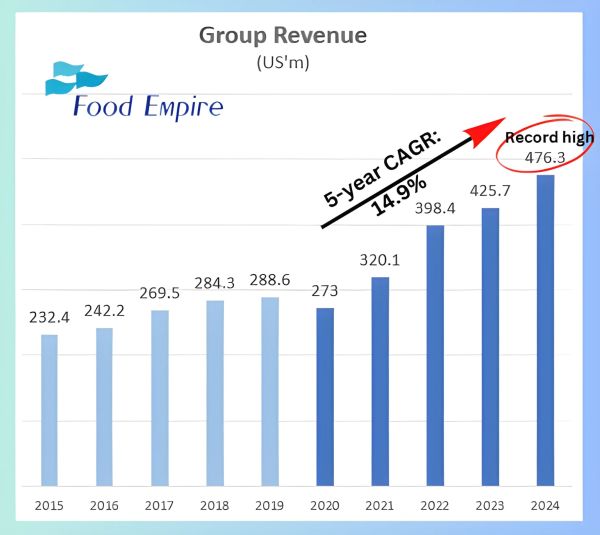

| Post-2024 results, we published: Surging coffee bean costs? No problem: This company has record sales, bigger dividends, and growth plan. It was largely reporting on Food Empire CEO's discussion with analysts and investors on the business performance and outlook. The company just posted record sales, announced bigger dividends, and laid out some solid growth plans. Their stock? Up a whopping 26% since their FY24 results were announced, jumping from $0.975 to $1.23 this week.  In this follow-up, we’re diving into what three analysts—UOB Kay Hian, CGS, and Maybank Research—are saying about the company. Spoiler alert: They’re all bullish on its future of Food Empire, which manufactures and distributes a wide range of instant beverages, snacks and ingredients. Below is a summary: |

| Similarities Between Reports |

1. Positive Revenue Growth

All three reports highlight Food Empire’s robust revenue growth in FY24, driven by strong performance in Southeast Asia and South Asia.

Southeast Asia grew by 27.3% year-on-year, with Vietnam being a standout contributor.

South Asia (ie India) also performed well, with a 24.9% YoY increase in revenue.

- Key Drivers: Food Empire's selling price adjustments to reflect higher coffee bean costs; its new product launches, and expansion into fast-growing markets like Vietnam and Malaysia.

2. Challenges with Margins

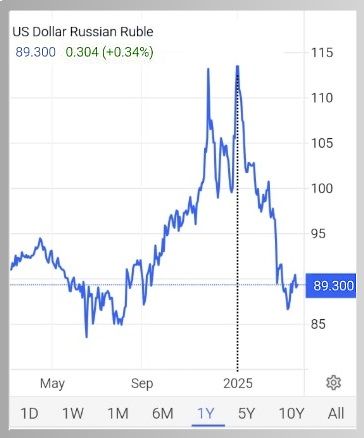

The analyst reports acknowledge profit margins are feeling the heat from pricier coffee beans, higher marketing expenses, and currency swings (the Russian ruble didn’t help).  The Russian ruble has strengthened significantly from its 4Q2024 levels. This means Food Empire's revenue from Russia will be stronger on a USD basis, an important point considering Russia's market size: It contributed 30% of revenue in 2024.But hey, the company managed to pass some of those costs to customers.

The Russian ruble has strengthened significantly from its 4Q2024 levels. This means Food Empire's revenue from Russia will be stronger on a USD basis, an important point considering Russia's market size: It contributed 30% of revenue in 2024.But hey, the company managed to pass some of those costs to customers.

3. Strategic Diversification

All analysts agree that Food Empire’s diversification strategy is paying off.

The company has reduced its reliance on Russia (historically its largest cash cow) by expanding into other regions like Southeast Asia, South Asia, and Central Asia.

- New production facilities currently being built in Kazakhstan (coffee-mix) and Vietnam (freeze-dried coffee) are expected to bolster growth further.

- The reports also note Food Empire’s investments in brand-building efforts across key markets like Vietnam.

4. Dividend Payout

The reports highlight Food Empire’s commitment to rewarding shareholders despite lower total dividends compared to FY23.

A final dividend of 6 Singapore cents per share and a special dividend of 2 cents were declared for FY24.

5. Upgraded Recommendations

All three reports recommend a "BUY" or equivalent rating for Food Empire due to its strong growth potential, strategic initiatives, and attractive valuation metrics.

| Differences Between Reports |

1. Target Price Projections

The target prices vary significantly across the reports due to differences in valuation methodologies:

Cafe Pho is Food Empire's best-selling instant coffee in Vietnam.UOB Kay Hian: Raised its target price to SGD 1.20 (previously SGD 1.10), citing stronger-than-expected revenue growth.

Cafe Pho is Food Empire's best-selling instant coffee in Vietnam.UOB Kay Hian: Raised its target price to SGD 1.20 (previously SGD 1.10), citing stronger-than-expected revenue growth.- CGS: Set a higher target price of SGD 1.71, reflecting optimism about Food Empire’s long-term growth potential in Vietnam and its food ingredients business.

- Maybank Research: Increased its target price to SGD 1.19, driven by expectations of margin recovery and continued growth in Southeast Asia.

2. Valuation Metrics

Each report employs different valuation multiples:

- UOB Kay Hian uses a price-to-earnings (P/E) multiple of 9x FY25F earnings.

- CGS adopts a higher P/E multiple of 11.2x FY25F earnings, reflecting greater confidence in Food Empire’s growth trajectory.

- Maybank Research uses an 8x FY25E P/E multiple.

3. Long-Term Growth Drivers

The emphasis on long-term growth drivers varies:

- UOB Kay Hian: Focuses on Food Empire’s expansion into Kazakhstan and Vietnam as key catalysts.

- CGS: Highlights potential re-rating catalysts such as improving operating margins, sustained market share in Russia, and resolution of the Russia-Ukraine conflict.

- Maybank Research: Stresses diversification efforts away from Russia and strong growth prospects in Vietnam.

|

Conclusion The three reports collectively paint an optimistic picture of Food Empire Holdings’ future prospects while acknowledging near-term challenges such as margin pressures from high coffee prices. |