DESPITE DANGEROUSLY high inventories by rivals and cut-throat competition in China’s sportswear sector, Hong Kong-listed Xtep International (HK: 1368) has managed once again to surprise on the upside with its interim earnings, thanks to a run-away performance by its running shoes.

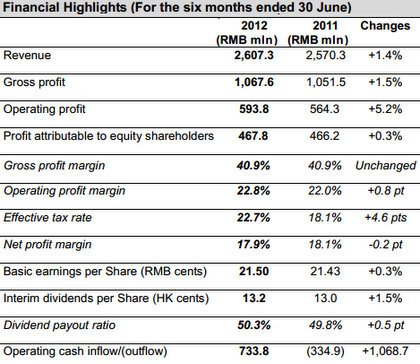

The sportswear firm sports one of the most generous dividend policies in the industry, with its interim dividend up 1.5% to 13.2 HK cents per share and a high payout ratio for the sector of 50.3% -- as Xtep has had a longstanding tradition since its listing of generously rewarding shareholders as such.

Management was on hand to answer queries from a ballroom full of investors and journalists.

First of all, it should be said that in the current market environment, no PRC-based listed athletic apparel and sports footwear firms are running away with gold medals on the performance or market share side of things.

However, some are clearly overperforming relative to their domestic peers.

Xtep is in this pack of leaders.

In the first half, Xtep International managed to boost its revenue by 1.4% year-on-year to 2.61 billion yuan, producing a 0.3% increase in the bottom line to 468 million yuan.

Perhaps most impressive among its January-June numbers is that the Hong Kong-listed sportswear firm managed to maintain its net profit margin at 17.9% -- head-turningly high in such a downbeat consumer spending climate.

“Despite a slowing Mainland Chinese economy, mounting debt crises in Europe, concerns about the recovery in the US and an extremely overcrowded, overstocked domestic sportswear scenario, we still managed to put up a solid first half performance,” said Xtep International’s Chairman and CEO Ding Shuipo.

He said that with the intense competition in China’s marketplace to shod the soles of an increasingly fitness-savvy and sports-crazed population, it was necessary to appeal to their "brand souls" as well by emphasizing the cache that the Xtep logo enjoys with its enhanced reputation for quality and reliability.

“As the preeminent and most prolific promoter and sponsor of international marathons in the region, Xtep continues to drive home its image as a rising powerhouse in the running sector,” Mr. Ding said.

And Xtep’s Chairman expects more forward momentum, thanks to the company’s growing reputation as the go-to brand for runners – both professional and recreational -- as well as in the youth sector.

“We see more stable growth ahead as we successfully expand our foothold in the youth market in particular.”

Photo: Andrew Vanburen

Clearly driving this point home was the recent performance of one its most high-profile spokespersons.

US sprinter Justin Gatlin won a bronze medal earlier this month in the London Games during the uber high-profile 100 meter dash event, thus bringing global attention to the Xtep brand as he mounted the medals podium alongside the world’s fastest human – Jamaica’s Usain Bolt.

“Although there is no way to quantify the upside, we certainly were happy with our spokesperson’s performance in London this month.

"This not only helps bolster our brand’s recognition worldwide, but also will make it easier for us to sign on additional high-profile spokespersons from sports and entertainment spheres down the road,” Mr. Ding added.

Due to China’s less sluggish GDP growth these past few quarters, most domestic sportswear makers bit off more than they could chew late last year and were faced with overcrowded stockrooms for much of the first half.

This meant drastic discounting which of course cut into margins and watered down erstwhile high-end brand images for some.

Take Li Ning Co for example.

Four years ago, its founder and chief – who gave the company its name – was flying high across Beijing’s Birds Nest Stadium carrying the Olympic Flame to its cauldron while all decked out in his company’s sportswear.

What a difference four years makes.

At the time, it was China’s biggest name in the business, but now – thanks to staggering share price falls and inventory clearance sales – its market cap has plummeted to just 4.9 billion hkd – well below Xtep’s current market cap of 6.25 billion hkd.

“Everyone of us was cutting prices this past half, and our lowest mark was a 30% discount. But we were all in the same boat which allowed only the most efficient of us to end up on top,” said Xtep’s CFO Terry Ho.

Xtep’s shares are currently trading around 2.86 hkd, which is leaning toward the low end of their 52-week range of 2.13 - 4.45 hkd.

“We continue to have one of the highest payout ratios in the sector, with our first half rate at 50.3%. Our steady cashflow and good first half allow us to reward shareholders in this way,” Mr. Ho said.

And while the most prolific ads flooding television, print and new media outlets in the sector typically revolve around one sport – basketball – Xtep was taking a decidedly different step.

“Our peers almost invariably remain focused on basketball. But as the No.1 sponsor of regional marathons, we see the running market as a crucial growing niche for us.

“And our easily identified and remembered ‘Love Running, Love Xtep’ slogan is certainly helping our cause,” he added.

Indeed, it seems Xtep is onto something with its focus on footwear, and running in particular.

While its first half sales of athletic footwear rose 13.0% to 1.19 billion yuan, its apparel sales edged down 0.5% over the same period to 1.35 billion due to what Xtep called “market competition and cost pressures.”

Meanwhile, it gave most of the credit for its footwear performance to “successful running promotions.”

“Running has become our top focus,” Mr. Ho added.

But lest investors think Xtep is destined to become a dedicated running shoe play, they should know that the Hong Kong-listed firm is also planning new Xtep Kids and X-TOP stores to appeal to children and the “urban-youth theme” markets, respectively.

And already with extensive coverage across China in Tier II, III and IV cities with 7,603 outlets to date, Xtep is poised to begin running away with more market share and brand cachet.

But the firm was also wary of the sluggish economy overseas as well as slower-than-expected growth in Mainland China.

For that reason, it was cautiously optimistic going forward, with a potential slowdown in the current half and next year.

However, it does expect a general turnaround in 2014.

"We see 2014 as looking much brighter," said Mr. Ho.

"Investors should not necessarily expect year-after-year of high growth. But we are confident that if a company like Xtep can pay out dividends even in the bad times – it shows our real cash is really REAL, and not just 'figure-wise' profits."

Looking around the coverage space, HSBC is still "Underweight" on Xtep with a 2.20 hkd target due to "lack of visibility on future growth prospects" despite the sportswear firm's H1 earnings being 7% above HSBC's original expectations.

Meanwhile, Bocom is still "Sell" (target hiked to 2.40 hkd) despite saying Xtep's recent margin pressure was "less than expected."

Finally, JPMorgan says 2013 will be a "difficult year" for the sector, as is keeping its "Underweight" call on Xtep (target hiked to 2.30) while also saying the sportswear firm's revenue and profit have shown "stable growth" of late with "stable" gross margins and A&P expenses as well.

Xtep is currently trading at around 2.86 hkd.

See also:

TWO LEFT FEET: China Sneaker Play Li Ning Sees Dire Year

Houses Hike XTEP To ‘Outperform’, 'Buy'; GIORDANO Target 15% Upside

XTEP Orders Lead Sector

XTEP: In It For The Long Run With Marathon, Social Media