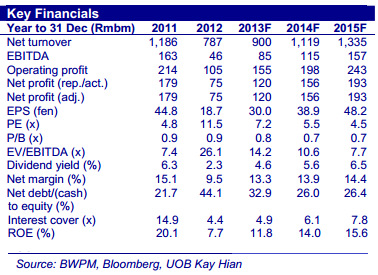

UOB KH says World Precision Machinery's "recovery has started"

Analyst: Jonathan Koh, CFA

World Precision Machinery (BWPM) benefitted from a recovery in the home appliances sector and a pick-up in the automobile sector. Orderbook has recovered from Rmb118m at end-Feb 13 to about Rmb180m at end-Mar 13.

World Precision Machinery (BWPM) benefitted from a recovery in the home appliances sector and a pick-up in the automobile sector. Orderbook has recovered from Rmb118m at end-Feb 13 to about Rmb180m at end-Mar 13.It secured a Rmb9.3m order for four highperformance high-tonnage stamping machines from an autoparts manufacturer who supplies specifically to Dongfeng Yueda Kia Motor.

It also secured a large Rmb20.8m order for 13 high-end stamping machines from Chongqing Baosteel Meiwei Wheel, the autoparts division of Baosteel Group, for delivery in 3Q13.

Share Price S$0.43. Target Price S$0.54  Workers insert steel plates into a WPM high-tonnage stamping machine customised for the automotive components manufacturer. Voila! Out comes autoparts such as truck doors (middle) and vehicle base plates (right) etc. NextInsight file photos

Workers insert steel plates into a WPM high-tonnage stamping machine customised for the automotive components manufacturer. Voila! Out comes autoparts such as truck doors (middle) and vehicle base plates (right) etc. NextInsight file photos

Recent story: WORLD PRECISION MACHINERY: Stronger China Boosting Prospects

OCBC raises United Envirotech's fair value to 90 c

Analyst: Carey Wong

Dr Lin Yucheng, CEO of United Envirotech.

Dr Lin Yucheng, CEO of United Envirotech.

NextInsight file photoUnited Envirotech Ltd (UEL) has recently inked an agreement worth RMB200m (S$40m) with the local government of Siyang County, Jiangsu Province, China for TOT (Transfer-Operate-Transfer) and BOT (Built-Operate-Transfer) projects in an industrial park for the textile industry.

Management intends to finance its latest investment using proceeds from the previous convertible bond issue to KRR and bank financing.

Based on its usual 40% equity/60% debt financing model, UEL would need around S$5.6m for Phase 1 of the TOT project, which should not be an issue as it is currently sitting on ~S$63.2m of cash (as at 31 Dec 2012).

In light of the latest investment, we bump up our FY14 estimates for revenue by 1.5% and earnings by 4.9%; this in turn raises our fair value from S$0.88 to S$0.90, still based on 13x FY14F EPS. Maintain BUY.

Recent story: MEMSTAR, UNITED ENVIROTECH: Sterling quarterly net profits