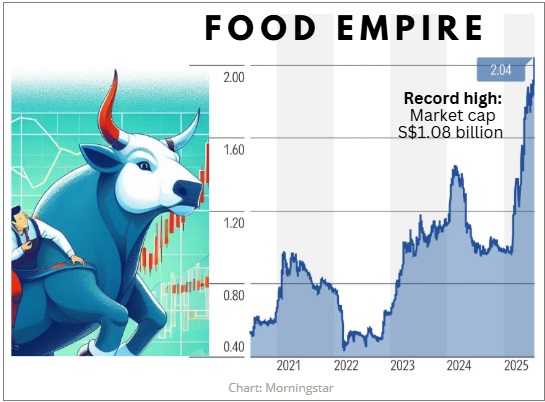

• Food Empire was listed on the Singapore Exchange in 2000. Despite winning awards for brand value and its strong international presence, the company did not receive much love from the market for much of its history. After growing its Asian business substantially and expanding its manufacturing base, Food Empire has suddenly found new fans. It was a little at a time and then all at once! The stock is +100% year to date, this year being its 25th year of listing. It has achieved a market cap now above the $1-billion level for the first time in its history, which will put it on the radar screen of more fund managers.  • Analysts have been advocating for the stock. In January 2025 when it was trading at 99 cents, CGS International gave it a target price of $1.53, the highest among analysts covering the stock. Just half a year later, CGS bumped it up to $2.28 recently. Now, not to be outdone, UOB Kay Hian has a new target: $2.40.  • UOB KH highlights that Food Empire is opening new factories in multiple countries and is benefiting from changing coffee trends among younger consumers. This, along with a reputation for strong brands in key markets, is helping boost its financial outlook and investor interest. • Well, all the buzz now is pointing to positive 1H2025 results to be released in August. Read more below ... |

Excerpts from UOB KH report

Analysts: John Cheong & Heidi Mo

Expect Healthy Growth And Outlook; Raise Target Price By 22% To S$2.40

We expect FEH to deliver 1H25 core earnings of S$27m (+14% yoy).

|

||||

Sudeep Nair has been CEO since 2012 while Executive Chairman Tan Wang Cheow is the founder of the Group and took the company public in 2000.

Sudeep Nair has been CEO since 2012 while Executive Chairman Tan Wang Cheow is the founder of the Group and took the company public in 2000.

| Expect positive outlook from strong brand equity and emerging trend for instant coffee |

• We maintain our positive view on Food Empire holdings (FEH) and expect it to achieve core earnings growth from ongoing investments in brand building as well as the market leadership positions of FEH’s brands.

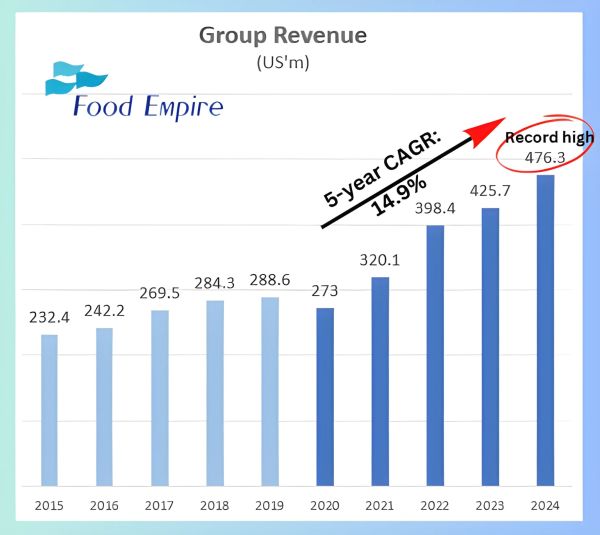

To recap, FEH has the largest market share in Russia and Kazakhstan, and is also a top three player in Vietnam. FEH’s strategic focus on Asia allows it to capitalise on high-growth emerging markets that have shown an increasing preference for good quality instant beverages that provide convenience and cater to busy lifestyles.

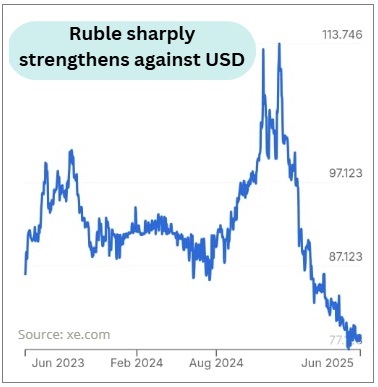

In addition, FEH is expected to benefit from tailwinds of falling coffee prices and a strengthening Russia Ruble.

Furthermore, we see rising popularity of instant coffee vs brewed coffee due to instant coffee’s convenience and affordability, especially among younger demographics and those with busy lifestyles.

Affordability is becoming a more crucial push factor with the recent increase in coffee bean costs.

• Strong expansion pipeline of four new manufacturing facilities to drive growth.

FEH has put in place a pipeline of four new manufacturing facilities from 2025-28:

a) 50% capacity expansion of a snack production factory in Malaysia, expected to commence production in 3Q25,

b) its first coffee mix manufacturing facility in Kazakhstan, expected to boost production capacity for coffee mixes by about 15%, targeted to start production by 2025,

c) a freeze-dried soluble coffee manufacturing facility in Binh Dinh Province, Vietnam, targeted to start production by 2028, and

d) 60% capacity expansion of spray-dried soluble coffee manufacturing facility to support its branded consumer business, expected to start production by 2028.

The Russian ruble has strengthened significantly from its Dec 2024 levels. This means Food Empire's revenue from Russia will be stronger on a USD basis, an important point considering Russia contributed 30% of revenue in 2024.• Supplemental agreement of REN will eliminate earnings volatility from 3Q25 onwards.

The Russian ruble has strengthened significantly from its Dec 2024 levels. This means Food Empire's revenue from Russia will be stronger on a USD basis, an important point considering Russia contributed 30% of revenue in 2024.• Supplemental agreement of REN will eliminate earnings volatility from 3Q25 onwards.

On 30 Jun 25, FEH entered into a second supplemental agreement for its US$40m redeemable equity note (REN) at a conversion price of S$1.09.

This will eliminate the need to mark the REN at fair value which will cause earnings volatility from 3Q25 onwards.

As the new agreement only takes effect from 1 Jul 25, we estimate that FEH will have to recognise a oneoff fair value loss of around US$20m in 1H25.

We believe that a negative share price reaction because of the fair value loss should be a good buying opportunity due to non-recurring nature of this event.

| STOCK IMPACT |

• In Vietnam, FEH will continue to invest in brand-building activities to keep up the growth momentum and further entrench its position as a market leader in the instant coffee-mix space. FEH has announced its plans to establish a freeze-dried soluble coffee manufacturing facility in Binh Dinh Province.

Construction of the facility is expected to commence by the end of 2025 and be completed by 2028. Together with the facilities in India, this will position FEH as a leading manufacturer of soluble coffee in Asia.

• In Malaysia, FEH has completed the expansion of its snack manufacturing facility in 1H25.

Commercial output from the new production line is expected to be ready in the third quarter, which will expand output capacity by approximately 50%.

Meanwhile, the newly expanded non-dairy creamer (NDC) manufacturing facility will also continue to increase production capacity utilisation.

• FEH expects the construction of its first coffee-mix manufacturing facility in Kazakhstan to be completed by end-25.

The new facility will boost the FEH’s total coffeemix production capacity by approximately 15% and allow it to expand its reach in Central Asia.

|

Full report here.