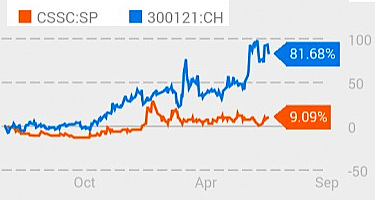

Relative performance of China Sunsine (stock code: CSSC) and Shandong Yanggu (stock code: 300121) over the past year. Sunsine has risen 9% but Yanggu has soared 82%.

Relative performance of China Sunsine (stock code: CSSC) and Shandong Yanggu (stock code: 300121) over the past year. Sunsine has risen 9% but Yanggu has soared 82%.

Chart: BloombergCHINA SUNSINE, listed in Singapore, is significantly lagging behind its Shenzhen-listed peer, Shandong Yanggu Huatai Chemical, in stock price performance (see chart).

Shandong Yanggu Huatai Chemical sports a trailing PE ratio that is worlds apart at 144. Susine's PE: 6.3.

This has impacted their market capitalisation: Shandong Yanggu is valued at S$476m (RMB2.38b) versus Sunsine's S$112m. See Google Finance page.

While the PE of Shandong Yanggu is out of this world, it largely suggests investor expectation of an enormous jump in the company's future earnings --- a prospect which is largely absent in the case of Sunsine, perhaps due to investors being unaware of positive industry happenings.

It doesn't help that there has been no Singapore analyst coverage of Sunsine for several years now, and the S-chip stigma has held back investors from getting overly enthusiastic about promising China stocks. Rubber accelerators in powder form at China Sunsine's factory. CBS is one of several types of accelerators made from MBT. NextInsight file photoShandong Yanggu is a much smaller company with an annual production capacity of 25,000 tonnes of rubber accelerators versus Sunsine's 75,000 tonnes. (Yanggu also produces anti-scorching agents, which have risen in price recently).

Rubber accelerators in powder form at China Sunsine's factory. CBS is one of several types of accelerators made from MBT. NextInsight file photoShandong Yanggu is a much smaller company with an annual production capacity of 25,000 tonnes of rubber accelerators versus Sunsine's 75,000 tonnes. (Yanggu also produces anti-scorching agents, which have risen in price recently).

Both companies are riding on a strong rise, which started in 1Q this year, in the price of rubber accelerators made from an intermediate product called MBT. This type of accelerator accounts for the bulk of accelerators produced.

Four Chinese broking firms, 国泰君安证券, 安信证券, 广发证券 and 中信建投证券 have put out reports highlighting the rising prices of MBT-based accelerators. See finance.sina.

The rise is directly attributable to shrinking MBT supply because many producers who cannot meet environmental regulations have been shut down by the government.The shortage has driven MBT prices up, from RMB 13,700 per tonne at the end of last year to RMB 17,500 in June this year. As a result, prices of accelerators have gone up.

The MBT shortage will last for a sustained period of time as it won't be easy for the producers to raise capital and obtain the know-how for installing the necessary environmental safeguards, according to analysts.

Here is the math for how Sunsine’s profit in 2Q may soar more than 100% year-on-year, as guided by some Sunsine investors.

1). Sunsine has an annual MBT production capacity of 45,000 tonnes, which is more than sufficient for its own needs to produce MBT-based accelerators. (This is unlike many other accelerator producers which depend on external suppliers of MBT).

With an aggregate 75,000 tonnes, Sunsine is the world’s largest rubber accelerator producer, accounting for 17% of world’s output. Its products are purchased by top tyre manufacturers such as Michelin and Yokohama.

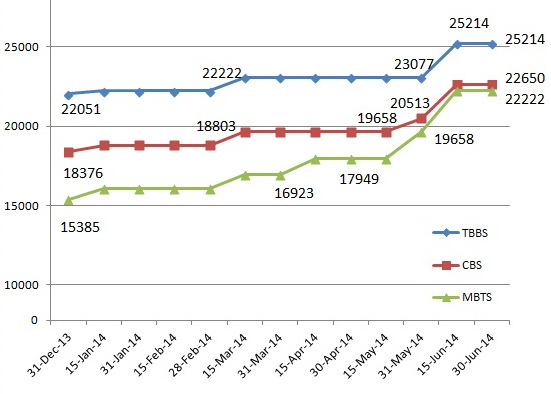

2). The following chart shows the recent (VAT-exclusive) prices of MBTS, CBS, and TBBS -- three types of accelerators which are produced using MBT -- charged by another competitor 山东斯递尔化工科技:

The price trends (in RMB per tonne) for MBT-based accelerators, especially the strong price spike in June, augur well for Sunsine's profit in 2Q2014 and beyond.

The price trends (in RMB per tonne) for MBT-based accelerators, especially the strong price spike in June, augur well for Sunsine's profit in 2Q2014 and beyond.

Data source: http://zgxcl.oilchem.net/x/p_281_110_553_0_1.html

Prices of non-MBT based accelerators have stayed stable.

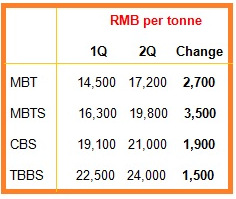

3). In 1Q, Sunsine sold 17,000 tonnes of accelerators, which was lower than the normal quarterly sales volume of 19,000 tonnes because of the Chinese New Year holidays.  Average product prices cited by 山东斯递尔化工科技. 4). If another 2,000 tonnes had been produced, this would have generated additional gross profit of RMB 10m (ie, 1Q ASP of RMB 19,300 X 2,000 tonnes x 26% gross margin [derived from GP margin of 19% for sales of 17,000 tonnes + 7% manpower cost & overheads that were incurred in the production of the first 17,000 tonnes]).

Average product prices cited by 山东斯递尔化工科技. 4). If another 2,000 tonnes had been produced, this would have generated additional gross profit of RMB 10m (ie, 1Q ASP of RMB 19,300 X 2,000 tonnes x 26% gross margin [derived from GP margin of 19% for sales of 17,000 tonnes + 7% manpower cost & overheads that were incurred in the production of the first 17,000 tonnes]).

5). Operating profit would have been RMB 8.9m after subtracting RMB 1.1m distribution cost.

6). RMB 6.7m would have been the net profit associated with the 2,000 incremental sales volume.

7). 1Q net profit on sales volume of 19,000 tonnes was theoretically RMB 29.5m (ie, 22.8 + 6.7m).

8). Assume 60% of accelerators produced is MBT-based ---> thus, 11,400 tonnes are produced. Conservatively, take lowest figure of RMB1,500 (see table) as the price change in 2Q for all accelerator products. Result: RMB17m pretax profit, or RMB13 m after-tax profit.

Thus, Sunsine's 2Q profit could be RMB 43 m (ie, adjusted 1Q profit of RMB 29.5m + RMB 13m arising from price changes in 2Q).

Not covered in this estimate: any one-off costs, or changes in the profits for other products (insoluble sulphur and antioxidants) of Sunsine, or any increase in the price of raw materials to produce MBT.

If Sunsine can record RMB43 m profit in 2Q, that would be 110% higher than the entire group's net profit of RMB20.5 m in 2Q of 2013.

We will know the outcome in about 4 weeks' time. Sunsine reported its 2Q results last year on 5 Aug.

Recent story: CHINA SUNSINE: Prospects brighten as green investments pay off

a lot of people are just waiting to dump when the price goes up

Hence, it makes sense to further increase its production capacity to seize greater market share :)

Why is this S chip different? Will the company "inflate" other costs to cover the profits?