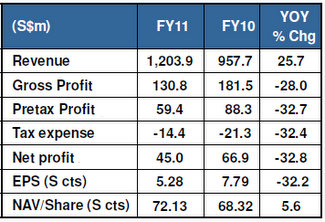

HI-P INTERNATIONAL has just had a 4Q2011 which was sharply more profitable ($9.4 million) than 3Q of 2011 ($6.5 million) but it expects the current year’s 1Q to be loss-making.

“Our customers’ business has dropped quite quickly and our new businesses have not caught up fast enough,” said Mr Yao Hsiao Tung, Hi-P’s executive chairman and CEO, at a briefing for analysts and investors last Friday.

“Also, we are facing material and component costs which are pretty high.”

Beyond the immediate term, Mr Yao guided for higher revenue and profit for Hi-P in the second half of this year compared to 1H2012.

And for the full year, “we expect higher revenue and profit in FY2012 as compared to FY2011.”

Much of the Q&A session at the briefing at Carlton Hotel was intensely centred on Hi-P’s just-announced S$180-million capex for this year and the optimistic prospects that it implies not only for 2012 but beyond.

It's record spending and is a few multiples of the the capex in the last couple of years which ranged only between $30 million and $70 million.

The reason was speculated on about a week ago by DMG & Partners in a report that sent the stock soaring from around 70 cents to above $1: “Our channel checks show that the group has already secured a large order for its new metal-casing business, which we believe to be Apple.”

Hi-P subsequently clarified that the report is not accurate and gave some insights into its business plan.

In any case, the S$180 million capex is so big it has to be among the biggest, if not the biggest, by a Singapore-listed company for 2012 (at least).

Highlights of the Q&A session, with answers from a panel of senior management (photo above):

Q: You have quite an ambitious capex plan for this year. In the past you have been very careful about capex. Seems like you are confident of securing a lot of business – can you let us know the products you are seeing strong orders for and the new business you are expanding into?

A: It’s true we are very cautious about spending money.... Potential projects include smart phones, tablets, metal casing and metal parts. News reports about metal casing business are not accurate but not totally wrong.

Of the $180 million capex, 30% is for injection moulding machines, 30% is for metal-stamping and CNC machines, 15% is for renovation, 10% for tooling, and 15% for R&D, automation and FPC, etc. We are investing in different processes to cater for business growth.

Last year we were heavily dependent on one customer. This year will see a big difference because of other customers' contribution.

Q: For the new metal casing business, will you be the main contractor or sub-contractor?

A: In our business model, we always have direct relationship with the OEMs.

Q: Given that Foxconn (which is already supplying to Apple) and others are entrenched in the industry, why would certain customers consider new players like Hi-P?

A: Any customer would like to diversify their supplier base, just as we would like to diversify our supplier base too. Customer feedback is they are comfortable with us.

Q: Can you tell us about the timing of the capex?

A: It will be spread gradually throughout the whole year. It would be a bit more in the first half than the second half.

Q: For the metal casing business, when do you expect the machines to come in?

A: Some of the machines are already installed, and some are on the way. All this is planned according to project requirements. But the majority of the machines will come in in 1H.

Q: How many customers have you secured for metal casing?

A: We are still working on it.

Q: For personal grooming devices and household appliances, is there more outsourcing from customers not just for parts but also whole-builds? Is that why there is a big jump in your revenue?

A: We do see a trend towards more box-builds. In addition, we are doing box build for wireless devices.

Q: How severe would the impact be on Hi-P as Europe goes into recession?

A: The business segments we participate in are still growing.

Q: Foxconn has just said it would raise wages again for its workers. When they did it a year ago, it brought up costs in China because they are a big employer. What will be the impact on Hi-P?

A: What we are paying is already above market rate, and we will continue to intensify our automation level.

Q: What’s your current headcount and estimated figure by year-end?

A: Now, it’s 13-14K in China. At year-end, it would be still in this range. For all our new projects, we are putting in a lot of automation. And with the switch in product mix in 2H, we believe there is an opportunity to automate processes.

I have asked the finance department to work closely with operations to lower our breakeven point, to be more lean and fit, to use space and equipment well.

I feel very comfortable now compared to a couple of years ago. One of our main customers have recently ranked us No.1 supplier. Our quality was rated 100%. So, Hi-P continues to make progress.

Q: You have so much cash (net $220.3 million) but you still take on a lot of bank borrowings (S$119.4 m).

A: We borrow the USD in Singapore and remit to China to enjoy high deposit rates there. So we hedge in USD and benefit from the spread in interest rates. That’s why our interest income has increased.

Q: To maintain the same dividend for FY11 as in FY10 would not have been a problem given the cash you have. Why did you cut the final dividend (from 3.6 cents to 2.4 cents a share)?

A: The dividend payout ratio (44%) wasn’t cut. To be on the conservative side to manage the cashflow, we maintained the payout ratio. We forsaw the heavy capex this year and the growth of business. Most of the capex would be self-funded.

Hi-P's official powerpoint presentation and financial statements for FY2011 results are accessible at the SGX website.

Recent story: HI-P reignites buyback program, SERIAL shares sought by chairman