|

On 8 Jan 2026, China Aviation Oil (CAO) announced its parent, China National Aviation Fuel Group (CNAF), will merge with Chinese global energy giant Sinopec Group.

The big question for investors: could this trigger a General Offer (GO) that surfaces the hidden value in Singapore-listed CAO’s books? CAO supplies jet fuel across China, trades oil products globally, and owns stakes in major airport fuel joint ventures (notably at Shanghai Pudong). |

||||

The CGS report is the first among brokers after the Jan 8 merger news:

|

Research house |

Call |

Target price for CAO |

|

DBS Research |

Buy |

$1.75 |

|

CGS International |

Add |

$2.63 (previously $1.45) |

|

OCBC Investment Research |

Buy |

$1.50 (previously $1.40) |

|

Phillip Securities |

Buy |

$1.50 (previously 90 cents) |

CGS analysts Tan Jie Hui and Lim Siew Khee explain the takeover financials: “In the event of a GO, valuation becomes critical. A meaningful portion of CAO’s balance sheet — particularly its associate stakes — is carried at historical cost.”

CGS notes a reassessment “introduces a credible pathway for value crystallisation — particularly if balance sheet assets are marked closer to intrinsic value rather than historical book cost.”

That revaluation could be game-changing.

CAO sits on US$508 million net cash (about S$0.59 per share) plus undervalued associate stakes.

From a 10x FY27F P/E approach, CGS has switched to a sum-of-parts (SOP) valuation to capture this better.

The bull case is exciting. CGS writes: “Under our bull case, positioning China Aviation Oil (CAO) as a dedicated international fuel trading platform… could lift volumes by up to sixfold, unlocking material operating leverage and earnings upside.”

Unipec trades roughly 110 million tonnes of third-party crude annually; CAO does far less.

If CAO inherits even part of that flow, margins could expand sharply.

In this scenario, CGS’s SOP valuation hits S$3.76 per share — nearly double the current S$1.92 level.

CGS International Sum-of-Parts Valuation for China Aviation Oil

|

Component |

FY26F Profit |

P/E |

Base Case |

Bull Case |

|

Oil Trading (Core Business) |

46 |

11x |

508 |

508 |

|

Associates (mainly SPIA) |

57 |

13.5x (50% discount to Shanghai Int’l Airport) |

767 |

1,534 (27x – in line with Shanghai Int’l Airport) |

|

Net Cash |

– |

– |

508 |

508 |

|

Total Equity Value |

– |

– |

1,783 |

2,550 |

|

Per Share (US$) |

– |

– |

2.07 |

2.96 |

|

Target Price (S$) |

– |

– |

S$2.63 |

S$3.76 |

|

Implied FY27F P/E |

– |

– |

15.4x |

25.3x |

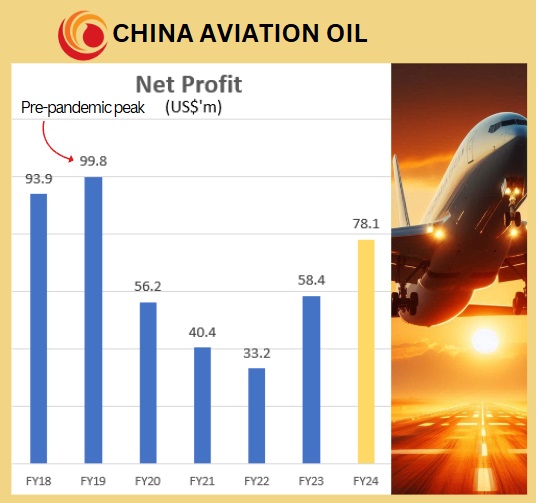

Operationally, the recovery of CAO is already strong.

Tan Jiehui, analyst"Reiterate Add, with a higher TP of S$2.63, based on Sum-Of-Parts to better capture CAO’s intrinsic equity value amid potential parent merger developments." Tan Jiehui, analyst"Reiterate Add, with a higher TP of S$2.63, based on Sum-Of-Parts to better capture CAO’s intrinsic equity value amid potential parent merger developments." |

“We expect CAO to deliver a strong FY25F net profit of US$102m (+31% yoy),” CGS forecasts, “underpinned by higher associate contributions driven by increased domestic and international flight activity.”

They highlight “strong net profit of US$52m [in 2H25F], supported by robust outbound traffic growth, higher associate contributions, and resilient margins.”

China-Japan flight tensions could slow FY26 growth, but aviation demand and sustainable aviation fuel (SAF) trading provide longer-term tailwinds.

With a new S$2.63 target, the analysts are clearly bullish on the opportunity. Of course, risks remain. In CGS' bear case, CAO could be quietly absorbed into Unipec without a GO and reduced to an “execution-only desk” with weaker margins. |

|||||||||||||||

See also another company with loads of cash: CHINA SUNSINE: Why 2026 Is Start of Long "Cash Harvest" Season for This Company