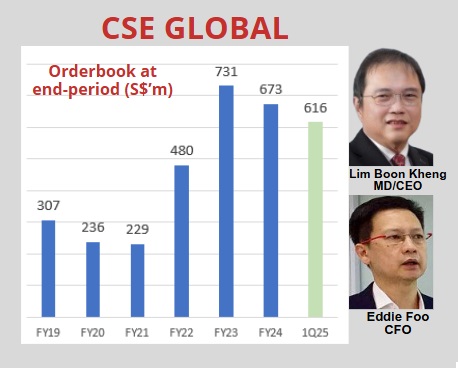

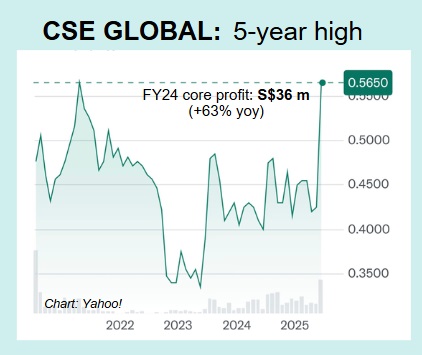

• CSE Global is a Singapore-based company that helps build and manage high-tech systems for industries like energy, public infrastructure, and data centres. Right now, CSE is in a great spot to grow, thanks to big trends like the proliferation of data centres, especially in the US. • CSE is engaged in projects that enhance electrical infrastructure, which includes working on substations, switchgear, switchboards, and transformers. These projects are crucial as power needs increase. • Outpacing other segments of CSE, the"electrification" segment has contributed to a strong orderbook for the group. See the chart and caption below.  Electrification segment accounted for S$329 m of the 1QFY25 orderbook. The other segments: Automation (S$56 m), Communication (S$155 m). Electrification segment accounted for S$329 m of the 1QFY25 orderbook. The other segments: Automation (S$56 m), Communication (S$155 m).• For sometime now, analysts have been noting that a growth driver for CSE Global is its "electrification" business. • The company could win big new projects in the US soon, says Maybank Kim Eng Securities in a new report that lifted its target price from 58 cents to 70 cents: "We believe CSE is gaining good traction with one of the largest data centre players in the US and is in the midst of qualifying for another 1-2 major customers." • For CSE (market cap: S$404 m, stock price 56.5 cents), that business has grown rapidly in the US, which contributed about two thirds of 1Q2025 group revenue by region. • But it’s not all smooth sailing—CSE faces challenges like supply chain hiccups, currency ups and downs, and the ever-present risk of project cost-overruns. • CSE counts Temasek Holdings as its No.1 shareholder (~23% stake) and the Singapore Government as one of its clients. Read excerpts of Maybank's report below .... |

Excerpts from Maybank KE report

Analyst: Jarick Seet

Multi-Year Breakout

Management is focused on expanding US capacity for these segments with a much larger facility being constructed. We believe CSE is gaining good traction with one of the largest data centre players in the US and is in the midst of qualifying for another 1-2 major customers. CSE is also well-placed to be one of the key beneficiaries of the Monetary Authority of Singapore’s (MAS) SGD5bn program. We lift our TP to SGD0.70, pegged to a higher 14.0x P/E from 11.5x FY25E due to its positive outlook |

|||||

| Reserving capacity for data centre/utility projects |

CSE’s 1Q25 orders fell 11.3% YoY to SGD155.3m, partially due to a weaker USD but also a strategic move to reserve capacity as management decided to focus on clients in the data centre and utilities spaces.

Margins are expected to remain resilient as management has ensured back-back pricing orders with suppliers to avoid any tariff shocks down the road.

Order wins are expected to pick up in 2H25, especially with data centre related projects in the US.

We are also expecting larger-sized orders to come from Singapore government-related projects.

| MAS SGD5bn scheme beneficiary |

With the Monetary Authority of Singapore (MAS) SGD5bn scheme set to be launched by year-end to boost liquidity and valuations of the Singapore market, we believe CSE will likely be one of the key beneficiaries, along with the Singapore SMIDs space.

As a result, we believe CSE’s valuations will likely increase.

This should be supported by the data centre space in the US, especially if it can win large-size orders in 2H.

We remain bullish on the outlook for CSE and see potential for a multiyear growth story. |

See full report here.