Excerpts from DBS report

| No slowdown in February despite the epidemic. SEMI recently published its preliminary reading of the 3-month moving average of the worldwide billings for North American-based semiconductor equipment manufacturers in February 2020 and the figure (US$2.4bn; +26.2% y-o-y) highlighted the continued recovery in the semiconductor industry. This growth was despite the shutdown in China amidst the COVID-19 outbreak. |

Downside risk prevails; outlook muted. However, going forward, though the factories for the semiconductor players were allowed to operate partially in countries affected by the lockdown, production will still be at a sub-par level.

End demand is also expected to be weaker on the back of a slower global economy with some countries, including Singapore, expected to fall into a recession in 2020.

Hence, we expect the semiconductor equipment billings data to taper down. However, on a y-o-y basis it could still record positive growth given a weak 1H2019. Overall, we expect the semiconductor sector to fare better than others in the technology value chain, as it forms part of the essential goods supply chain.

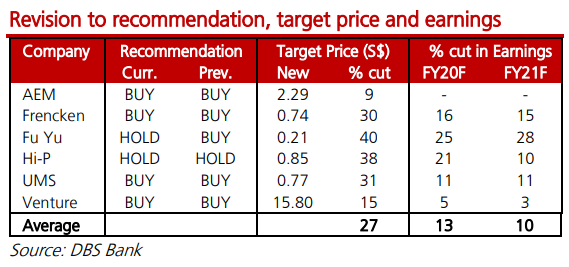

13/10% cuts in FY20F/FY21F earnings. In terms of earnings forecasts, we have revised down FY20F and FY21F figures for stocks under our coverage by an average of 10-13%, mainly on supply disruptions, weaker demand and margin pressure. FUYU and Hi-P saw a steeper cut in FY20F earnings of 25% and 21% respectively. We expect lower revenue across all segments for FUYU, except Medical. Hi-P is mainly on weaker mobile phone sales and margin pressure. Our target prices are cut by 27% on average. We have also downgraded Fu Yu to HOLD from BUY. |

AEM has one factory located in Malaysia (Penang) and c.34% of its revenue in FY2018 was from Malaysia. However, we believe that with a portion of Intel’s chips used in mission-critical medical applications, AEM’s factory in Malaysia should still be able to operate, albeit at a reduced capacity. We estimate AEM’s Malaysia factory to be operating at 30-40% production capacity. Intel’s factories are still in operation; company cites uncertainty in outlook. On 19 March, Intel’s CEO announced that its business as usual for Intel’s vast manufacturing operations despite the shutdown in the US. He said that it is fulfilling more than 90% of orders on time. However, he also believes that there could be a financial impact on the company’s business due to a slowdown in the global economy. Working from home raises demand for server processors. With more companies implementing a work-from-home policy for its employees amidst the COVID-19 outbreak, the demand for laptops and server capacity has surged. The use of remote working applications such as Zoom, Webex, and Skype has increased dramatically. Cisco saw a 22-fold increase in the amount of network traffic in February. More computing power is required for these communication companies to cater to the increased users and as a result, server chip demand has risen.

|

Full report here.