• Singapore's construction industry is booming yet one long-time builder, KSH Holdings, may have been overlooked by the market. Lim & Tan Securities has highlighted the stock's potential upside following its FY25 (ended March 2025) results that on the surface were dismal. • Founded in 1979 and SGX-listed since 2007, KSH (market cap: $127 million, stock price: 23 cents) is into construction, property development and investment. Its operations span two core segments—general building and civil engineering in Singapore and Malaysia, and property development, investment and management in China. • It reported a net loss of $5.9 million for FY25, hit by a double whammy:

• For the current FY26, Lim & Tan Securities is forecasting $15-20 million net profit. And a higher dividend payout, resulting in a 6.4% yield. • Read more below ... |

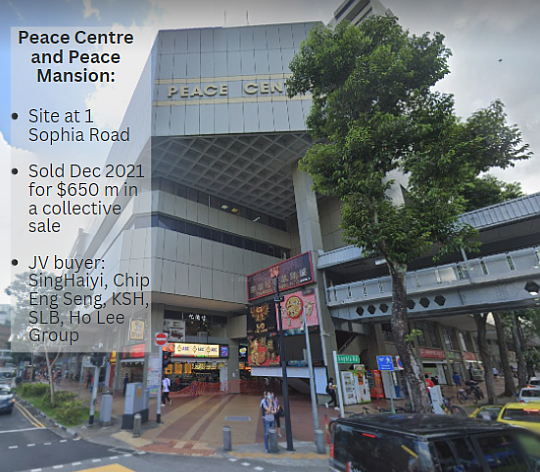

KSH is a JV partner in the purchase and redevelopment of Peace Centre/Peace Mansion. It is currently marketed as One Sophia / The Collective at One Sophia.

KSH is a JV partner in the purchase and redevelopment of Peace Centre/Peace Mansion. It is currently marketed as One Sophia / The Collective at One Sophia.

Excerpts from Lim & Tan Securities report

Conclusion and Recommendation:

If not for fair value losses of $7-8mln (commercial investment property in China) in 2H ended March’25, KSH would have turned around with a 6-month profit of $7-8mln, thanks to the recovery of their construction business and contributions from their development projects.

| Positive trends |

"We continue to benefit from favourable industry prospects underpinned by our strong track record and extensive experience.” -- KSH Holdings MD Choo Chee Onn |

Looking ahead, we understand that management is targeting to rebuild their order book from $230mln to more than $500mln on the back of the resurgence in construction activities in Singapore as the government uses pump priming measures to offset external macro challenges.

KSH’s development projects have recorded pre-sales of $160mln and these will start contributions in the new year ahead, helping to contribute to bottom-line.

Overall, we believe that KSH will see a nice boost of 25-30% in sales in FY ending March’26 to about $230mln while bottom-line will turnaround to $15-20mln range with margins reverting back to historical means.

Dividend payments which have recovered 25% to 1.25 cents last year is likely to rise further to 1.5 cents (50% payout ratio), translating to an attractive forward yield of 6.4%.

|

With a strong net cash position of $50-60mln and undemanding P/B ratio of 0.46x and forward PE of 7x-9x (at 23.5 cents, Market Cap is $135mln) we maintain an “Accumulate” rating on KSH.

Downside is likely limited given its continued share buy back program where the company has bought back 10.868mln shares around the 20 cents level, accounting for just under 20% of its allowable total buy back volume of 55.2mln shares. |

||||||||||||||||||

KSH's Powerpoint deck for FY25 is here.