Stamford Tyre FY2013 net profit up 18.5%, proposes 1.5ct dividend

Stamford Tyres President Wee Kok WahStamford Tyres has proposed to pay a first and final dividend of 1.5 Singapore cents after posting a 18.5% year-on-year (yoy) increase in FY2013 net profit of S$11.6 million.

Stamford Tyres President Wee Kok WahStamford Tyres has proposed to pay a first and final dividend of 1.5 Singapore cents after posting a 18.5% year-on-year (yoy) increase in FY2013 net profit of S$11.6 million.

The 1.5-cent dividend, unchanged from the previous year, amounts to a payout ratio of 30.6%.

The company’s earnings improvement for the year ended 30 April 2013 was mainly due to a one-off gain from the sale of an associate company and operating cost reduction efforts.

It recorded a one-off gain of S$11.9 million from the sale of its 20% stake in its China associate SRITP Limited.

Revenue dipped 3.5% yoy to S$351.2 million due to weaker tyre sales in Europe of its proprietary Sumo Firenza brand. This was mitigated by higher major brand sales in South East Asia and strong earthmover tyre sales in Indonesia.

Gross profit for FY2013 declined 8.6% yoy to S$72.5 million due to lower gross profit margin of 20.6% compared to 21.8% previously.

The decline in gross profit margin was due to the higher historical cost of goods sold during 1HFY13 compared to 1HFY12. 4Q2013 revenue was helped by strong strong earthmover tyre sales in Indonesia. Earthmover photo by Sim KihThe picture improved in 4QFY13 with gross profit margin rising 3.8 percentage points (compared to 4Q2012) to 23.6%, thanks to lower rubber prices and higher contribution from value-added services at its Stamford Tyres Mart retail chain and truck tyre centres.

4Q2013 revenue was helped by strong strong earthmover tyre sales in Indonesia. Earthmover photo by Sim KihThe picture improved in 4QFY13 with gross profit margin rising 3.8 percentage points (compared to 4Q2012) to 23.6%, thanks to lower rubber prices and higher contribution from value-added services at its Stamford Tyres Mart retail chain and truck tyre centres.

Net profit in that quarter was $5.5 million, up 48.6% year-on-year.

Stamford Tyres is one of the largest independent tyre and wheel distributors in Southeast Asia with distribution centres in Singapore, Malaysia, Thailand, Indonesia, Vietnam, Hong Kong, China, India, Australia and South Africa.

It has regional retail operations and provides on-site management services to fleet owners and mining operators. It also has a factory in Thailand for the manufacture of alloy wheels.

Related story: @ STAMFORD TYRES' AGM: Insights Into The Business And Real Estate Assets

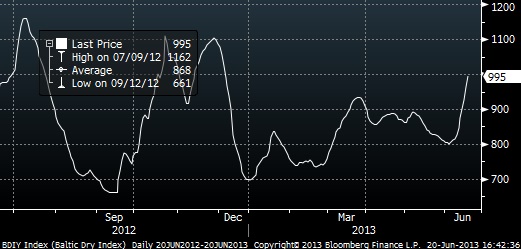

Expanding vessel fleet to boost Uni-Asia revenue Uni-Asia Chairman & CEO Kazuhiko YoshidaAT 995, the Baltic Dry Index is up by more than 40% over the past six months, as demand for dry freight is spurred by increasing production costs in China (by far the world’s largest market for iron ore).

Uni-Asia Chairman & CEO Kazuhiko YoshidaAT 995, the Baltic Dry Index is up by more than 40% over the past six months, as demand for dry freight is spurred by increasing production costs in China (by far the world’s largest market for iron ore).

This is good news for Uni-Asia Holdings, which took delivery of its 5th bulk carrier on 19 June through its wholly owned shipping unit Uni-Asia Shipping.

The 37,000 dwt handysize bulk carrier (M/V ANSAC PRIDE) was immediately deployed in a 5-year time charter to American Natural Soda Ash Corporation and will make immediate contributions to group earnings.

The bulk carrier was acquired in January 2011 and built by Japan’s Onomichi Dockyard.

“The vessel market is currently suitable for fleet expansion. Expansion of our charter fleet increases our profitability by building a strong recurring earnings base,” said Chairman and CEO Kazuhiko Yoshida. The Baltic Dry Index covers the costs of shipping via Handysize, Supramax, Panamax, and Capesize dry bulk carriers carrying a range of commodities including coal, iron ore and grain. Bloomberg data

The Baltic Dry Index covers the costs of shipping via Handysize, Supramax, Panamax, and Capesize dry bulk carriers carrying a range of commodities including coal, iron ore and grain. Bloomberg data

On 25 April, the company also inked deals to acquire another three vessels, also 37,000 dwt handysize bulk carriers, to be delivered during 2014 to 2016.

Group revenue in 1Q2013 was up 9% year-on-year at US$20.3 million, boosted by an increase in fee income and higher investment returns.

Vessel charter income contributed 17.1% to 1Q2013 group revenue, and was up 13.1% year-on-year at US$3.5 million.

Uni-Asia Holdings is an alternative investment company with investments in cargo vessels and properties in Japan, China and Hong Kong. It provides integrated services including vessel management and hotel operation, ship finance arrangement and broking.

Related story: UNI-ASIA HOLDINGS: Ship Charter Income Set To Rise