|

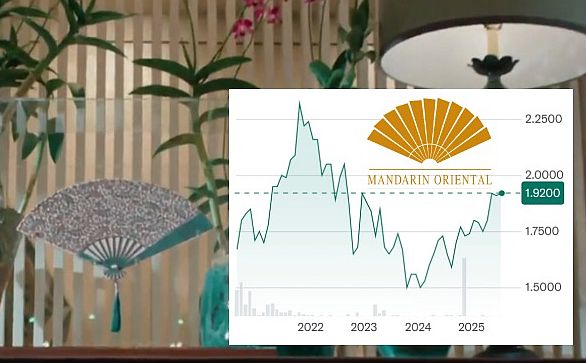

Will fund managers deploying the Monetary Authority of Singapore's billions discover a US$2.4 billion market company among undervalued quality ones?

|

Recent developments—including stake increases by its parent, a transformative property redevelopment, and a robust financial position— could well catch the eye of fund managers tasked to deploy S$5 billion under the MAS' so-called Equity Market Development Programme.

Firstly, the striking increase in Jardine Matheson Holdings' stake in Mandarin Oriental is seen in this table:

|

Year of Jardine Matheson Annual Report |

Stake in Mandarin Oriental |

|

2024 |

88.0% |

|

2023 |

80.2% |

|

2022 |

79.5% |

|

2021 |

79% |

|

2020 |

79% |

Jardine now owns 88%, a whisker below the 90% threshold for a compulsory takeover offer.

With such dominance, why bother maintaining a public listing?

As a private entity, it will be spared regulatory overheads which are not small as Mandarin Oriental has a secondary listing in Singapore and Bermuda and a primary listing in London.

The case for privatization is bolstered by past thin trading in Mandarin Oriental's stock on SGX as well as the other venues.

Back in 2021, Jardine Matheson privatised Jardine Strategic after its stake in the latter reached 85%.

The US$33 a share takeover offer was at a 20% premium to the pre-offer price.

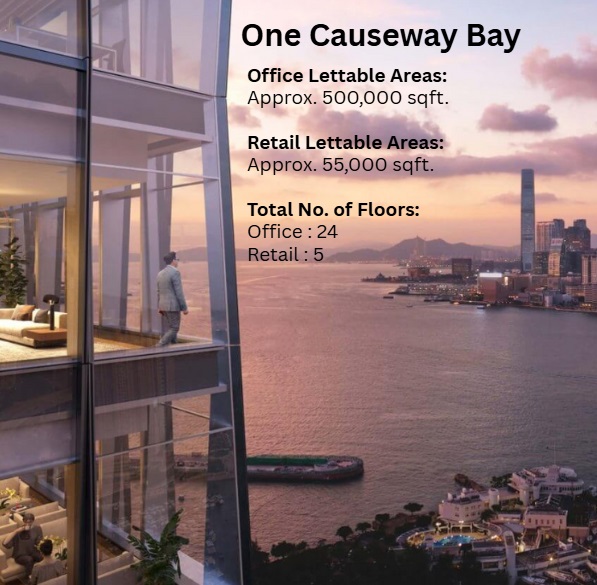

Not too generously, the offer was at a sharp discount to the US$58.22 NAV, sparking shareholder lawsuits and criticisms from many, including academic Mak Yuen Teen.  One Causeway Bay will be completed this year, rising from the site where the Excelsior Hotel once stood as a major landmark of Hong Kong’s colonial past.

One Causeway Bay will be completed this year, rising from the site where the Excelsior Hotel once stood as a major landmark of Hong Kong’s colonial past.

A new key pillar of the story of Mandarin Oriental is the redevelopment of its former Excelsior Hotel site in Hong Kong's Causeway Bay.

The hotel was demolished in 2019 to make way for a new Grade A office-retail building, One Causeway Bay, which was scheduled to be completed by 2H2025.

Being non-hospitality related, it is a non-core asset for Mandarin Oriental, which could divest it, unlocking substantial value for shareholders. The timing of it is uncertain as the Hong Kong market is anything but buoyant.

The carrying value of this development at US$2.1 billion—almost equal to the current market cap of Mandarin Oriental.

In the time that Mandarin Oriental keeps it, One Causeway Bay will generate a new income stream.

| Some key FY2024 figures |

| • Underlying profit after tax was US$75 million in 2024 compared to US$81 million in 2023. • Non-trading losses of US$153 million primarily comprised a non-cash revaluation of One Causeway Bay – the Group’s redevelopment site in Hong Kong, resulting in a loss attributable to shareholders of US$78 million. |

On the money side, investors will note that Mandarin Oriental has a low gearing at 2% of adjusted net asset value, achieved through divestments of some hotels.

As of December 31, 2024, consolidated net debt stood at US$94 million, with adjusted net assets at US$4.4 billion.

Revenue grew 13% to US$2.1 billion in 2024, driven by RevPAR increases and management fee expansions.

The stock is trading at a discount to revalued NAV (RNAV) of US$3.50 per share, which will appeal to value investors.

At the same time, they would be hoping that should Jardine Matheson make a bid for Mandarin Oriental, it would be at a fairer premium that when it privatised Jardine Strategic.

|

So, Mandarin Oriental seemingly stands at a cross-roads. |

Read also about this renowned hospitality chain: BANYAN GROUP's Share Surge: Why Phuket Property Focus will Add More Fuel Ahead ...