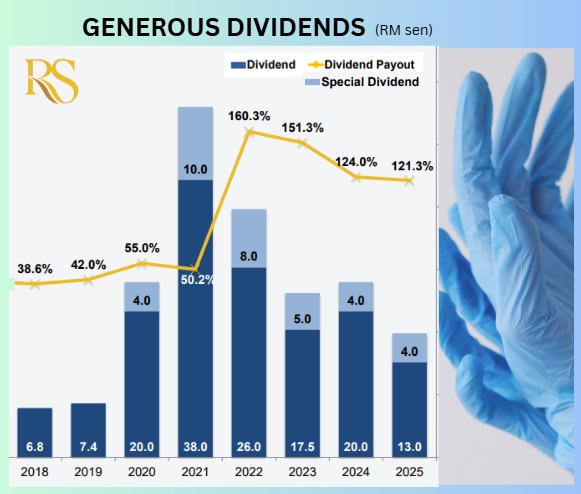

• Riverstone Holdings has a long history of paying dividends, reflecting its ability to generate high operating cashflow even when it invests in expanding its production capacity. In the FY25 results briefing, CEO Wong Teek Son said the company would give all of its yearly profits back to shareholders, as long as it doesn't negatively impact its day-to-day business.  • Interestingly, Riverstone also wants to continue to hand out special dividends and it describes an unusual way of approaching that. Management considers "depreciation" of assets (including operational machinery) as a loss of paper value for accounting purpose. • It treats the accounting entry (RM 71.5 million in FY25) as "extra cash" that it would give to shareholders as a special dividend. So that's how it is paying 121% of profits as dividends for FY25. The company would maintain a comfortable cash safety net (around RM600 million). • CGS International reckons FY26-28F yields would be a decent 5.6-6.6%. Read more below ..... |

Excerpts from CGS report

Analysts: William Tng, CFA & Then Wan Lin

■ RSTON’s FY25 revenue (RM995m) and net profit (RM208m) were in line with our full-year expectations. FY25 DPS at RM 0.17, a 120% payout.

■ Stronger yoy cleanroom sales expected in FY26-28F on robust demand from AI infrastructure and new customers, offset by strengthening ringgit vs. US$. ■ FY26-28F DPS of RM0.16-0.18 (100% payout) implies attractive 5.6-6.6% yields. Downgrade to Hold, with a lower TP of S$0.78 due to forex impact. |

|||||

FY25 results review: In-line results despite weaker yoy performance

Riverstone Holdings’ (RSTON) FY25 revenue was down 7% yoy to RM995m, while net profit was down 28% yoy to RM208m.  Wong Teek Son, Executive Chairman & CEO, Riverstone Holdings. FY25 revenue/net profit made up 100%/102% of our full-year forecasts, which we deem in line.

Wong Teek Son, Executive Chairman & CEO, Riverstone Holdings. FY25 revenue/net profit made up 100%/102% of our full-year forecasts, which we deem in line.

FY25 gross profit fell 23.4% yoy to RM298.7m, with gross profit margin narrowing 6.4% pts to 30%, mainly due to lower ASPs in generic healthcare gloves and unfavourable foreign exchange movement (strengthening ringgit against US dollar).

However, both cleanroom (CR) and healthcare (HC) segments still saw healthy volumes in 4Q25, which supported sequential sales growth, despite lower blended ASPs in CR segment due to product mix.

In addition, RSTON will transition to halfyearly reporting (from quarterly) from FY26F, with voluntary quarterly business updates. Expect robust CR growth and HC competition pressure to abate

During its FY25 results briefing on 26 Feb 26, management highlighted that the business still faces pricing pressure, particularly within the HC segment, alongside currency volatility and fluctuating raw material costs.

Nevertheless, management stays constructive on FY26- 28F prospects, supported by:

| 1) newly secured CR customers from China and other Asia markets that are expected to contribute incremental revenue profitability, and 2) intact CR demand in the US due to AI infrastructure. While HC gloves remain competitive, price undercutting has not been as intense as prior quarters, especially with competitors’ margins also affected by the US dollar depreciation. |

Given forex headwinds, we cut our FY26-27F EPS by 21-24% on lower revenue and GPM.

We downgrade RSTON from Add to Hold, with a lower TP of S$0.78, as we deem FY26-28F dividend yields of 5.6-6.6% attractive despite weaker earnings growth. We continue to value RSTON at a 15.9x P/E multiple on our FY27F EPS forecast, 0.5 s.d. above its 10-year (FY16-25) average P/E given its earnings exposure to higher-margin CR gloves (vs. its competitors) and management’s commitment to return excess cash earned during the Covid-19 pandemic to shareholders. |

Upside risks: stronger-than-expected glove demand recovery, especially in CR segment.

Downside risks: further weakening gross margins due to changes in product mix and a stronger RM against the US$ and lower tariffs for Chinese suppliers entering the US/Europe market.

→ See also: This Multi-Continent Business Delivers Record Revenue, Record Profit, Record Dividends, Record Stock Price

→ See also: This Multi-Continent Business Delivers Record Revenue, Record Profit, Record Dividends, Record Stock Price