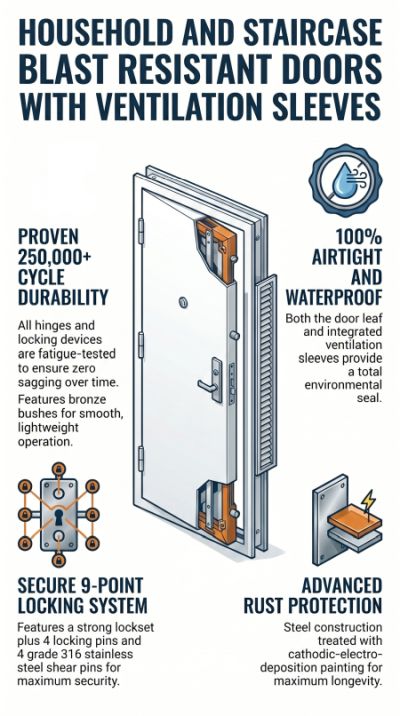

| Yong Tai Loong Pte Ltd (YTL) is an unusual business that you have not heard of until now. It's a 60+ year old in a highly niche, defensible space as one of only five suppliers approved by the HDB to provide civil defense shelter doors and ventilation sleeves. Hong Leong Asia (HLA) has expanded its footprint in the Singapore construction sector through the acquisition of YTL, which has over 100 construction company clients and two manufacturing facilities in Singapore. The five vendors are the second-generation sons of the founder, Yong Teng Long, who built the business from a S$3,000 family workshop in 1958. Beyond those blast-resistant doors, YTL also manufactures fire-rated steel doors, letterboxes, and refuse chute hoppers—items essential to every HDB unit. |

Analysts from DBS Group and UOB Kay Hian are bullish, driven by the acquisition’s strategic fit within a multi-year HDB construction upcycle.

And the deal is priced not only attractively at a 4.3x–4.5x PE multiple but it's delivering a boost right away to HLA's bottomline.

"The deal is immediately accretive with pro forma 2025 EPS rising by 18.6% from S$0.1508 to S$0.1789, excluding one-off items," says UOB Kay Hian analyst Adrian Loh.

The current share price ($3.40) of HLA offers a margin of safety compared to the $3.90-$4.90 range of analysts' target prices.

|

Metric |

UOB Kay Hian |

DBS Group Research |

|

Rating |

BUY (Maintained) |

BUY (Reiterated) |

|

Target Price |

S$4.90 |

S$3.90 |

|

Valuation Method |

SOTP: 15x PE for Powertrain; 8.4x EBITDA for Building Materials |

SOTP: (i) 15x P/E for stake in China Yuchai (ii) 12x P/E for building materials division, (iii) market value for c.20% stake in BRC Asia and (iv) net-cash position. |

| The Bull Case (Positives) |

-

High Revenue Visibility: Singapore’s HDB construction upcycle, targeting 19,600 units in 2026 alone, provides a captive market for YTL's products.

-

Defensible Niche: "As one of only five HDB-approved shelter suppliers, we see YTL as being in a privileged position that cannot easily be replicated by new entrants," says UOB KH's Adrian Loh.

-

Strong Cash Position: Even after the S$90.7m cash deal, HLA maintains a healthy net cash position (S$1.00/share net cash according to UOBKH).

-

Upcoming Catalyst: The potential Hong Kong IPO of HLA's marine and genset power unit (Guangxi Yuchai Marine and Genset Power) in 2026 could unlock further shareholder value.

| The Bear Case (Risks) |

-

Goodwill Impairment Risk: The deal created S$56.3m in goodwill; if the Singapore construction sector softens unexpectedly, this could lead to write-downs.

-

Concentration Risk: YTL is heavily reliant on Singapore’s HDB projects.

-

NTA Dilution: "The main risks lie in the premium valuation paid, and the reliance on continued strength in Singapore's construction cycle to support growth and justify the goodwill created," says DBS analyst Dale Lai. The NTA dilution is 5.7%.

"One item worth watching in the future is the large goodwill of S$56.3m (given that YTL’s net tangible assets was S$34.4m as at end-25) which could be impaired if the construction industry softens." "One item worth watching in the future is the large goodwill of S$56.3m (given that YTL’s net tangible assets was S$34.4m as at end-25) which could be impaired if the construction industry softens."-- Adrian Loh, UOB Kay Hian |

What’s priced in?

Analysts agree that the acquisition is a low-risk "bolt-on" because HLA is retaining the full YTL management team for at least 6–12 months.

For the high target ($4.90) to be hit, the 2026 IPO of Guangxi Yuchai Marine and Genset Power unit needs to happen.

Conversely, a spike in construction costs or interest rates, which could eat into the margins of the debt-funded portion of this acquisition, remains the main headwind.

HLA trades at a 2027 PE of 15.5x–16.0x. |