SUPER GROUP, which has had a sizzling business and stock performance so far this year, has served up more good news: record quarterly sales of S$86.8m for 3Q10, up 12% year-on-year.

Gross profit margins improved by 6.6 percentage points to 40% due to lower production costs, while net profit increased by 49% to S$13.6m.

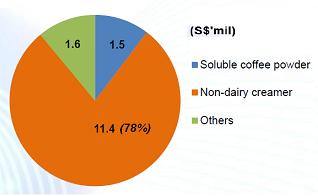

3Q10 ingredient sales grew 47% to S$14.5 million, driven by non-dairy creamer.

3Q10 ingredient sales grew 47% to S$14.5 million, driven by non-dairy creamer.

Ingredients sales increased by 47% to S$14.5 million, thanks to greater demand for non-dairy creamer, particularly in China, where contracts with major beverage manufacturers were secured.

A new production line had been completed in Sep, adding 25,000 metric tonnes annual capacity for non-dairy creamer at Wuxi.

”We want to distribute instant beverages to hotels, restaurants and cafes in China and Taiwan,” said Super’s business development manager, Darren Teo, at an investor briefing held at Republic Plaza today.

The 3-in-1 instant coffeemix player intends to shift its production of non-dairy creamer to China, which will have 75,000 tons capacity for this product by next Aug.

Its Singapore plant will be converted to produce foaming creamer and fat-free milk, which are more lucrative.

”We want to leverage on Singapore's reputation for food safety to position our plant here as a high-end ingredient sales hub,” he added.

Other higher-margin products include the newly launched organic instant soymilk and Ipoh white coffee product range.

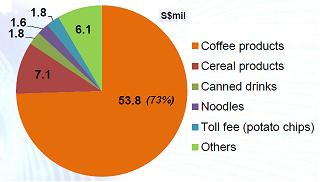

3Q10 consumer goods sales were up 7% at S$72.3 million, driven by 3-in-1 instant coffeemix.

3Q10 consumer goods sales were up 7% at S$72.3 million, driven by 3-in-1 instant coffeemix.

Consumer goods sales increased by 7% to S$72.3 million mainly due to higher sales into the Thailand, Malaysia and Mongolia markets.

The 3-in-1 instant coffeemix maker sustained a forex loss of S$1.6 million (3Q09: S$300,000) as the USD depreciated against the Singapore dollar by about 6%.

Taxation increased to S$2.4 million to (S$0.7m in 3Q09) as higher tax provisions were made for an impending expiry of the tax incentive for an overseas subsidiary.

Cash reserves were S$120.7 million as at Sep.

Below is a summary of questions raised at the investor briefing and replies given by Mr Teo and Super’s financial controller, Koh Chun Yuan.

Q: Why are the ingredient orders growing so fast?

There is huge growth in demand for milk tea in China. One of our customers is projecting that its sales will double next year.

The son of Super's founder, Darren Teo spearheads Super's business development. Photo by Pearl Lam

The son of Super's founder, Darren Teo spearheads Super's business development. Photo by Pearl Lam

Q: Have you got new customers for your ingredients division?

Utilization is now at 90% to 95%, so we do not have capacity for new customers. Our top 3 customers already command 80% of the milk tea market. Other than hiring us, these customers are also using other ingredient makers as our capacity constraint is preventing us from meeting their total production volume.

Q: What is the penetration of your high margin products?

We have launched our advertising and promotion for 100% organic soymilk in Singapore and Malaysia. Next year, we expect to roll this out in Thailand, Myanmar and Indonesia.

At more than S$7 for 15 sachets for 100% organic soymilk, our strategy is to target this product at markets with affluent consumers. We will be rolling out a less pricey range of soymilk that is partially organic.

We are shifting our advertising dollar to Ipoh white coffee and functional coffee.

Q: How does the spike in raw materials impact you?

Robusta coffee beans are now about US$2,000 a ton, compared to its high of US$2,500. Palm kernel oil is now US$1,800 (record levels) and sugar at US$800 has been rising and is nearing record high.

We have already adjusted our prices during the previous round of commodity price increases, so we have been able to protect our gross profit margins.

Q: If raw material prices continue to rise, will you be able to maintain margins by improving product mix?

Nestle is the price leader. Large food manufacturers such as Unilever, Kellogg’s have been reported to be increasing retail prices next year. We may raise our retail price, depending on competitor action and consumer sentiment.

Q: Why are you keeping such a large cash reserve?

Other than organic growth, we are looking at acquiring brands with a presence in regions we are not strong in. This will probably be a coffee or instant beverage brand.

Q: Have Japanese F&B players approached you for M&A?

Japanese brewer Kirin recently bought Temasek’s 15% stake in F&N. Yes, we have been approached by F&B players as there is value in our integrated business model which includes manufacturing, distribution and brand building. However, we are not open to M&A that does not value-add to us.

Related story: SUPER GROUP, YONG XIN: What Analysts Say Now