|

Singapore’s construction landscape is undergoing a powerful infrastructure upcycle and construction stocks are having their time in the sun. A sector update from UOB Kay Hian offers its top 3 picks and a slew of companies whose orderbooks are outsized relative to annual revenue. |

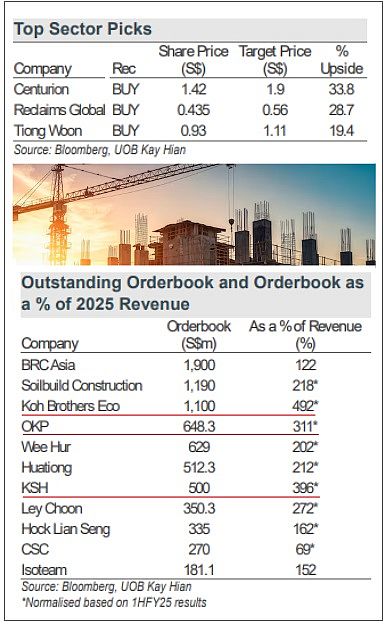

| UOB KH’s Top 3 Stock Picks |

The three that offer the best blend of valuation upside and operational strength are:

1. Centurion – Target: S$1.90

Offering a 33.8% upside from its recent price of S$1.42, Centurion is a key player in specialized accommodation for the increased labor demand required to execute Singapore’s infrastructure pipeline.

Offering a 33.8% upside from its recent price of S$1.42, Centurion is a key player in specialized accommodation for the increased labor demand required to execute Singapore’s infrastructure pipeline.

2. Reclaims Global – Target: S$0.56

Positioned at the intersection of construction and recycling, Reclaims Global offers a 28.7% upside.

On a 2026 PE of 12.1x, it is recognized for its role in the "green" construction cycle, which is becoming increasingly important as Singapore focuses on sustainable development.

3. Tiong Woon – Target: S$1.11

Recently upgraded to BUY, Tiong Woon is enjoying margin recovery.

After gross margins moderated to 38% in FY25 due to equipment cross-hiring costs, the company is expected to see margins return to over 40% as project scheduling normalizes.

| Visibility is King: Top 3 Companies by Orderbook vs. Revenue |

As an orderbook represents revenue visibility, a high "Orderbook as a % of Revenue" indicates that a company has secured years of work relative to its current size.

According to UOB's screening, these 3 have the highest visibility:

|

Company |

Orderbook Value (S$m) |

Orderbook as % of Revenue |

|

Koh Brothers Eco |

492% |

|

|

KSH |

500 |

396% |

|

OKP |

648.3 |

311% |

1. Koh Brothers Eco

Leading the pack with a staggering 492%, Koh Brothers Eco has nearly five years of revenue equivalent sitting in its backlog.

This is largely driven by its involvement in major public sector water and infrastructure projects and includes 68.14% subsidiary Oiltek's ~S$110 million orderbook.

Koh Eco's stake in Oiltek accounts for nearly 85% of its S$236 million market value (based on 8.4 cent stock price). Koh Eco has a track record of delivering major projects as illustrated above.

Koh Eco has a track record of delivering major projects as illustrated above.

At an implied value of just S$36 million for its core construction and civil engineering business, the market is valuing the core business at 0.03x its orderbook.

This is exceptionally low, even for the construction sector, so any improvement in construction margins could lead to a massive re-rating of Koh Eco's stock.

2. KSH

Beyond pure construction, the group benefits from a diversified portfolio that includes property development and investments.

It is trading at a 2025 PE of 11.3x and a 2026 PE of 9.2x. Dividend yield is 5.3%.

3. OKP

For a contractor specializing in transport-related public works, this high percentage reflects the government's continued commitment to expanding Singapore's MRT and road networks.

OKP has a market cap of S$400 million and trades at a 2025 PE of 10x with a strong orderbook of S$648.3 million.

Dividend yield is 2%.

See the UOB KH report here.