UBS: Maintains ‘Buy’ on XTEP

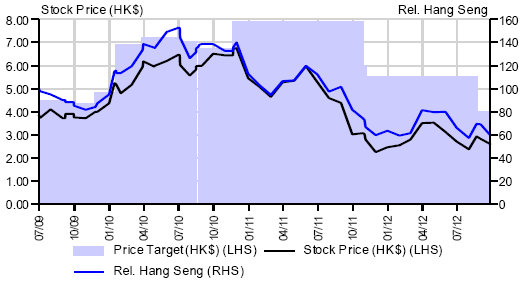

UBS Investment Research said it is maintaining its “Buy” recommendation and 4.00 hkd target price on fashion sportswear firm Xtep International (HK: 1368), saying Xtep is actively restructuring its product designs and selections to produce merchandise that consumers truly want.

The Swiss research house said it expects the Hong Kong-listed sportswear maker to also enjoy a healthier cash balance going forward which will enable potentially richer dividend payouts.

“We conducted detailed analysis on Xtep’s cash balance to assess its capacity to pay higher dividends in 2012-14.

"Based on the results, we believe its cash balance could continue to rise in a fixed-dividend scenario,” UBS said.

It stress-tested its analysis assuming 10% and 20% downside to its earnings estimates.

“The results suggest Xtep has the capacity to pay a higher dividend even if fundamentals worsen.

"We revise our estimates assuming 2012-14 dividends remain at the 2011 level.”

Product design driven by front-line feedback

Early indications from the distribution channel suggest Xtep’s H213 product portfolio will be much more attractive.

UBS said Xtep is actively restructuring its product design, wholesale, and distribution functions "by incorporating more involvement from large distributors and retailers in product design process."

"The initial impact was significant—more distributor involvement in the design process led to the redesign of up to 50% of SKUs, helping Xtep produce merchandise that consumers want. The results are encouraging and indications from the distribution channel shown Xtep’s 2H2013 product portfolio will be much more attractive,” UBS said.

Flatter organizational structure helps Xtep remain competitive

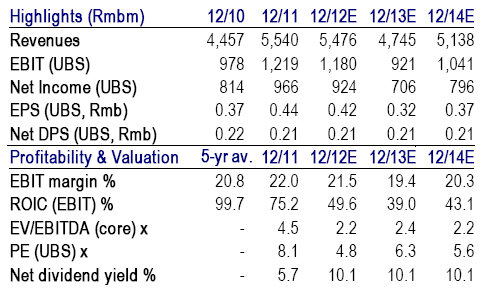

Xtep recorded earnings growth in H112 while all domestic peers recorded declines.

“We believe this is because Xtep’s flatter organization structure has helped the company gradually evolve to adapt to changes in the retail environment.

“Our checks suggest management is actively restructuring its product design, wholesale, and distribution functions.”

See also:

XTEP: Overperforming In Overcrowded, Overstocked PRC Sportswear

TWO LEFT FEET: China Sneaker Play Li Ning Sees Dire Year

Houses Hike XTEP To ‘Outperform’, 'Buy'; GIORDANO Target 15% Upside

UBS: Top Consumer Picks; Sportswear Recovery Seen

UBS Investment Research says that the sportswear sector will surprise on the upside going forward.

“We expect sportswear to be one of the first of the consumer discretionary segments to emerge from the current downturn, as the consolidation process is near completion,” the Swiss research house said.

It added that while store closures for listed sportswear firms might seem low, most non-listed sportswear companies have either exited or scaled back their operations materially in the past two years.

“We turn bullish on the sportswear segment.”

For the Hong Kong-listed consumer stocks, UBS said its preferred plays are sportswear firm Anta (HK: 2020) and iconic liquor maker Kweichow Moutai (SHA: 600519).

“Our least preferred are Belle International (HK: 1880), China Yurun Food (HK: 1068), Golden Eagle (HK: 3308), Li & Fung (HK: 494), Lianhua (HK: 980) and Parkson Group (HK: 3368).

See also:

XTEP Orders Lead Sector

XTEP: In It For The Long Run With Marathon, Social Media