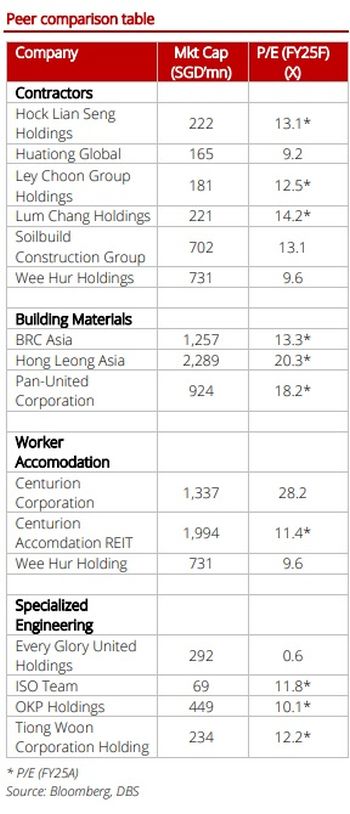

| Singapore’s construction sector has transformed into a rare bright spot for the local equity market, as a wave of multi-billion dollar infrastructure projects and housing rollouts fuels a "supercharged" multi-year boom. The rally in construction-related stocks is thus no accident, matching the sight of towering cranes dominating Singapore's skyline.

In its 2 March report titled "From Backlog to Breakout", DBS Group Research describes the construction industry as entering a "multi-year super-cycle". The report says "building activity will be lifted by mega projects such as Changi Airport Terminal 5, Tuas Port, North-South Corridor, Marina Bay Sands, and Resorts World Sentosa, along with substantial housing rollout, both public and private". |

DBS further emphasizes that "order book visibility at multi-year highs... providing earnings visibility stretching into 2027-2029 for several contractors".

DBS further emphasizes that "order book visibility at multi-year highs... providing earnings visibility stretching into 2027-2029 for several contractors".

While SGX-listed construction stocks have enjoyed a significant rerating, a curious valuation anomaly persists for a cluster of Singapore-based construction firms -- these are listed on the Hong Kong Stock Exchange.

They trade at levels (3-5X PE versus 10-12 for their SGX-listed peers) and are buoyed by net cash levels that suggest the market is quite blind to the "supercharged" demand back home.

| The HKSE "Laggards" |

Despite having order books and profits that rival or exceed their local peers, companies like HPC Holdings, Chuan Holdings, CTR Holdings, and Kwan Yong remain stuck in a deep valuation discount.

• HPC Holdings (1742.HK): In its FY25 results released in Jan 2026, HPC reported a strong recovery -- from a net loss to S$7.7 million in core profit (excluding a bargain purchase gain of S$27.6 million from the purchase of an asset).

Its project pipeline amounted to S$1.37 billion as of end-Oct 2025 covering pharmaceutical buildings (XDC/STA Pharmaceutical), specialized food processing plants, and essential utilities (PSA maintenance base, SP Group substations), etc. HPC Building at 7, Kung Chong Road in the Redhill area serves as HPC's HQ.

HPC Building at 7, Kung Chong Road in the Redhill area serves as HPC's HQ.

• Chuan Holdings (1420.HK): A leader in earthworks, Chuan saw its profit grow 160% to S$6.2 million in 1HFY25 as it continues to build on a S$453 million order book as at end-June 2025.

Like its peers, Chuan’s gross profit margin has been rising (likely with the end of projects hit by a surge in costs during and post-pandemic) to hit 19.1% in 1HFY25, up from 10.9% in 1HFY24.

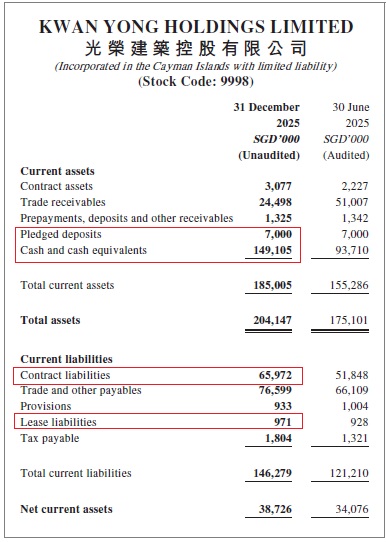

• Kwan Yong (9998.HK): A stark example of growth-valuation mismatch, Kwan Yong's net profit for 1HFY26 (ended Dec 2025) jumped 250% to S$6.9 million and has net cash exceeding its market cap (see table).

It was sitting on an order book as at end-Dec 2025 of over S$715 million, heavily weighted toward government projects such as schools and nursing homes.  Kwan Yong's projects are mainly government ones, including educational institutions.

Kwan Yong's projects are mainly government ones, including educational institutions.

• CTR Holdings (1416.HK): This is another case where its net cash exceeds its market cap (see table).

CTR is involved in Singapore public sector infrastructure, including structural engineering and wet architectural works for hospitals and MRT-related works, which are multi-year engagements.

Its order book stands at S$386 million.

Net profit of S$6.9 million for 1HFY26 (ending Aug 2025) was more than double the previous S$3.2 million.

|

Company |

Stock price (HK$) |

Market Cap (S$) |

Net Cash* |

Order Book** |

P/E Ratio |

|

HPC Holdings |

0.225 |

$59M |

$49M |

$1.37B |

7.7x core; 1.3x |

|

Kwan Yong Holdings |

0.50 |

$65M |

$88M |

$715M |

5.0x |

|

CTR Holdings |

0.177 |

$40M |

$67M |

$386M |

3.5x |

|

Chuan Holding |

0.29 |

$60M |

($22M) |

$453M |

4.8x |

|

*Excludes contract liabilities, which are advances from clients at last reported period |

|||||

Cash on Kwan Yong's balance sheet, with zero debt. (Not shown in above table: non-current lease liabilities of S$1.65 million).

Cash on Kwan Yong's balance sheet, with zero debt. (Not shown in above table: non-current lease liabilities of S$1.65 million).

The above tables are a snapshot -- in the case of HPC and Kwan Yong, the data are recent (as reported by the companies in Jan and Feb 2026, respectively) but the other two companies (Chuan and CTR) are based on announcements several months ago.

Here's the schedule for the next corporate updates, with Chuan's due in a few weeks:

|

Company |

Last reported period |

Next results announcement |

|

HPC Holdings |

FY25 (ended 31 Oct ’25) |

July 2026 |

|

Kwan Yong Holdings |

1HFY26 (ended 31 Dec ’25) |

Aug 2026 |

|

CTR Holdings |

1HFY26 (ended 31 Aug ‘25) |

May 2026 |

|

Chuan Holdings |

1HFY25 (ended 30 June ‘25) |

Mar 2026 |

The reasons for this laggard performance are likely twofold: liquidity and market bias. |

→ See also: Overweight Stocks on Construction Wave, says Broker. One stock is lagging way behind

→ See also: Overweight Stocks on Construction Wave, says Broker. One stock is lagging way behind