Excerpts from recent analyst reports....

Lim & Tan Securities highlights Hi-P's buyback at 71-cent book value level

Hi-P spent $194,471.37 on 4 June buying back 289,000 shares in the open market, the most since it restarted its buy back program on 21 May ’12.

True to management’s guidance, the company began its share buy back program when the stock price was hit close to its book value of 71 cents on 21 May ’12.

While the stock price continued to fall on the back of global stock market weakness as well as a profit warning from its major customer Research In Motion (RIM), the company spent more money each time buying back its shares on 21 May ’12 ($82,248), 23 May ’12 ($112,527), 30 May ’12 ($143,103), 4 June ’12 ($194,471), having since bought a total of 752,000 shares.

With cash holdings of $325mln against debts of $129mln, the company would have no problem continuing its share buy back program.

In the past when the company bought back its shares and backed it up with good financial performance, the stock price had done well.

This time around, management is optimistic that 2H 2012 will see a strong financial recovery (similar to 2010) with the help of Apple, Amazon, Nike, Seagate, Colgate and P&G to help them counter weakness from RIM.

We maintain our BUY recommendation on Hi-P.

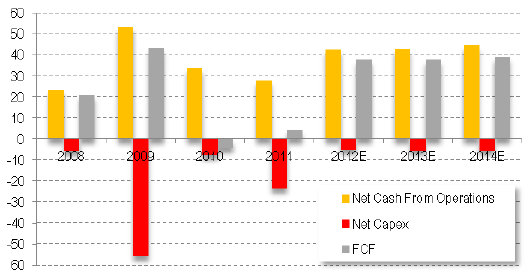

Recent story: HI-P INTERNATIONAL: Record S$180 m capex this year for strong business growth

Maybank KE expects SHENG SIONG's dividend payout to be sustained after FY12.

Analyst: Allison Fok

Although Sheng Siong’s 90% dividend payout commitment (for its IPO) ends in FY12, we strongly believe that it will be sustained.

The group has a strong net cash position of SGD149m, a defensive business model with positive working capital cycle, free cash flow yield of 8.7% and no major capex requirement in sight.

Growth secured for 2012. Management has secured two outlet spaces which has commenced operations this quarter.

They would increase the group’s current store space of 367,800 sq ft by 3.6%.

We estimate FY12F-14F recurring net earnings to grow at 14.9% CAGR, driven by steady outlet growth, better utilization in new outlets and improving margins. Given its target of low-to-mid-end mass market, it is also a recession-resilient business.

We initiate coverage on Sheng Siong Group with a BUY rating and target price of SGD0.52, based on 18.8x FY13F earnings, pegged to Dairy Farm International and applying a 25% discount. Assuming 90% dividend payout, our target price would imply a sustainable forward dividend yield of 4.8-5.4% p.a.

Recent story: SHENG SIONG: 1Q2012 net profit up 74% on gain from warehouse sale

Comments

To answer your sarcasm (I'm sure it wasn't meant to be a question) - The phrase "net gross margin" was taken to denote the gross margin less the 3 items (a) to (c) which had not been taken into account in gross margin of 22 % as quoted in your example. I thought it was quite clear there. Perhaps it's because my command of the English language is not up to the mark and my expression was too pedestrian for college professors to grasp.

Transfered 30 million ordinary shares to Mr Tan Ling San, who joined the firm in 2006, as a gift.

This works out to 2.17 per cent of its issued share capital.

SS Holdings is made up of the three Lim brothers - group chief executive Lim Hock Chee, executive chairman Lim Hock Eng and managing director Lim Hock Leng

These supermarket chains are being kept alive because of good cash flow. That is all. They collect hard cash everyday but make payment 30 - 90 days later.