|

Excerpts from KGI initiation report

Analyst: Tang Kai Jie

Strong supply chain position presents growth potential

| Further expansion into Hainan. Zixin Group is expanding its sweet potato value chain from Liancheng County, Fujian, to Lingao County, Hainan, through a Revitalisation Project covering 8,961.33 hectares across 12 villages. This new land in Hainan is significantly larger than their original area in Fujian, offering substantial replication potential. Although currently in the initial stages, the group anticipates realizing profits from this expansion starting in FY2027. This strategic move marks Zixin's first replication of its model outside Fujian, demonstrating its growth ambitions in the agricultural sector. |

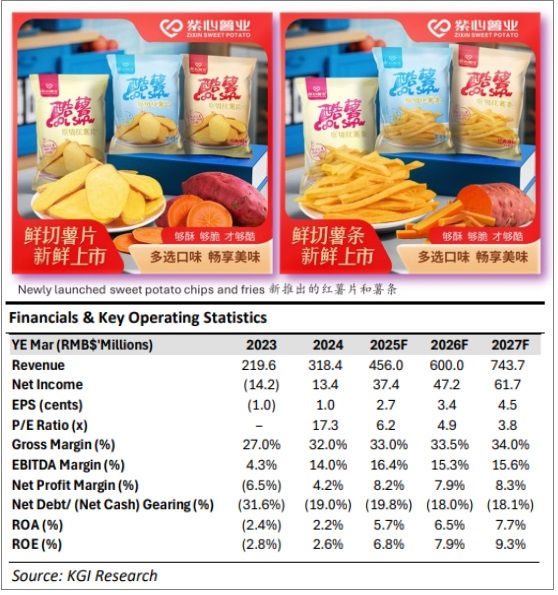

• Breakthrough in new snack products. Zixin Group recently announced that it has achieved a breakthrough in the production of sweet potato chips and fries snack products.

CEO Liang ChengwangThe company has begun to deliver the substantial orders received in February 2025 for these new products from its network of distributors.

CEO Liang ChengwangThe company has begun to deliver the substantial orders received in February 2025 for these new products from its network of distributors.

These products have also received significant demand, and Zixin has ramped up its production capacity at its existing snack manufacturing facility.

• Improving margins. Zixin Group saw an improvement in margins YoY in FY2024.

The company’s gross profit margin (GPM) rose to 32.0% in FY24, largely attributed to higher sales and lowered costs due to economies of scale. The company also recorded an operating profit margin (OPM) of 6.9% and a net profit margin (NPM) of 4.2%, highest in over 5 years, largely attributed to lower costs relative to revenue.

The company also recorded an operating profit margin (OPM) of 6.9% and a net profit margin (NPM) of 4.2%, highest in over 5 years, largely attributed to lower costs relative to revenue.

These improving margins showcased the initial results of Zixin Group’s integrated industrial value chain, which includes the supporting industry of cold storage warehousing services, enabling the company to recover from the post-Covid crisis and return to profitability.

• We initiate with an OUTPERFORM recommendation and a 12M target price (TP) of S$0.060.

1H25 financial results. Zixin Group Holdings reported total revenue of RMB156.7mn in 1H25, representing a 33.1% YoY increase, compared with a revenue of RMB117.8mn in 1H24.

|

Stock price |

2.9 c |

|

52-week range |

1.4-3.2 c |

|

Market cap |

S$46 m |

|

PE (ttm) |

9 |

|

Dividend yield |

-- |

|

P/B |

0.4 |

|

1-year return |

38% |

|

Source: Yahoo! |

|

The company continues to make strong progress on its integrated circular economy industrial value chain across business operations, driving significant and organic growth in financial performance.

Net profit after tax increased to RMB7.73mn in 1H25, compared to a net loss after tax of RMB3.40mn in 1H24.

The group’s basic EPS was 0.54 RMB cents in 1H25, compared to a loss per share of 0.25 RMB cents in 1H24.

|

Valuation & Action |

Risks: Environmental risks present a key operational challenge for Zixin Group.

The direct impact of variable weather patterns on sweet potato cultivation, coupled with the increased exposure from the extensive farmland, introduces significant yield uncertainty.

The risk of widespread disease outbreaks across its agricultural holdings further highlights the urgent need for comprehensive risk assessment and mitigation strategies to safeguard the company’s output and profitability.

Full report here

See also:ZIXIN's Sweet Potato Power: This Singapore Listco Excels, From Seedlings to Super Snacks