Kevin Scully, executive chairman of NRA Capital. Photo: CompanyCEFC International reported its Q3-2013 results which showed a loss of RMB0.46mn.

Kevin Scully, executive chairman of NRA Capital. Photo: CompanyCEFC International reported its Q3-2013 results which showed a loss of RMB0.46mn. Key highlights of the results:

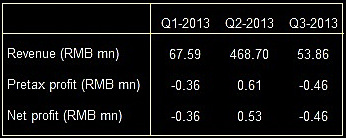

a) Revenue rose 452% to RMB53.9mn in Q3-2013 over 2012 but compared to Q2-2013 revenue fell 88.5%

b) The group reported a net loss of RMB0.46mn in Q3-2013 compared to a loss of RMB0.25mn in Q2-2012

c) The Group had negative shareholders equity of RMB1.24mn as at 30 September 2013

In its results commentary, the Group explained that the loss was due to insufficient sales revenue to cover fixed costs.

In its forward looking statement, the Group highlighted some of its futures plans:

"The Company continues to focus on its back-to-back oil trading business and the utilisation of its bank facilities.The Company is working hard to generate more revenue in the following quarter and to seek banks’ continuous support through increasing in the facility amounts. In addition, in order to diversify from the single back-to-back business model and product and achieve bigger profit margin for the Group, from October 2013, the Company has commenced trading in petrochemicals by entering into several trading contracts with suppliers and leasing several petrochemical bonded warehouses. The leased petrochemical bonded warehouses are located in China in order to be close to the Group’s potential China based customers and the China market. The Company is utilizing SPED, the Company’s controlling shareholder’s additional interest-free loan and its own working capital resources to finance those storage facilities. In addition, the Company is discussing with banks to seek additional bank facilities to further finance its petrochemical trading business. The Company is also exploring additional revenue streams, including investments in the energy sector through a wholly-owned Hong Kong subsidiary to be set up. It is intended that the US$300 million initial paid up capital of such new Hong Kong subsidiary will be financed by way of a new interest-free loan from SPED. The Board will keep the Shareholders informed of the progress of the incorporation and will make such further announcement as and when appropriate. The Group will comply with the applicable listing rules in connection with any investments in the energy section, including making the requisite announcement(s) and/or obtaining shareholders’ approval to the extent required under Chapter 10 of the Listing Manual of the Singapore Exchange Securities trading Limited.”

Commentary

CEFC’s results in 2013 have been volatile at the revenue level (see table on the right)

CEFC’s results in 2013 have been volatile at the revenue level (see table on the right)2013 can be considered a transition year for CEFC with the group being removed from the SGX Watchlist.

The company has also secured banking facilities of US$370mn.

I was expecting these facilities to convert into strong revenue with an average age of receivables of 2 to 4 weeks.

This has not occurred because as stated in the first line of item 10 above that they can only be used for back to back trading.

The Group needs more flexibility for its oil trading services to drive revenue to a more consistent level.

This plan to drive revenue from more oil trading activities is articulated in item 10 above which includes diversifying into petrochemical trading activities, renting oil storage facilities and moving more into the energy sector through a new Hong Kong subsidiary which will be capitalised at US$300mn.

As CEFC has negative equity of RMB1.2mn – the US$300mn investment in the new Hong Kong subsidiary will be financed via an interest free loan from its major shareholder for that amount. CEFC remains a concept stock at this stage.

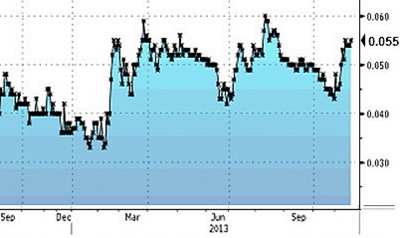

CEFC stock has attracted buying interset at 0.54 cent level since its 3Q results were announced. Source: BloombergThe Group has moved into the oil trading and energy space and needs time to execute its plans in this area which will hopefully be able to drive revenue and profit on a sustained basis.

CEFC stock has attracted buying interset at 0.54 cent level since its 3Q results were announced. Source: BloombergThe Group has moved into the oil trading and energy space and needs time to execute its plans in this area which will hopefully be able to drive revenue and profit on a sustained basis. The main risks remains execution, ie can the company execute its plans.

Existing investors can find hope in the huge financial support provided by the new major shareholder while potential investors if they are more risk averse can wait on the side lines until the Group delivers some success in its plans. I note some buying interest at the S$0.054 level in the share since it announced its results. Still on my radar screen as a turn around story.

Atlantic Navigation, one of my new Stock Picks, has announced that it will acquire two new vessels for US$28.7mn.

These acquisitions are important as Atlantic's current utilisation rate is in excess of 90% so it wil be hard to drive revenue and profit growth from just charter rate renewals.

One vessel is due for delivery in 2014 and the second in 2015. No impact from the acquisitions on 2013 earnings which remain intact.

The articles above were recently published on www.nracapital.com, and are reproduced with permission