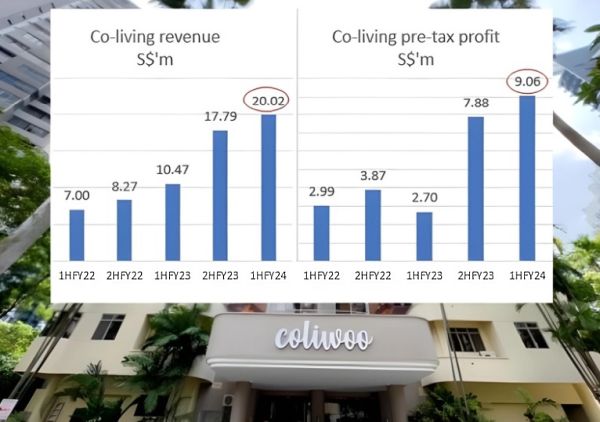

Coliwoo Orchard (above) is the largest co-living service apartment in the Orchard area. LHN has other more affordable offerings in other parts of Singapore such as Bugis, Balestier and Boon Lay. Coliwoo Orchard (above) is the largest co-living service apartment in the Orchard area. LHN has other more affordable offerings in other parts of Singapore such as Bugis, Balestier and Boon Lay.• "Co-living" -- imagine multiple individuals (usually expatriates, exchange students, medical tourists and younger Singaporeans) living together in a low-rise or even high-rise setting. In Singapore, co-living has picked up with LHN Limited expanding its co-living spaces and emerging as the No.1 player. LHN (market cap: S$137 million) manages and furnishes the spaces, providing a variety of amenities such as Wi-Fi and kitchens, and cleaning services and utilities. • Co-living revenue accounted for 37% of LHN group revenue in 1H FY24 (ended March 2024). Compared to its other business segments, co-living is a relatively high margin business, accounting for 51% of group adjusted pre-tax profit.  • The chart shows the steady growth in revenue and profit of the co-living business. Future growth will come mainly from more co-living properties, and LHN is busy developing that front. For details, read Phillip Securities' report below. • Maybe because the co-living business is a rarity among Singapore-listed companies, and thus not readily understood, LHN's stock trades at cheap valuations still. PE is 5.2 only. Dividend yield is juicy at 6%. And there is a massive 40% discount to book value. Read on ... |

Excerpts from Phillips Securities report

Analyst: Paul Chew

| Co-living profits tripled, more growth expected |

|

▪ 1H24 revenue was within expectations, but earnings exceeded.

▪ 1H24 adj. PATMI rose 25% YoY to S$16mn. Growth was driven by co-living revenue doubling and earnings tripled to S$9mn. |

||||

▪ We raised our FY24e earnings by 7% to account for the better-than-expected earnings from Coliwoo.

Our target price is raised from S$0.39 to S$0.42. We peg our valuations to 6.5x FY24e P/E, while the industry is trading around 13x.  Under CEO Kelvin Lim, some 20 years ago LHN ventured into master leasing unused and under-utilised industrial properties and refurbishing them to increase their net lettable area and rental yield. With that experience, LHN entered the co-living business some years back and it evolved into LHN's main business.We expect growth to remain stable for LHN in 2H24, supported by stable room rates.

Under CEO Kelvin Lim, some 20 years ago LHN ventured into master leasing unused and under-utilised industrial properties and refurbishing them to increase their net lettable area and rental yield. With that experience, LHN entered the co-living business some years back and it evolved into LHN's main business.We expect growth to remain stable for LHN in 2H24, supported by stable room rates.

FY25e will be a banner year of growth.

The number of keys in co-living will expand by at least 900 (187 in Coliwoo GSM Building and 700 healthcare professionals).

In addition, the sale of 49 food processing industrial units will be another one-off gain from the property development business.

We maintain our BUY recommendation. The Coliwoo franchise is scaling up and expanding into 3rd party management contracts.

The stock pays a dividend yield of 6% and trades at a PE of 5.2x and 40% discount-to-book value of S$0.55.

| The Positives |

+ Stellar earnings for Coliwoo. Co-living profit before tax tripled in 1H24 to S$9mn.

| FY25 banner year |

| "FY25e will be a banner year of growth. The number of keys in co-living will expand by at least 900 (187 in Coliwoo GSM Building and 700 healthcare professionals)." |

Revenue growth of 91% YoY to S$20mn was supported by 28% growth in keys to 2,151 and an estimated 70% jump in room rates to S$1,900 per month.

The commencement of the 411 keys in Coliwoo Orchard in Feb 23 was a major boost to room rates.

The residential rental index in Singapore is up 33% over the past 2-years but has started to stabilise.

| The Negatives |

- Weaker facilities management earnings. Facilities management earnings declined 32% YoY to S$1.7mn despite revenue growth of 14% YoY to $17.2mn.

The number of car parks under management rose from 74 (~20k lots) to 81 (~25k lots).

We believe the margin weakness was due to a loss of government grants. Nevertheless, the number of car park lots will grow with the recent contract award of another 900 car park lots.

| Outlook |

Coliwoo still the growth driver. We expect 2H24 earnings to be comparable to 1H24. Room rates for Coliwoo will be stable.

After a stellar rise in residential rents of 50% over the past 3-years (Source: URA), rents have started to move sideways. Nevertheless, the demand for co-living remains healthy.

Demand is now coming from corporate accounts as Coliwoo focus its marketing efforts on this segment.

Co-living is still more than 50% cheaper than hotels and still provides services (housekeeping) and amenities (cooking, laundry, broadband) to its residents.

Another driver is the increased number of residents in the country. In 2023, the population rose by 281,000 to 5.91mn, the highest annual increase on record and 6x the prepandemic average of 47,000.

LHN targets to grow co-living by 800 keys every year.

FY25 is a banner year. In 2025, there will be 2 large additions to the co-living sector – 700 healthcare professionals* and 187 from the GSM Building (3QFY25).  Paul Chew, Head of Research(*In January 2024, LHN secured a contract to provide accommodation to around 700 healthcare professionals at 100 Ulu Pandan Road and 60 Boundary Close. The contract is expected to commence in 2H24). Paul Chew, Head of Research(*In January 2024, LHN secured a contract to provide accommodation to around 700 healthcare professionals at 100 Ulu Pandan Road and 60 Boundary Close. The contract is expected to commence in 2H24).Another boost in earnings will be the property development project in 55 Tuas South to sell 49 units for the food processing industry. The expected launch is in 4QFY24. We maintain a BUY with a higher TP of S$0.42. Our valuations are pegged to 6.5x FY24e P/E, while the industry is trading around 13x. LHN is trading at 5.2x PE and a 40% discount to a book value of S$0.55. |

Full report is here.

See also: LHN: 2024 will be better year? Co-living portfolio to cross 2,000 keys?