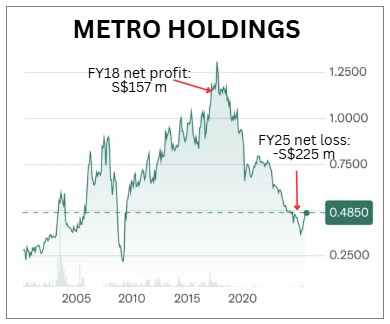

Metro Holdings, once Singapore's premier department store chain with 11 outlets at its early 2000s peak, has significantly contracted its retail footprint, now operating just two stores (Metro Paragon and Metro Causeway Point). Its property concentration in China, in recent years, has not brought relief as the country's economy faltered.  Thus Metro stock has declined from $1.20 in 2017 to 46 cents rerently. Thus Metro stock has declined from $1.20 in 2017 to 46 cents rerently.But is Metro shaping up as a classic privatisation candidate? It has a highly concentrated ownership, recent share accumulation by an insider, and a steep valuation discount.

This was noted in a 1 Sept initiation report (110 pages!) from FPA Financial, a wealth management company. |

| Background: Ownership Changes, Strategic Moves |

Metro Holdings operates principally in property investment & development and retail.

The FPA Financial report gave reasons for its privatisation speculation:

(1) As of 28 August 2025, Ong Sek Hian (Wang ShiXian), one of the founder’s grandchildren, holds 35.7% total interest in Metro. (1) As of 28 August 2025, Ong Sek Hian (Wang ShiXian), one of the founder’s grandchildren, holds 35.7% total interest in Metro.Ong Sek Hian, who is also a non-executive director of Metro, and several Ong family members hold their stake via Dynamic Holdings, Leroy Singapore, and Eng Kuan Company;

(2) the total interest of Ong Sek Hian rose by 2,633,600 shares from 13 to 28 August 2025. A total of S$1.1 million was paid at an average of S$0.433 per share; and (3) Metro’s P/B multiple is 0.32x. |

||||||||||

These factors open the door for a privatisation scenario, reminiscent of past moves by legacy family-controlled Singapore companies.

| Valuation Gaps: Discounts and Peer Analysis |

Metro’s share price of S$0.445 translates into a Price-to-Book (P/B) multiple of just 0.32x, which is approximately 68% below stated NAV.

"Metro is currently trading at a P/B multiple of 0.32x, which is lower than the peer average P/B of 0.78x. This suggests that Metro is undervalued at its current share price. Adopting a relative valuation approach, we estimate a target price of S$1.100 if Metro is to trade at the peer average P/B of 0.78x" -- FPA Financial |

The report notes that this undervaluation is stark compared with peer averages; for context, selected property and retail peers trade at an average P/B multiple of 0.78x.

However, as the analyst notes, “Metro’s P/B multiple may be lower than the peer average as the market may be expecting further fair value losses in Metro’s interest in Chinese properties (as compared with Metro’s peers).”

This caution is warranted, especially with the company recording substantial impairments and China exposure risks: “Metro Group’s exposure to the PRC has been reduced from 76% (2010) to 45% (2025)… China accounted for 92.0% of Metro’s loss from operations before taxation (S$219.8 million) in FY2025”.

| Privatisation Potential: Price Premiums and Feasibility |

The likelihood and pricing of a privatisation hinge on precedent.

According to the report, “the average price premium of the selected privatisation offers was 25.1%.”

Applying this premium to Metro’s last traded price implies a potential offer of S$0.557 per share, representing a 25.1% uplift.

The analyst adds: “Any privatisation offer may need to have a price premium of 25.1% from the current share price of S$0.445 to have a chance to be successful. Thus, we estimate our overall target price to be S$0.557”.

Key catalysts for a more favourable share price, beyond privatisation, include a write-back of large fair value losses should the Chinese property market recover, and possible corporate action by the family shareholder.

|

→ The full FPA Financial report is here. → The full FPA Financial report is here.→ See another stock with privatisation potential as the parent owns 88% already: MANDARIN ORIENTAL: Parent Company's Grip Tightens on Undervalued SGX Gem. Is Privatisation On The Cards? |