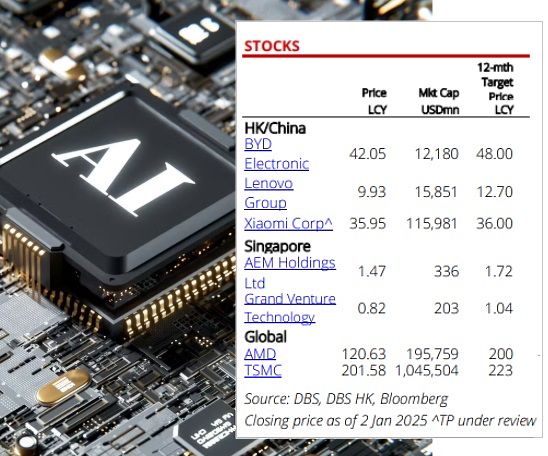

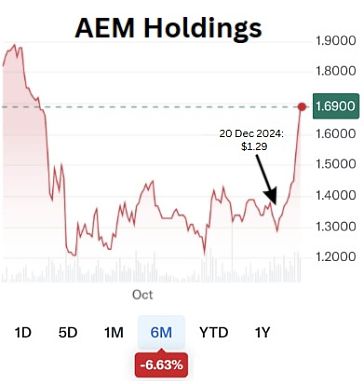

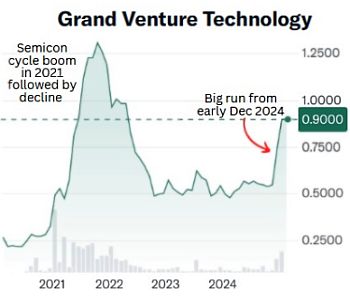

• The AI revolution is opening up a world of opportunities for invetors, and like 2024, this year is set to be an exciting year. • From the surging demand for AI-driven consumer electronics to the recovery in semiconductors, there’s no shortage of growth stories. Companies like Xiaomi and BYDE are riding the wave of emerging market expansion. Lenovo is poised to capitalize on the AI-enabled PC boom. • Meanwhile, Singapore's own AEM Holdings and Grand Venture are standing tall in advanced chip testing and production of semiconductor equipment. • With AI reshaping industries and emerging markets thriving, it’s a prime time to explore these dynamic investment avenues, as highlighted in a new DBS Research report.  • An update on AEM -- the stock has surged 30% from before Xmas 2024 to date -- from $1.29 to $1.68. It's its strongest run in a long time. GVT has run 56% in the past 4 weeks, from 55 cents to 86 cents, triggered by news it has acquired a new client followed by a DBS upgrade of the target price to $1.04. • Read excerpts from DBS Research's 10-page report below .... |

DBS analysts: Lee Keng LING, Fang Boon FOO, Amanda TAN & Jim AU

| Winners and losers in 2025 We anticipate multiple winners in the thriving AI market ecosystem as companies continue to monetise AI. |

Our picks: AI plays and downstream consumer electronics. Companies that straddle both the ongoing themes of AI and recovery should also be in a favourable spot.

We pick TSMC and AMD in this space. Our references in the downstream consumer electronic space are Xiaomi and BYDE, capitalising on the emerging market growth, and Lenovo, riding on PC replacements.

For SGX listed plays, we like AEM and GVT.

In the downstream space, our preferences remain Xiaomi, BYDE and Lenovo. The expected rise of AI-enabled devices and a wealth-driven shift in emerging markets in 2025 create distinct opportunities for the companies positioned to capitalise on these dynamics. Xiaomi is leveraging its strong brand recognition and large user base from its smartphones and AIoT products to build and cross-sell its EVs.

Xiaomi is leveraging its strong brand recognition and large user base from its smartphones and AIoT products to build and cross-sell its EVs.

Xiaomi (BUY, TP: HKD36.0 under review)

Its growing exposure to emerging markets, particularly India and Southeast Asia, highlights its potential to benefit from the feature phone-to-smartphone transition.

In 2Q24, its exposure to these regions rose to 13%, compared to 10% in 2Q24. This growth underscores Xiaomi’s alignment with rising disposable incomes and the increasing demand for higher-tier devices.

Xiaomi’s diverse product portfolio – from the affordable Redmi series to the mid-tier POCO and premium Mix/Fold models – positions it to cater to a wide range of consumer preferences.

With faster-than-expected shipment growth and an upward trajectory in ASPs, the company’s earnings are anticipated to increase 47.4% and 20.7% in FY25F and FY26F. We maintain BUY on Xiaomi.

Our TP of HKD36.0, based on a 28x FY25F PE, is under review.

BYDE (BUY, TP: HKD48.0)

The company stands out as a critical enabler of AI-driven smartphone adoption, playing a pivotal role in the supply chain for Apple’s AI-optimised iPhones.

As Apple continues to upgrade iPhone’s hardware to enhance the AI edge computing, BYDE is poised to benefit from the increased order volume, and improvements in ASP.

Additionally, its participation in Xiaomi’s supply chain further aligns it with the growth momentum in emerging markets. With FY25F earnings projected to grow by 48%, we maintain BUY on the stock with a TP of HKD48.0, reflecting a compelling valuation at 14x FY25F PE.

Lenovo (BUY, TP: HKD12.7)

The company’s leadership in the commercial PC segment makes it exceptionally well-positioned to capitalise on the upcoming replacement cycle driven by Microsoft’s discontinuation of Windows 10 support.

With the largest global market share in commercial PCs at 23%, Lenovo’s exposure to business customers places it at the forefront of this opportunity. Its robust AI PC pipeline in 2025, featuring models such as the ThinkPad, Yoga, and IdeaPad, aligns with rising demand for AI-enabled devices.

Forecasted AI PC shipment growth of 125.9% y/y in FY25 underscores Lenovo’s potential for accelerated earnings growth, with FY25/26F earnings projected to rise by 46.6%/ 45.0%, respectively.

These dynamics solidify Lenovo’s position as a key beneficiary of the AI PC boom.

We maintain BUY with a TP of HKD12.7, based on a 13x FY25F PE.

Chart: Yahoo!For SGX-listed plays, we favour AEM and Grand Venture, riding on the ongoing semiconductor industry recovery and increasing contribution from their new customers. Chart: Yahoo!For SGX-listed plays, we favour AEM and Grand Venture, riding on the ongoing semiconductor industry recovery and increasing contribution from their new customers. AEM (BUY, TP: SGD1.72) AEM is a pioneer in providing SLT (system-level test) solutions and is around one generation ahead of its competitors. Given its technological superiority, we believe AEM is well positioned to ride on the growing SLT market that has benefitted from the increased complexity of chips and higher test coverage requirements, alongside the need for advanced heterogeneous packaging. The group is at the cusp of a multi-year rollout for new customers. We foresee its customer diversification strategy yielding more significant returns starting from 1Q25. Current valuations are still undemanding at 15.8x PE on FY25F earnings, below -0.5SD of the historical mean, with further improvement to c.11x on FY26F earnings. Grand Venture (BUY; TP: SGD1.04)  Chart: Yahoo!Grand Venture is a high-growth company with a strong blue-chip customer base. Chart: Yahoo!Grand Venture is a high-growth company with a strong blue-chip customer base. In the semiconductor back-end space, it serves four of the top six; in the analytical life sciences segment, it serves three of the top 10. The products that GVT supplies are made according to certain product specifications, thus its customer base tends to be sticky in nature. We believe that FY24 is a turning point for the group with momentum to continue through FY25 as the semiconductor equipment market recovers and new front-end contributions come in more meaningfully. We have pencilled a 41% y/y increase in earnings, after a projected 73% y/y gain. |

Full report here.