|

There's a deep-value play in the Singapore energy and marine offshore sector, Baker Technology, a name rarely heard of among investment professionals and on investment-focused social media platforms. |

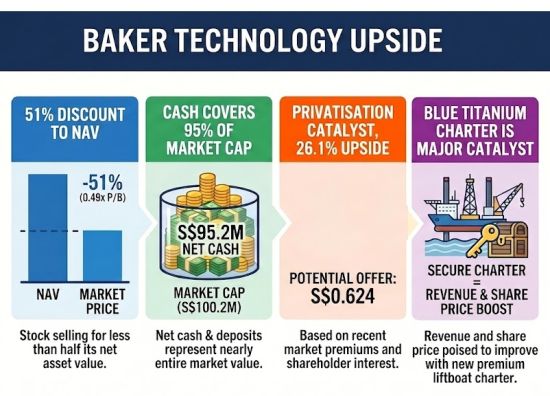

Not surprisingly, the share price (48.5 cents, - 12% in the past 1 year) has been lacklustre in a bull market.

BTL is trading at a Price-to-Book (P/B) multiple of just 0.49x.

Analyst Calvin Mau notes, "BTL’s cash & short-term deposits (netting the loans & borrowings) were S$95.2 million... or 95.0% of BTL’s market capitalisation of S$100.2 million as at 22 May 2026".

Given this cash hoard, he points toward a buyout scenario led by former CEO Dr. Benety Chang, who currently holds an estimated 56.0% total interest in the company.

(Dr Chang's daughter, Jeanette Chang, has been CEO of Baker Technology since 2019 while the father is CEO of Baker's listed subsidiary CH Offshore since 2018).

Mau states, "Based on the average price premium of privatisation offers for SGX-listed companies over the last twelve months, we estimate that any privatisation offer may need to have a price premium of 26.1% from the current share price of S$0.495 to be successful".

That places the necessary minimum buyout offer at S$0.624, which the analyst adopts as the target price.

| Catalysts for Growth Beyond a Buyout |

Even if a privatisation does not materialize immediately, BTL possesses multiple avenues to unlock shareholder value.

The analyst identifies several potent catalysts.

| The risks |

| "We recognise that our target price is subject to risks such as delays in rechartering the Blue Titanium liftboat, lower-than-expected rate for the Blue Titanium new charter, and upcoming expiry of property leases." -- FPA Financial |

First, an increase in global offshore commitments and rising crude oil prices could eventually drive up charter demand for their fleet.

Second, BTL is actively exploring a sale of the Blue Titanium liftboat.

Regarding this potential capital injection, Mau writes, "Should BTL manage to sell its liftboat, cash & short-term deposits may rise. Accordingly, BTL may raise DPS or increase share buybacks".

Of course, no investment is without risk. However, at its current valuation, the margin of safety appears substantial. |

→ See also:NORDIC: Cash-Positive Again and Piling Up $: What Are Growth Areas for This Company?

→ See also:NORDIC: Cash-Positive Again and Piling Up $: What Are Growth Areas for This Company?