• Will Wee Hur Holdings, a Singapore-based property developer and operator of purpose built workers accommodation, feel the sting of Trump’s new US tariffs? Unlikely. Its focus is firmly on projects, especially in property development and workers’ accommodation than trading with the US. • A key project currently is the massive Pioneer Lodge in Jurong West, which offers 10,500 beds for foreign workers. That's Wee Hur's second workers accommodation after Tuas View (15,744 beds). Wee Hur is enjoying very favourable dormitory rates because of a shortage of dormitories versus demand.  Pioneer Lodge will open in 2 phases in 2025. It comprises: 4 blocks of 4-storey workers' dormitories and 4 blocks of 9-storey workers' dormitories. There is 1 block of 2 storeys with amenities such as multipurpose rooms, gymnasiums as well as minimarts and canteens. Pioneer Lodge will open in 2 phases in 2025. It comprises: 4 blocks of 4-storey workers' dormitories and 4 blocks of 9-storey workers' dormitories. There is 1 block of 2 storeys with amenities such as multipurpose rooms, gymnasiums as well as minimarts and canteens.• Wee Hur's shares fell 7.7% (from 52 cents to 48 cents) in the past week but that is more tied to general market jitters over the tariffs than anything specific to the company. • On another note, it has pocketed a cool S$300 million by selling off a big chunk of its student accommodation business in Australia. Shareholders are in for a treat: 7.8 cents / share (0.8 cent ordinary dividend + 7 cent special dividend) which translates into a 16.25% yield. Read more below .... |

Excerpts from Phillip Securities report

Analyst: Ben Yik

| The wait is over - special dividends are here |

| ▪ On 1 April 2025, Wee Hur announced that the disposal of 37.1% stake in WH PBSA Master Trust (Fund I) has completed (net proceeds ~S$300mn). S$0.07 special dividend per share (~14% dividend yield) was declared and will be paid in May 2025.

▪ Following the disposal, Wee Hur will continue to own 13% of Fund I, its stake valued at ~S$175mn (~38% of market capitalisation). |

||||

Using SOTP, we reduced Fund I’s stake to 13% (prev. 50.1%) as the disposal of 37.1% of Fund I has completed.

With balance sheet strengthened with an expected ~S$122mn net cash post-special dividends, we lowered WACC of workers’ dormitory segment to 9.7% (prev. 13.7%) and raised EV/EBITDA assumption to 7.3x (prev. 3x) to be more in-line with Wee Hur’s FY24 EV/EBITDA of 8.6x.

Fund II’s discount to RNAV assumption is lowered to 40% (prev. 60%) to reflect an intent to dispose of the asset, timeline uncertain.

At S$0.62 target price, Wee Hur would be trading at a ~17% discount to its expected NAV per share of S$0.75.

| Key Highlights |

▪ Wee Hur announced S$0.07 of special dividend per share.

The amount was 8% higher than our initial expectations of S$0.065 per share.

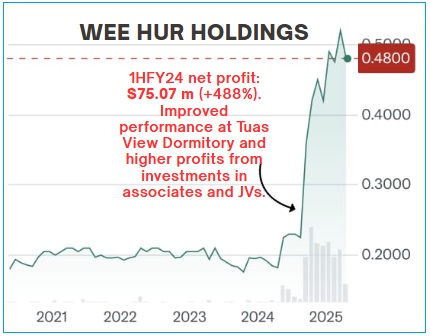

The special dividend represents a dividend yield of ~14%. We are forecasting FY25e dividend yield of 15.5% (inclusive of special dividend). 2H24 saw a net loss of $18.1 m, largely owing to $45 m of items such as fair value adjustments on investment properties and forex losses. Chart: Yahoo!

2H24 saw a net loss of $18.1 m, largely owing to $45 m of items such as fair value adjustments on investment properties and forex losses. Chart: Yahoo!

▪ Wee Hur received S$300mn in net proceeds and S$37mn in net gains from its PBSA disposal.

The substantial net proceeds (~65% of its market capitalization) is expected to boost its balance sheet from a net debt of S$114mn to an expected net cash of ~S$122mn after giving out special dividends.

The gain on sale is expected to boost Wee Hur’s NAV per share from S$0.71 to ~S$0.75.

▪ Going forward, Wee Hur still has ~S$232mn worth of assets (~50% of its market cap) to be sold.

Following the transaction, Wee Hur owns 13% of the units in the WH PBSA Master Trust (Fund I), with its stake valued at ~S$175mn (Figure 1).

Wee Hur also owns 30% of Fund II, which holds a 409-bed PBSA asset in Sydney, its stake valued at ~S$57mn.

We believe Wee Hur will eventually implement an exit strategy for these assets, although the timeline is uncertain.

Assuming ~14% of fair value paid out as special dividends as in this case, we expect a possible special dividend of S$0.035 per share (yield: ~7%) from sale of remaining assets.

|

Full report here.

See also: OILTEK: Technical Business Became a Market Darling with a 390% stock surge in 1 year