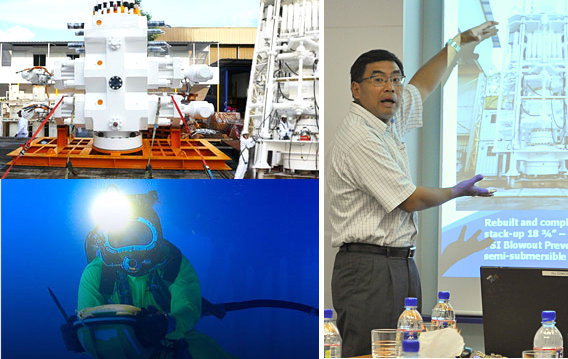

MTQ, with its robust growth prospects, is one of OSK-DMG's top offshore stocks. CEO Kuah Boon Wee (above, right) wants to maximize yields in Singapore and grow in Bahrain. He also wants to boost the profitability of newly-acquired Neptune Marine Services, and expand its business beyond Australia.

MTQ, with its robust growth prospects, is one of OSK-DMG's top offshore stocks. CEO Kuah Boon Wee (above, right) wants to maximize yields in Singapore and grow in Bahrain. He also wants to boost the profitability of newly-acquired Neptune Marine Services, and expand its business beyond Australia.

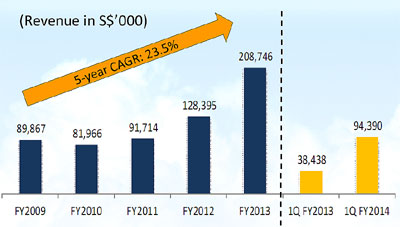

OSK-DMG maintained its ‘Buy’ call on MTQ Corporation after it posted a 38% increase in net profit attributable to shareholders of S$6.5 million for the three months ended 30 June 2013 (“1QFY2014”).

The OSK-DMG analyst, Mr Lee Yue Jer, who likes the stock for its strong cash generating ability, raised his target price to SGD2.20 based on 10x FY14F EPS. CEO Kuah Boon Wee cautioned that revenue from Neptune is likely to dip for the upcoming quarter because its diving campaign had ended in 1QFY2014. Photo by Sim KihMTQ, a regional engineering, maintenance and subsea services group, reported 1QFY2014 revenue of S$94.4 million, an increase of 146% year-on-year, boosted by contributions from ASX-listed subsidiary, Neptune Marine Services.

CEO Kuah Boon Wee cautioned that revenue from Neptune is likely to dip for the upcoming quarter because its diving campaign had ended in 1QFY2014. Photo by Sim KihMTQ, a regional engineering, maintenance and subsea services group, reported 1QFY2014 revenue of S$94.4 million, an increase of 146% year-on-year, boosted by contributions from ASX-listed subsidiary, Neptune Marine Services.

Neptune provides underwater welding services and started contributing to MTQ after it became a 86.8%-owned subsidiary.

Neptune's services also include asset integrity maintenance and service, diving, fabrication & offshore, subsea engineering, geomatics, ROV, subsea stabilization and NEPSYS.

MTQ’s two other business segments are:

>> Oilfield Engineering Services operating out of Singapore and Bahrain. It specializes in oilfield equipment repair and reconditioning, component manufacturing, fabrication and rental. In particular, it is a niche player in components related to the Blow-Out Preventor used in oilrigs.

>> Engine systems distribution and service in Australia, with a focus on turbochargers and fuel injection engines

MTQ's 1QFY2014 revenue multiplied more than twofold after consolidating revenues of its new subsidiary, Neptune.Its oilfield engineering segment margins improved during 1QFY2014, but the Group’s gross profit margin eased to 29.9% as Neptune has relatively lower margins.

MTQ's 1QFY2014 revenue multiplied more than twofold after consolidating revenues of its new subsidiary, Neptune.Its oilfield engineering segment margins improved during 1QFY2014, but the Group’s gross profit margin eased to 29.9% as Neptune has relatively lower margins.

Cash balance was S$38.7 million and net gearing was 19.6% as at 30 June 2013.

”I am cautiously optimistic as our project delivery pipeline is healthy but cost is a concern,” said CEO Kuah Boon Wee during an investor meeting on Wed.

Utilization of the world’s fleet of oilrigs has been firm over the past couple of years. The industry's prospects remain strong, and DNB Oil expects offshore exploration and production operating and capital expenditure to grow 10% a year over the long term.

Below is a summary of questions raised at the investor briefing and the replies made by the CEO and CFO Dominic Siu.

Q: Do you have access to shipyards that are building jack-up rigs in China?

We approach these rig builders through our customers and principals. Our drilling contractor customer has ordered rigs from Chinese yards. Chinese yards usually adopt a vessel-building model like Singapore yards: They take care of fabrication and rely on National Oilwell Varco or Cameron for the OEM equipment stack. 'We have a healthy cash balance,' said CFO Dominic Siu.

'We have a healthy cash balance,' said CFO Dominic Siu.

Photo by Sim KihQ: Is relocating out of Singapore a possible solution to cut costs?

The big boys like Keppel Shipyard and Sembawang Shipyard are not moving and we need to be near our customers.

What is interesting is we are getting work from customers in Malaysia and Batam, where the cost of operation is in fact cheaper than in Singapore. We are able to attract orders because we have a fast turnaround time and we have a good equipment stockist.

Q: Is there a likelihood of you delisting Neptune?

Our costs for maintaining Neptune’s listing are: its listing fee of A$250,000 a year, plus an independent director in Australia who costs A$140,000 a year.

However, Neptune has over 3,700 shareholders and we need acceptances from more than 90% of them to delist. Moreover, we are able to operate Neptune like any other subsidiary. Thus, delisting Neptune is not our priority.

Q: It has become fashionable for small companies to raise money through Medium Term Notes. If all your competitors are issuing MTN notes for M&A and you remain conservative, does that disadvantage you?

In the past, MTN offered a longer tenure so that we can spread out our loan maturities. However, MTN these days have maturities comparable to what banks offer. There is no push factor to consider MTN because the banking sector serves our needs.

Only a small portion of our debt is in Singapore dollars. Even though there are multi-currency options in MTN, there are currency swap costs associated with these options. At the end of the day, it may not be a cheaper option, especially since such a source of funds usually costs 6% to 7% a year.

Related story: MTQ, UNI-ASIA, TRIYARDS: What Analysts Now Say...