| China Aviation Oil has a very long history on the Singapore Exchange, having listed way back in 2001 and a few years later filing for bankruptcy on huge losses from speculative options trading. Soon after, it was resuscitated financially and led by a new board. The Covid pandemic dealt a blow to its business which depends on aviation travel but it looks set to regain ground from here on. |

Excerpts from OCBC Investment Research's 16-page initiation report

Analyst: Ada Lim

• China’s reopening resets the growth trajectory of its aviation industry

• Short-term demand recovery and long-term structural tailwinds in place |

|||||

Investment thesis

China Aviation Oil (CAO) is the largest physical jet fuel trader in the Asia Pacific (APAC) region. A key supplier of imported jet fuel in the civil aviation industry in the People’s Republic of China (PRC), CAO is a strong proxy to the growing Chinese aviation industry.

Although CAO’s financial performance has been battered in recent years by the pandemic and an extended period of lockdowns due to China’s zero-Covid policy, it is well positioned to capture the recovery in jet fuel demand with China’s reopening, given its entrenched presence in China and status as a market leader in the region.

Beyond this immediate catalyst, the increasing affluence of the APAC region and burgeoning middle class in China will support the long-term growth of the regional aviation fuel market, making CAO an attractive multi-year investment story.

Investment summary

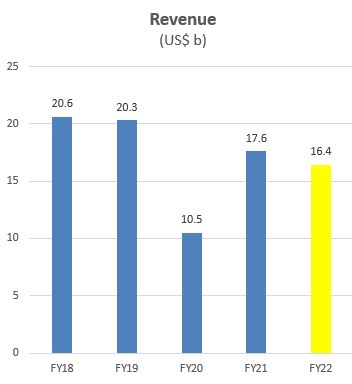

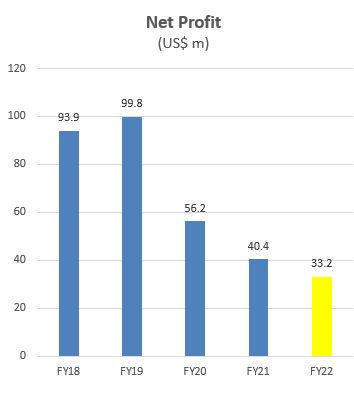

China’s aviation industry hit rock bottom in 2022 – CAO’s FY22 results were in line with consensus expectations. Total revenue fell 6.7% to USD16.4b on the back of a 40.6% decline in total supply and trading volume.  Share of results from associates also fell 24% to USD17.9m, mainly due to a 17.2% decline in contributions from Shanghai-Pudong International Airport Aviation Fuel Supply Company (SPIA), which struggled with lower refuelling volumes during protracted lockdowns in Shanghai.

Share of results from associates also fell 24% to USD17.9m, mainly due to a 17.2% decline in contributions from Shanghai-Pudong International Airport Aviation Fuel Supply Company (SPIA), which struggled with lower refuelling volumes during protracted lockdowns in Shanghai.

Total expenses rose 37.8%, driven by a USD2.8m increase in staff costs following the consolidation of CNAF Hong Kong Refueling Limited as a subsidiary.

Altogether, CAO reported a net profit of USD33.2m, down 17.8% from USD40.4m in FY21.

Altogether, CAO reported a net profit of USD33.2m, down 17.8% from USD40.4m in FY21.

It has proposed a final dividend of 1.6 cents per share (versus 1.9 cents per share in FY21).

China’s reopening should support near-term recovery… – With the relaxation of China’s zero- Covid policy, the release of pent-up demand for airline travel should translate to a significant rebound in the demand for jet fuel.

We expect recovery of air travel in China to be led by domestic flights in 1Q23, while international travel sees a meaningful rebound from late 2Q23 or 2H23.

At the same time, recovery in the broader APAC region remains supportive.

This will benefit CAO, whose top line is primarily dependent on its trading volume.

SPIA will be a key oil-related asset to watch out for, as it is the exclusive supplier of jet fuel and refuelling services at Shanghai Pudong International Airport (Pudong Airport), and contributed to ~59% of CAO’s net profits in FY2019.

… while structural tailwinds support long-term growth – (i) APAC is expected to lead the growth of the global aviation fuel market, with higher airline travel demand underpinned by the presence of many increasingly affluent developing countries in the region, as well as a burgeoning middle class in China.

CAO’s status as a market leader in the region positions it well to capture this growth over the next few years.

(ii) Airlines are increasingly transitioning towards sustainable aviation fuel (SAF), which is expected to contribute to 65% of the reduction in carbon emissions needed by the aviation industry to reach net-zero by 2050.

CAO is already looking to incorporate SAF into its product mix, which could potentially lend CAO a first mover advantage to capture demand from airlines in APAC.

Potential to deploy cash to augment growth– CAO has historically maintained a strong balance sheet and a healthy net cash position.

Given a slow but steady track record of acquisitions, we see potential for the company to deploy cash either to acquire new, synergistic oil-related business assets, or to expand its current operations in a manner that will be accretive to the company’s earnings – thereby unlocking further value for shareholders.

| Initiate coverage on CAO with SGD1.12 FV estimate– All things considered, we forecast a fair value estimate of SGD1.12 for CAO based on the Dividend Discount Model (DDM) methodology, with cost of equity elevated at 10.1% on the back of higher risk-free rates and country-specific risks, and a terminal growth rate of 2%. We assume that CAO’s jet fuel supply and trading business will recover to a conservative 55% of 2019 levels, as recovery may be clouded by geopolitical tensions weighing on tourists’ sentiments. CAO is currently trading at an elevated FY23 price-to-earnings (P/E) ratio of 10.3x, driven by investor optimism on the back of China’s reopening, even as earnings have yet to catch up. However, we still see further upside from current levels (based on closing price on 22 Mar 2023), given the supportive secular tailwinds in place. |

Potential catalysts

• Faster and stronger than expected recovery in Chinese air travel

• Deployment of cash through accretive acquisitions

• Introduction of initiatives to improve profitability

Investment risks

• Slower than expected reopening of China’s borders, or a reinstatement of zero-Covid policies

• Geopolitical tensions

• Regulatory risks