| So, small- and mid-caps have been rallying this year. They are not the only ones. Many of the bigger caps such as Singapore property developers has also had a good run but they are far from running out of steam. According to the latest report from DBS Group Research, 2026 is shaping up to be "Act 2" of a re-rating cycle. We're talking about meaningful room for re-rating for property stocks, even after the 50% share price surge in 2025. |

Recent prices: UOL : $8.38 | CDL : $7.18 | GuocoLand : $2.02 | Fraser : $1.12

Recent prices: UOL : $8.38 | CDL : $7.18 | GuocoLand : $2.02 | Fraser : $1.12

Why the optimism?

Well, developers are still trading at deep-value levels—a mere 0.6x forward Price-to-Book (P/B) and a hefty 55% discount to their Revalued Net Asset Value (RNAV), according to DBS analysts Derek Tan and Tabitha Foo.

The Big Value Unlock: Lower Rates and Creative Restructuring

A lower interest rate environment, coupled with buoyant capital markets, is setting the perfect stage for developers to boost returns and capital efficiency.

The main game changer is restructuring.

For developers sitting on mature, stabilised assets (think commercial buildings or investment properties), the smart money is now looking at ways to monetise these assets, either by spinning them off into a REIT or restructuring the whole thing into a stapled security (developer plus REIT).

DBS highlights the example of accommodation asset owner Centurion Corporation, which saw its share price rocket by over 80% following the announcement of its potential REIT listing, dramatically narrowing its RNAV discount.

Developers like UOL, GUOL, and others with substantial hotels and investment properties could follow this path.

Beyond financial engineering, redevelopments are huge value boosters.

UOL's plans for Marina Square, for example, could potentially lift the development's value by 3.5 to 4.5 times, says DBS.

CDL is also busy with major redevelopments at Union Square and Newport Plaza.

Plus, we’re seeing continuous portfolio recycling, where companies shed non-core assets to "clean up" the balance sheet, with proceeds often used to return capital to shareholders.

Specific Upside Triggers for Top Picks

|

Developer |

Key Upside Initiatives/Reasons for Re-rating |

|

UOL |

Driving major value creation through the planned redevelopment of Marina Square. Recently raised its regular dividend (from 15 cts to 18 cts). Has a robust launch pipeline, including the massive Thomson View project (1,240 units) slated for 2026. Holds significant investment properties that could be monetised via a REIT. |

|

GUOL |

Also recently raised its regular dividend (from 6 cts to 7 cts). Has significant investment properties and hotels that present a strong opportunity for value unlocking through REIT/stapled structure. Robust launch pipeline includes the River Valley Green (Parcel B) project in 1Q26 and Tengah Garden Avenue in 3Q26. |

|

CDL |

Actively pursuing major redevelopment projects like Union Square and Newport Plaza, with Delfi Orchard also a mid-term possibility. Accelerated its divestment pace in 2025 (contracted divestments over S$1.5bn). Special dividend potential is high, following the significant gain from the South Beach divestment. Launch pipeline includes Lakeside Drive and two new Executive Condominium projects. |

Show Me the Money: Shareholder Returns

DBS analyts say another big signal that 2026 is the year for developers is their increasingly proactive stance on rewarding shareholders.

Developers haven't typically been viewed as dividend plays, but that’s changing. UOL raised its dividend from 15 cts to 18 cts per share, and GUOL hiked theirs from 6 cts to 7 cts.

What about special dividends? They could be on the cards for companies like CDL, especially after the huge gains from their South Beach divestment. Returning capital is a core part of this structural re-rating.

Finally, while residential sales volumes might ease in 2026 compared to the robust 2025 (when we saw around 11,000 primary sales units), the strong launch pipeline from DBS' picks ensures solid earnings visibility.

UOL, GUOL, and CDL each have about 1,500 units in their respective pipelines, which is set to boost RNAV and ensure strong pre-sales performance.

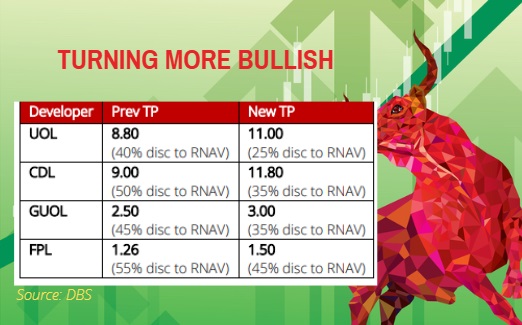

Thus, DBS is raising its target prices across the board, narrowing the discounts by 10 to 15 percentage points.