Excerpts from JP Morgan's report

|

|

Commodities

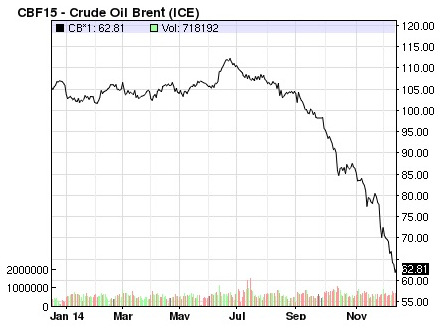

Commodities are down 23% YTD. Energy is down almost 40%, while the other sectors are relatively unchanged. The fall in oil prices is largely a supply story, in our view. On present estimates, physical global oil demand is tracking exactly what we forecast a year ago, while supply grew 300K barrels per day faster.

The excess supply is only 0.3% of world demand, but had many times this impact as a very price-inelastic demand side was met by a not-willing-to-budge supply side, as no country has so far cut production in the face of a collapse in prices.

The excess supply is only 0.3% of world demand, but had many times this impact as a very price-inelastic demand side was met by a not-willing-to-budge supply side, as no country has so far cut production in the face of a collapse in prices.

Weaker economic growth than expected, especially in EM, did result in weaker physical demand, but this was offset by a sharp increase in demand for strategic reserve building. The material increase in Libyan production over the summer was a surprise, and US supply also surprised on the upside, resulting in much reduced demand for African crude.

OPEC has not acted to cut output and thus we have seen the sharp fall in prices. We still think OPEC is more likely than not to act in Q1, but it is a very close call and there is no indication anything will change before next year. Thus prices will likely fall further and we stay short Brent.

OPEC has not acted to cut output and thus we have seen the sharp fall in prices. We still think OPEC is more likely than not to act in Q1, but it is a very close call and there is no indication anything will change before next year. Thus prices will likely fall further and we stay short Brent.