Excerpts from SIAS Research's report on Sapphire Corporation, which traded recently at 31 cents:

Sapphire Corporation Limited announced a strong set of FY10 results with operating profit, excluding one-off items, growing by 89.8% from S$5.9m in FY09 to S$11.1m in FY10.

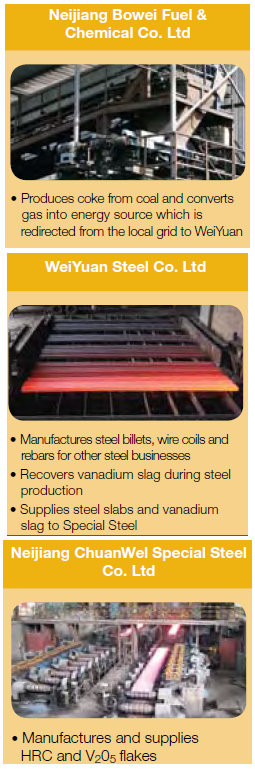

We expect Sapphire to maintain its strong growth in FY11 owing to a) a 42.9% increase in vanadium pentoxide (V2O5) production capacity and b) full year contribution from rebar processing for Weiyuan Steel Co., Ltd (Weiyuan). Maintain Increase Exposure based on an intrinsic value of S$0.600.

Fundamental Developments:

* Sapphire has increased its V2O5 production capacity from 3,500 to 5,000 tonnes per annum. It is also sourcing for more vanadium slag to facilitate further expansion. We are excited by these moves which has raised Sapphire’s growth visibility. We now expect revenue to grow by 25% to S$149.8m in 2011.

* The increased capacity will also yield the company economies of scale and improve profitability. As a result, we are projecting a reference 5% point increase in gross margin in 2011. Consequentially, net margin is expected to widen from 9.3% in FY10 to 16.3% in FY11F.

* Last month, Sapphire pledged its China Vanadium Titano-Magnetite Mining Company Ltd (CVTM) shares to Credit Suisse International (CSIN) as collateral to refinance some of its investments.

Under the agreement, Sapphire gained a) continued exposure to CVTM share price upside and b) an exit option via its right to repay the loan using the said CVTM shares from 2013. Notably, this resolves much of Sapphire’s funding needs without diluting existing shareholder value.

* To further enhance value, Sapphire proposed a dividend of 1 S cent per consolidated share for FY10 – its first pay out as far back as 2004. We view this decision as a signal of strong future growth and sufficient cash flows by Sapphire.

The full SIAS report can be accessed at http://www.sapphirecorp.com.sg/