Translated by Andrew Vanburen from a Chinese-language piece in Securities Times

THE VALUE of property assets held of Mainland China’s top 500 real estate developers rose 50% year-on-year to nearly five trillion yuan.

So where did all this come from and what will the property barons do with it?

The land bank accumulation craze over the past couple years is the main reason for the sky high inventory values.

Meanwhile, real estate firms are hoping the “buyer’s market” that currently characterizes Mainland China’s property market will be a quick fix remedy.

Developers are lately looking to offload properties now rather than be stuck with them at lower market prices.

“Our realtors are likely to sell their plots without much hesitation now because there’s still a small profit to be made,” said a chairman of a Shanxi Province-based real estate firm.

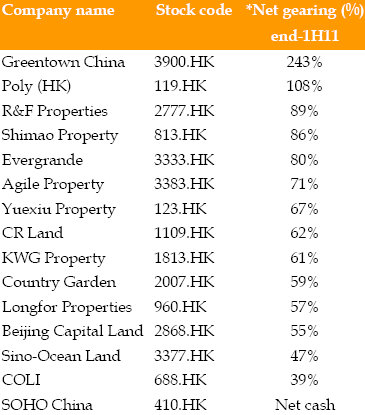

Guangdong Province-based Country Garden Holdings (HK: 2007) is also riding the flip-happy fiesta, a source with the Hong Kong-listed developer said.

The real estate firm reportedly has been one of the sector’s most aggressive sellers of properties of late, with realtors chasing still attractive returns on their sales and property shoppers lured by increasingly attractive buying incentives.

The geographic sales push for the developer is apparently concentrated around the Tianjin area and North China in general.

The overall impetus for the sector wide sales push across the country is the fear of excessive land bank accumulations by developers on an individual basis as well as rising debt burdens on balance sheets within the industry on the whole.

“The high gearing ratios for many developers and alarming inventory levels in the sector are both problems that are unlikely to be remedied anytime soon by a quick selloff of assets at any price,” said the general manager of a Beijing-based property consulting firm.

According to the most recent statistics available, the value of land banks sitting idle in the inventories of Mainland China’s top 500 property developers at the end of 2012 rose 50.34% year-on-year to 4.99 trillion yuan.

This represents a 6.5 percentage point increase rise over the previous year and represents an average of just under 10 billion yuan value per firm, a new record high.

Annual results released so far this year are also painting a grim picture of the inventory backlog burden for the country’s developers.

As of March 27, 32 property developers selling A-shares on the Shanghai and Shenzhen bourses have released their financial earnings statements.

Among these, 21 are reporting inventory increases over the 12-month period, or nearly two in three.

Additionally, seven of these 21 firms have seen an over 30% rise in the value of their land bank assets over the period.

China Merchants Property Development (SZA: 000024) saw its property assets value jump 33% year-on-year to 51.4 bln yuan.

China Vanke (SZA: 000002) saw its inventory shoot up an even more alarming 56% to 133.3 bln yuan, while Beijing Capital Development (SHA: 600376) endured a 72% rise to 43.0 bln yuan.

It is clear that this land bank accumulation and asset value creep is unsustainable over the long run, and in the context of this inventory burden it becomes evident why there is such a buyer friendly feel to the market of late.

See also:

"HK Housing Market To Fall Up To 15% This Year"

PROPERTY SURVEY II: Settling Down In Shenzhen

HK Property Initiated ‘Outperform’

Hong Kong Developers On PRC Bargain Hunting Spree