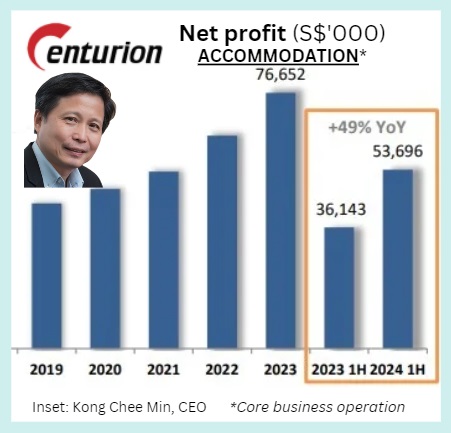

• Kong Chee Min, the CEO of Centurion Corp, has rare first-hand corporate leadership experience of a sunset industry and a sunrise industry. • He was its finance director and regional CEO. The company was then called SM Summit -- a Singapore-listed manufacturer of audio cassette tape, then CD-Roms and DVD-Roms. As the Internet era dawned, demand for those storage media would die off. • SM Summit then acquired a small business providing dormitories for workers' accommodation, renamed itself Centurion, and appointed Mr Kong its CEO. • That property management business targeting workers -- and then students as well -- has grown plenty. Today, Centurion owns and manages a portfolio of 32 accommodation assets totalling 66,495 beds as of 30 June 2024, including student accommodation. Centurion operates not just in Singapore but also Malaysia, the UK, the US, Australia, and China.  Centurion management at last week's results briefing (L-R): Ho Lip Chin, Chief Investment Officer – Accommodation Business | CEO Kong Chee Min | CFO Foo Ai Huey | Head of Corp Communications David Phey. Photo: Company Centurion management at last week's results briefing (L-R): Ho Lip Chin, Chief Investment Officer – Accommodation Business | CEO Kong Chee Min | CFO Foo Ai Huey | Head of Corp Communications David Phey. Photo: Company  Centurion's accommodation profit was turning up even through the pandemic.Centurion's stock has gained 65% since the beginning of this year (from 40 cents to 66 cents), as its 1H24 results extended a long-running profit streak (see chart). Centurion's accommodation profit was turning up even through the pandemic.Centurion's stock has gained 65% since the beginning of this year (from 40 cents to 66 cents), as its 1H24 results extended a long-running profit streak (see chart). With S$53.7 million net profit in 1H2024, excluding fair value gain on investment properties, it's on track to achieve more than S$100 million for the full year. • As the largest Purpose-Built Workers Accommodation (PBWA) provider in Singapore and Malaysia, Centurion is riding on high demand for foreign workers' living quarters. See: CENTURION: Homes for workers can't be built fast enough, so this company is enjoying a rental boom Centurion continues to increase the capacity of its workers accommodation and students’ accommodation. For UOB Kay Hian's latest take on the company, read excerpts below... |

Excerpts from UOB Kay Hian report

Analyst: Adrian Loh

Centurion Corporation (CENT)

1H24: Growth Outlook Undimmed For The Next Two Years

Centurion Corp delivered better-than-expected 1H24 core net profit of S$53m (+48% yoy), driven by strong occupancies and positive rental revisions across both its PBWA (Purpose-Built Workers Accommodation) and PBSA (Purpose-Built Students Accommodation) segments.

Target price upgraded to S$0.85. |

||||

• Robust growth in its PBWA and PBSA segments with strong occupancies. Both its PBWA and PBSA segments performed well with segmental profit growth of 35% and 37% yoy to S$46m and S$11m respectively.

CENT’s PBWA assets in Singapore are essentially full with 99% occupancy rate while those in Malaysia declined by 4ppt yoy to 90% due to asset enhancement initiatives.

The company’s PBSA assets in the UK had full occupancy at 99% (+9ppt yoy) while Australia registered 94% occupancy and is likely to hit full occupancy in the near term given that student arrivals in 2023 are set to be a new record for the country.  ASPRI-Westlite Papan: This Centurion worker accommodation is strategically located near Jurong Island, home to more than 100 global energy and chemical companies.

ASPRI-Westlite Papan: This Centurion worker accommodation is strategically located near Jurong Island, home to more than 100 global energy and chemical companies.

• Positive demand and rental rate outlook for PBWAs. In the near to medium term, CENT’s PBWA business in Singapore will continue to exhibit full occupancy given the construction sector’s robust spending in the next 3-5 years.

At its results briefing, management stated that its average rental rate per bed is around S$450-500/bed vs some rates at S$600/bed, thus implying some scope for positive rental rate reversions in the next 12-18 months.

One positive overlay is that in both Singapore and Malaysia, authorities have put in place higher housing standards for migrant workers, thus highlighting CENT’s assets in a positive light vs some of its smaller peers.

• PBSA expected to remain at healthy levels. Occupancy rates at CENT’s UK and Australian assets were at full or near full at 99% and 94% respectively in 1H24, with both geographic segments expected to remain high in the next 12-18 months due to lack of quality accommodation.

As a result, the company stated that it is continuing to explore new opportunities to expand its portfolio, either via development projects or asset light ones.

Management does not foresee new Australian visa regulations, which has materially increased visa fees, crimping demand for its PBSA assets.

• Solid balance sheet. For 1H24, CENT had available cash and banking facilities totaling S$91m.

The company continues to lower its gearing levels: at end-1H24, CENT had a net gearing of 34% vs 43% in 1H23 and 38% at end-23.

The company’s interest coverage ratio was 4.7x (1H23: 3.4x) with an average long-term debt maturity of five years.

EARNINGS REVISION/RISK

• Upgrading earnings. We nearly doubled our 2024F earnings to take into account the S$61m fair value gain on the company’s investment properties.

Earnings for 2025 and 2026 have been raised by 6% and 9% to account for the new bed capacities in Malaysia, Singapore and Hong Kong, offset by the sale of two assets in the US.

• Potential for higher dividend payout. CENT declared a 1H24 dividend of S$0.015, implying a 26% dividend payout based on EPS of S$0.0577 from its core business operations.

We have maintained our current forecast dividend of S$0.03 for the full year, but we believe that there is a high likelihood of an upside to S$0.035 given the strong earnings, implying a 2024F yield of 5.3% based on Friday’s closing share price.

VALUATION/RECOMMENDATION

|

• Maintain BUY with a higher PE-based target price of S$0.85 as we have rolled forward our valuation year to 2025. |

Full report here.