TECH STOCKS have been in play of late, especially in the first two months of this year.

Hard disk drive (HDD) manufacturers such as Seagate and Western Digital have spotted impressive year-to-date returns of 80% and 34%, respectively.

This optimism has also filtered to our Singapore-listed HDD component manufacturers such as Armstrong and Broadway, which have jumped 33% and 52%, respectively year-to-date.

In addition, most market watchers are expecting HDD players to rebound after the Thai flood last year. Coupled with the positive industry momentum, there are already a number of takeovers in the technology sector, such as Meiban and Adampak.

A proxy that comes to my mind is Singapore-listed Riverstone which counts as its customers the major HDD players such as Seagate, Hitachi, Western Digital, Toshiba and Samsung and semiconductor companies such as Infineon and Texas Instruments.

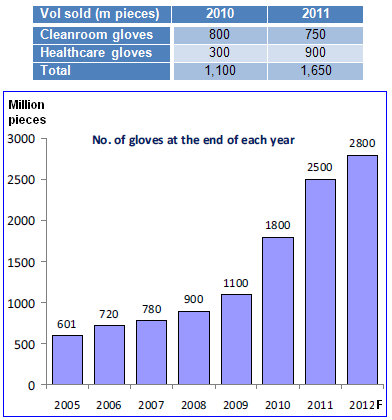

Riverstone's products are used in the HDD, semiconductor and healthcare industries. Although Riverstone has significantly increased its annual production capacity from 720m gloves in 2006 to 2,500m in 2011, it managed to generate positive free cash flow and has been giving dividends every year since 2006.

In fact, it has been in a net cash position since 2006.

As it seems to be a conservative, yet well-run, company, I arranged an exclusive meeting with Riverstone’s key management, namely Mr Wong Teek Son, the Executive Chairman and CEO, and Mr Lim Sing Poew, the CFO, to discuss their company's business and prospects.

Key takeaways from management meeting

Worst is likely over for HDD industry

The HDD industry went into a tailspin after the floods hit Thailand, the world’s largest manufacturing hub for HDDs. As the floods subsided and rebuilding commenced, demand is likely to pick up especially when there was a shortage of HDDs in 4Q.

Management postulated that demand is likely to resume in the second half as the industry continues to face some supply constraints in the first half of 2012.

Diversification to healthcare gloves bears fruit

Notwithstanding the flood in Thailand, Riverstone’s 4QFY11 revenue rose 20% from MYR60m in FY10 to MYR72m in FY11.

This was mainly attributable to higher sales for healthcare gloves which offset the lower sales in cleanroom gloves. This was a sound testament to management’s prescient move into the healthcare industry from 2009.

Its rapid expansion in the healthcare industry is noteworthy. Starting with zero pieces of healthcare gloves in 1QFY09, Riverstone produced 900m pieces in FY11 (see table on the right).

This was the result of a continuous focus on quality and R&D efforts. The company has a strong team of 20 chemists engaged in R&D work which provides highly customized solutions to customers.

Management also emphasized that the size of the healthcare industry is significant at around 150-200 billion pieces of gloves per year and growth is likely to rise approximately 10% per annum.

Capacity to increase to 2.8b pieces this year

Riverstone is adding three dipping lines at its Malaysian plants to raise the annual production capacity to 2.8b pieces of gloves in 2012 (see chart on the right). Furthermore, it is refurbishing old lines to increase the capacity per line.

Investment merits

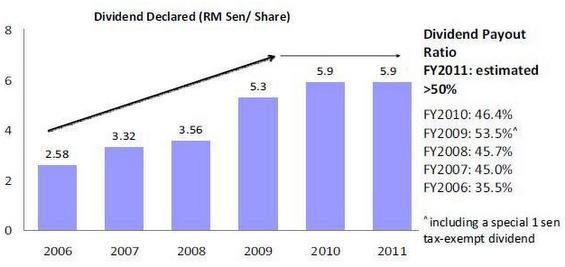

Management also shared with me the investment merits of their company. Firstly, notwithstanding the vagaries of their business cycles, management pointed to their consistent track record of paying dividends since 2006. At the current price of $0.440, FY11 dividend yield is around 5.5%.

Secondly, management added that 2012 would benefit from a full year impact of the expansion in capacity in 2011; average production capacity in 2011 was 2.0b pieces of gloves per annum compared to that of 2.5b at 2011 year end.

Thirdly, management is cognizant that they are small relative to their peers. However, management believes that being a small player has its benefits. They can service some customers with their customized solutions which Top Gloves may not find it worthwhile to. Furthermore, Riverstone, with its smaller base, is likely to grow faster than its peers.

Investment risks

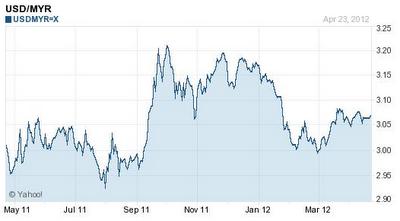

Management is candid about the challenges which they face in their business. Firstly, the volatile swings in the USD currency against MYR have an adverse impact to the company.

This is because about 60-70% of Riverstone’s sales are denominated in USD but only 40-55% of expenses are denominated in USD, thus the net portion is exposed to the fluctuations in USD/MYR.

Although management hedges the remaining exposure to a certain extent, the fluctuating USD does accentuate some challenges.

Secondly, according to The Malaysian Insider, Malaysia is seeking to announce a minimum wage policy by the end of the month, probably in the region of MYR800 & MYR900 for Peninsular and East Malaysia, respectively.

Labour costs in China are rising too. To mitigate such cost pressures, Riverstone is embarking on more automation and streamlining its manufacturing processes.

Thirdly, according to CIMB Research, fuel costs are on the rise as the previous gas subsidies amounting to a staggering MYR23b in 2011 are unlikely to be sustainable. To control costs, Riverstone commissioned a new biomass water tube boiler each at Taiping and Bukit Beruntung in 2011 and is seeking to achieve a balanced usage of biomass and gas.

Another noteworthy point is that Riverstone has about 48.97m warrants outstanding which can be converted to an equivalent number of Riverstone common shares at the exercise price of S$0.31 each.

The warrants expire on 4 Aug 2013. As the warrants are in the money, it is likely that they would be exercised, resulting in share dilution. However, these additional funds may prove useful for business expansion or other purposes, and may enhance shareholder value over the long term.

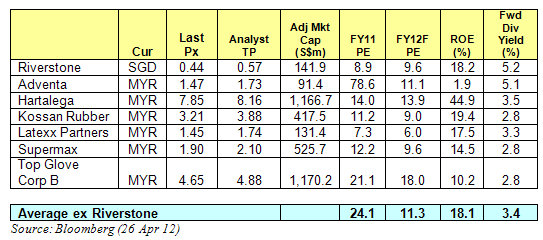

Valuations discount vs peers; higher estimated dividend yield

Riverstone seems to be trading at a slight discount relative to the FY12F industry average PE of 11.3x. It also has a higher estimated dividend yield of around 5.2% as compared to 3.4% for their peers. It will be interesting to see how they fare in the next few quarterly results.

Visit remisier Ernest Lim's blog http://www.ernestlim15.blogspot.com/