This article was recently published in the Let's Get Rich Together blog, and is reproduced with permission.

|

|

Notable clients

- Trump Tower, Las Vegas

- Burj Khalifa, Dubai

- Resorts World Sentosa

- Marina Bay Sands

- City Developments

- Capitaland

- Keppel Land - Reflections at Keppel Bay

- GoucoLand Limited

- Far East Organisation

- South Beach Mixed Development

- Westin Hotel, Marina Bay

These big names bodes well for DS' reputation, helping them to gain more clients in the future.

Valuations

Design Studio

PE ratio = 6.8

PB ratio = 1.2

Dividend yield = 11.8% (more on that later)

Kingsmen Creative

PE ratio = 11.5

PB ratio = 2.0

Dividend yield = 4.0%

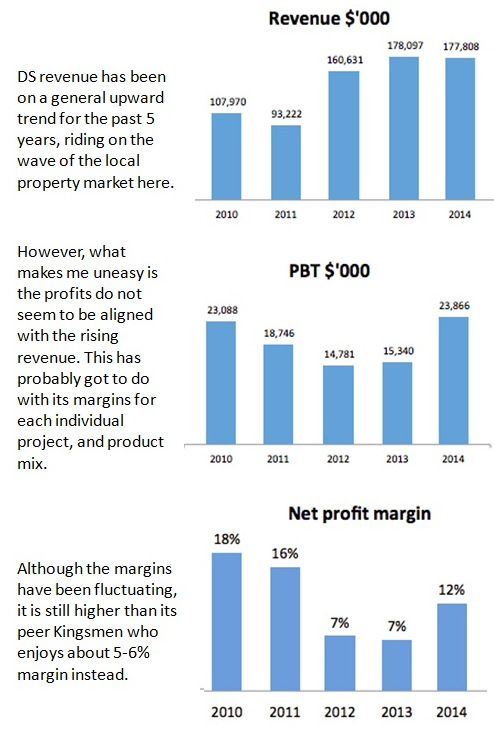

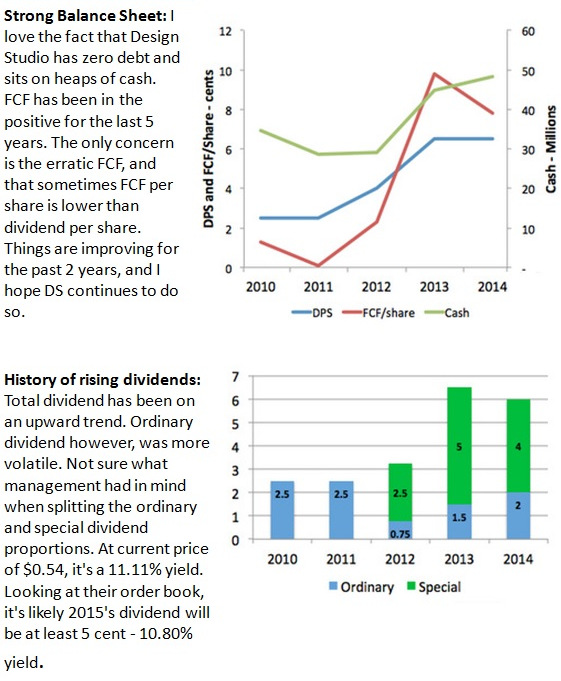

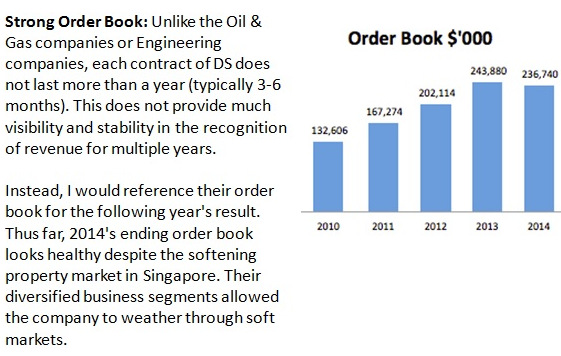

Past results

Business moat?

| Singapore interior fitting-out projects | ||

| Developer | Project | Location |

| MBS | Marina Bay Sands | Supply & installation of joinery to Tower 1, VIP suits and basement |

| RWS | Resorts World Sentosa Casino | Supply & installation of joinery including gaming & non-gaming tables & chairs |

| Pontiac Land Group | Capella Singapore | Supply & installation of interior fit-out solutions to hotel guest rooms, suites, villas & other public areas (except F&B outlets) |

| OUE | Meritus Mandarin | Supply & installation of interior fit-out solutions to the 5th and 6th storeys incl. lobby, specialty restaurants and bars |

Liquidity (or the lack of)

89.81% held by immediate holding company

10.19% held by public as at 11 March 2015

20 of the largest shareholder makes up 98.14% of the shares outstanding.

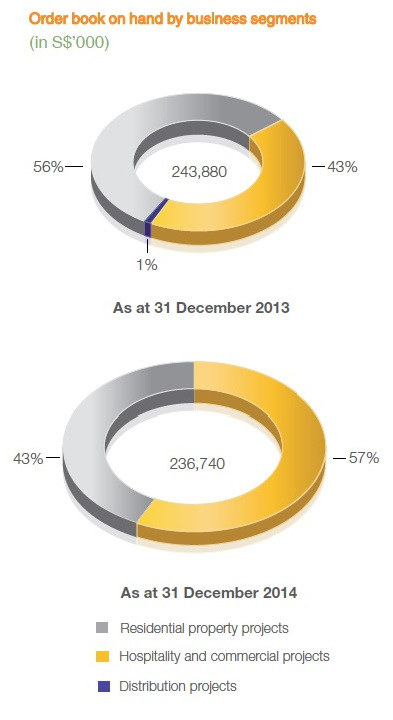

Dependent on property market

Residential segment takes up about half of DS' revenue. The softening property market will have adverse impact on the Group, as evident in the change in order book composition.

The uptick here is that the hospitality segment is poised to pick up the slack due to Singapore Tourism Board effort to spruce up Singapore and bring back the tourists here. New and existing hotels will be potentially DS' client for Alterations & Additions (A&A) services.

I was immediately interested when I found out the strong balance sheet and FCF ability they had in recent two years. I've initiated a small position with DS back then. Now that I've found out about their moat and past clients, I will probably add more to the position. I hope I'm right though.

I'm also watching out for that public float percentage.

Comments

- marginal Qtr profit growth against corresponding 2Q14

- order books remain solid

- interim dividend per share raised

Performance is impressive considering slower market conditions.

Am vested earlier in view of its established business model, rising order books and strong FCF and financial position. A quality stock and one should hold long term as high yield play..