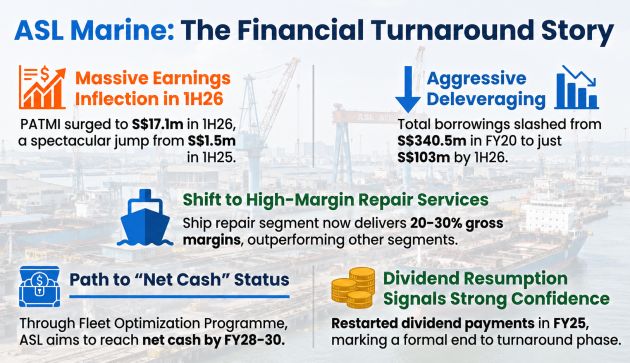

ASL Marine has come a long way since the offshore and marine downturn that began in the mid-2010s. Back then, weak charter rates, poor demand for offshore support vessels and troublesome shipbuilding contracts put heavy pressure on both earnings and the balance sheet. Since then, the tide has clearly turned. Revenue started recovering in FY2023, ship repair activity returned to more normal levels, charter utilisation improved and ASL became much more selective about the shipbuilding jobs it takes on. Just as importantly, the group has been working hard to cut debt through vessel sales and refinancing.

Source: Evolve Capital, company. Lower finance costs, stronger ship repair margins and better chartering performance lifted PATMI sharply, while the prospect of reaching a net cash position created a powerful rerating narrative.

Evolve Capital has just initiated coverage with a BUY rating and a S$0.42 target price. |

|||||||||||||||||||||||||||||||||||

Evolve’s initiation report answers a number of investor questions. Here are five:

1. Has ASL Marine’s turnaround genuinely been completed?

It examines whether the sharp profit recovery reflects sustainable operational improvement rather than accounting effects or one-off gains. Ang Kok Tian, Chairman and MD, ASL MarineEvolve argues that higher-value repair work, better charter utilisation and sharply lower finance costs show that the turnaround is real.

Ang Kok Tian, Chairman and MD, ASL MarineEvolve argues that higher-value repair work, better charter utilisation and sharply lower finance costs show that the turnaround is real.

2. How much more can earnings grow from deleveraging?

The report explains why profits can rise faster than revenue as debt and interest expenses fall.

Evolve forecasts PATMI increasing from S$14.6 million in FY25 to S$33.1 million in FY26 and S$42.6 million by FY28, despite relatively moderate revenue growth.

3. Can ASL successfully dispose of idle vessels and reach net cash?

This is central to the investment thesis.

Evolve assesses the fleet-optimisation programme, under which ASL plans to sell about 20–30 vessels, reduce its fleet from 181 to roughly 150–160 vessels and reach net cash around FY28–FY30.

"Management notes that a vessel typically takes around six months to sell, and finding buyers for its vessels is generally easy."

4. What will drive growth after the deleveraging benefits run out?

| Waiting for rerating |

| "We think the market continues to undervalue ASL Marine given that its deleveraging efforts are still underway. As management delivers, we opine that the market would rerate ASL closer to that of its peers." -- Ethan Aw, Analyst, Evolve Capital |

The report considers whether ASL can evolve from a balance-sheet-recovery story into a genuine growth story. The main potential drivers are:

-

sustained high-margin ship-repair demand;

-

a third floating dock expected to add 20–30% capacity around late FY27;

-

higher charter-fleet utilisation despite a smaller fleet; and

-

long-term reclamation, port and coastal-protection projects such as Long Island and Tuas Port.

5. Is ASL structurally less risky than it was during the previous marine downturn?

Evolve examines whether management has learnt from past mistakes.

ASL now focuses on smaller, standardised vessels with shorter delivery cycles, avoiding the large, highly customised shipbuilding contracts that previously left it exposed when customers cancelled orders.

Together with a leaner fleet, lower debt and a greater contribution from recurring ship-repair work, this suggests the company’s improved earnings are being built on a more resilient business model.

What is ASL worth, and what could prevent the rerating? |

→ See also:ASL MARINE From 6 cents to 33 cents in 6 months: This Company is Riding a Marine Wave

→ See also:ASL MARINE From 6 cents to 33 cents in 6 months: This Company is Riding a Marine Wave