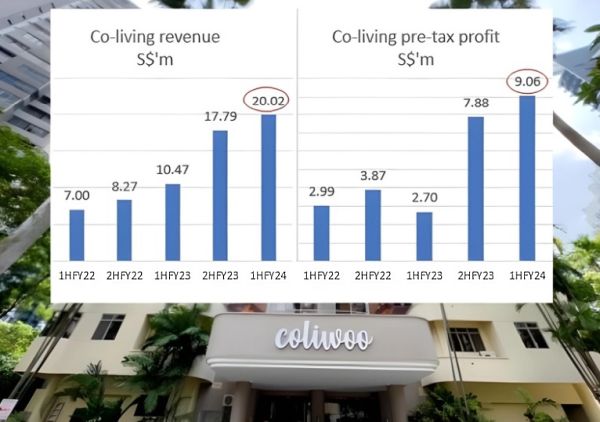

• It takes a while to grasp what is key to LHN's story, which is a promising dividend and growth one. LHN has its fingers in quite a spread of businesses but in the end, it's "space optimisation" that accounts for virtually all of its profit. It's essentially property management. • Out of its $15.3 million pre-tax profit for 1HF24 (ended March 2024), "space optimisation" contributed $14.4 million. That came from managing and renting out residential, industrial and commercial spaces. • Of that, the bulk came from the residential sector in the form of co-living homes, hostels, hotels, and serviced residences. Clients are mainly foreigners. In "co-living", multiple people (usually strangers to one another) live in a communal setting. In Singapore, co-living has picked up pace with LHN emerging as the No.1 player. Its business is branded as Coliwoo.  Co-living revenue (Singapore) accounted for 37% of LHN group revenue in 1H FY24 (ended March 2024). Compared to its other business segments, co-living (Singapore) is a relatively high margin business, accounting for 51% of group adjusted pre-tax profit. Co-living revenue (Singapore) accounted for 37% of LHN group revenue in 1H FY24 (ended March 2024). Compared to its other business segments, co-living (Singapore) is a relatively high margin business, accounting for 51% of group adjusted pre-tax profit.• Briefly, LHN's other businesses include managing carparks, providing cleaning services for properties, and operating EV charging points and solar installations. • Notably, LHN has one large industrial property development project whose units are currently being offered for sale. The sale is expected to contribute $10 million pre-tax profit of which 60% ($6 million) will be attributable to LHN -- which possibly will result in a special dividend for LHN shareholders. • With that corporate backdrop, read excerpts of Maybank's latest report on LHN below .... |

Excerpts from Maybank KE report

Analysts: Li Jialin & Eric Ong

LHN Ltd (LHN SP)

Operations on track

| 3Q24 business update; maintain BUY We attended LHN’s briefing yesterday following the release of its 3Q24 business update on 21 Aug 2024. Management guided for stable operations at its Coliwoo assets, supported by incremental demand from more tourists and summer-holiday makers. The average occupancy rate of its co-living portfolio edged up from 91.8% in 1H24 to c.95% in 3Q24, helped by competitive pricing and the newly launched River Valley assets as they continue to be ramped up. Two Coliwoo assets leased to the Ministry of Health and Holdings (MOHH) are expected to start contributing from Sep’24 onwards. Maintain BUY and TP of SGD0.43, based on an undemanding 6.5x FY25E P/E. |

Key takeaways of core business

LHN will launch 268 & 288 River Valley and two assets leased to the MOHH in 4Q24.

Projects in the pipeline in FY25 include Arab street (1H25) and the GSM building (3Q25).

Overall, LHN expects total number of keys to exceed 3,000 (+8%) by 2Q25.

LHN targets its food processing factory (55 Tuas South Avenue) to achieve a Temporary Occupation Permit (TOP) in Sep’24, and the subsequent sale of 49 strata units (saleable area of 112,000 sqft) over the next 6-12 months.

Management estimates SGD10m in pre-tax profit from the sale of the food factory.

LHN owns 60% stake of this development project.

Increasing renewable capacity

In 3Q24, LHN secured 3 solar energy contracts with a combined capacity of approximately 0.8 MW.

|

LHN |

|

|

Share price: $0.33 |

Target: |

Supported by an attractive IRR of 20-30%, management intends to build upon its existing capacity of 6MWs.

Despite the renewable energy market being competitive, management targets to increase solar energy capacity by 2 megawatts per year.

Dry powder and minor crosswinds

LHN divested its 40% stake in the Bukit Timah Shopping Centre car park in Jul’24 for estimated net proceeds of SGD4m (after offsetting bank loans), which will be used for working capital or strategic M&As.

Management is open to explore master lease opportunities in ASEAN, targeting around 200 keys.

LHN manages 2 carparks with over 800 lots in Hong Kong but may look to exit its loss-making operations in the city at end of the year due to the challenging macro environment.

LHN has a gearing of 58.1% as of 1H24 and 45% hedge-to-floating ratio, and hence, lower interest rates would benefit LHN.

Full report here.