8 million, leading to a 2.1 cent a share dividend payout.

If that is repeated in the current FY, the yield would be a juicy 8.57%.

> No rights issue, placement of shares

Tai Sin's dividend payouts have been good to shareholders.

And they have not been asked to shell out money through a rights issue nor have they, at least in nearly a decade, been diluted through share placements, as Mr Bobby Lim highlighted.

The rights issue in 2007 was carried out in conjuction with a bonus dividend to allow the company to pass on its tax credits under Section 44A of the Income Tax Act.

Any shareholder who used all the bonus dividend to pay for all his rights entitlements did not have to come out with any cash outlay.