• CSE Global stock ($1.32, +184% in the past 1 year), a Singapore-based systems integrator, has undergone a significant strategic shift, with data centres in the US now emerging as its dominant growth engine. It was once primarily recognized for its contributions to the Energy and Infrastructure sectors. • With the US being the world's largest (with reportedly 5,500 data centres, or 10X more than the closest peer) and most advanced data center market, CSE has clinched a pipeline of US$1.5 billion worth of work from Amazon over the next 5 years. • CSE, in which Temasek Holdings holds the No.1 stake (~23%), is engaged in projects that enhance electrical infrastructure, which includes working on substations, switchgear, switchboards, and transformers. These projects are crucial as power needs increase. • With this being a massive multi-year upcycle, analysts are bullish on CSE profit growth for years to come, following the company's recent reported strong FY25 net profit of S$37.5m.  Electrification segment accounted for S$462 m of the end-HFY25 orderbook. The other segments: Automation (S$143 m), Communication (S$105 m). Electrification segment accounted for S$462 m of the end-HFY25 orderbook. The other segments: Automation (S$143 m), Communication (S$105 m).Read excerpts of CGS International's report below .... |

Excerpts from CGS International report

Analysts: TAN Jie Hui & LIM Siew Khee

■ Maintain Add with unchanged TP of S$1.50 as we expect CSE to deliver c.22% p.a. FY26-28F EPS growth despite a high FY25 base |

|||||

"We participate in the data center market through two segments, the primary segment is electrification -- that is AWS. We also have partners that we do for their critical communications, where we work with three hyperscalers. For electrification currently, we work with one. We are working on getting qualification on the second one." -- Lim Boon Kheng, CEO, CSE Global, at FY25 results briefing. |

| FY25 earnings beat on better-than-expected cost discipline and tax |

CSE posted FY25 net profit of S$37.5m, up 42% yoy, beating our/Bloomberg consensus estimates at 110%/108%, fueled by lower-than-expected admin costs and tax savings.

Revenue rose 13% yoy to S$969m, driven by the electrification segment (+17% yoy) on major US DC and LNG contracts, and the communication segment (+13% yoy) from newly acquired subsidiaries.

EBITDA margin fell c.1% pt across key segments due to front-loaded costs, project delays and one-off write-offs.

CSE declared a higher final dividend of 1.46 Scts, bringing full-year DPS to 2.60 Scts (+8% yoy), in line with its payout target of ≥50%.

| Margin improvement expected in FY26F as front-loaded costs ease |

Key types of electrification projects by CSEDuring the FY25 analyst briefing, management said some elevated operating costs will persist into FY26F given scaling requirements and higher absolute activity levels.

Key types of electrification projects by CSEDuring the FY25 analyst briefing, management said some elevated operating costs will persist into FY26F given scaling requirements and higher absolute activity levels.

However, FY25 likely captured the bulk of one-off start-up costs, with FY26F expected to benefit from better EBITDA and net margins as revenue increases.

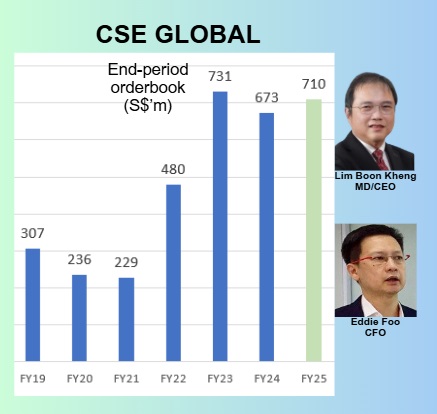

We expect electrification revenue growth in FY26F to outpace FY25’s +17% yoy, supported by a record-high electrification order intake of S$593m and a strong order book of S$462m.

| AWS alliance anchors FY26F growth; CSE aims to expand DC reach |

Amazon Web Services (AWS, AMZN US, NR, CP: US$208) will anchor CSE’s FY26F growth under a five-year, S$1.5bn alliance, with the new 241k sqft Champion facility tripling existing AWS capacity, positioning CSE for multi-year volume ramp-up as production expands, in our view.

Beyond AWS, CSE said during its FY25 analyst briefing that it seeks to broaden its hyperscaler footprint across electrification and communication, supported by expanded land, manpower and inventory.

The group is also exploring M&A in the US and Australia for communication to deepen geographic reach and enhance flow revenue.

We adjust FY26F/FY27F EPS by +2%/0% on higher revenue recognition from the existing orderbook for FY26F.

Our TP remains at S$1.50, based on 19x FY27F P/E (+1 s.d. above 10-year mean). |

→ See full report here.

→ See full report here.

→ Read about another data centre play: ISDN: 1H25 Core Profit Jumps 35%, Powering Ahead with Automation and Hydropower