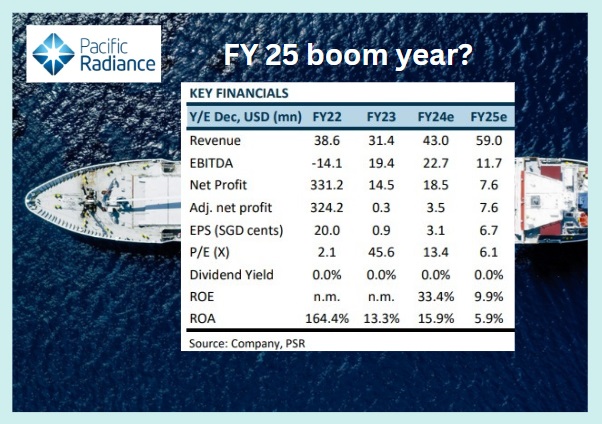

• It's the new year but Maybank Kim Eng's favourite small-mid caps remain the same as they have been for most of 2024 -- CSE, Marco Polo and LHN. Then there's SingPost. SingPost is actually a relatively recent addition, triggered by news of its impending unlocking of the value of its Australian assets. • Marco Polo is Maybank's only pick in the offshore support business but it has good things to say about the industry: "We remain bullish on the O&G supply chain theme, especially on the OSV charterers as demand is still more than supply which should result in higher charter rates and high utilization rates." • So which other OSV plays are not on Maybank's radar? Let's give a shoutout to Nam Cheong and Pacific Radiance. • To get up to speed on Nam Cheong, see: From Debt Restructuring to Big Profits: This company is a nice turnaround story in 2024  A less-familiar story is Pacific Radiance, which has garnered coverage by, first, Phillip Securities, and, recently, CGS International. • In brief, Pacific Radiance is mainly into ship management but is rebuilding its ship ownership business by acquiring vessels. A wild card is its Indonesian associate, Logindo, which emerged from debt restructuring recently and has a fleet of 41 vessels, some of which could be deployed out of Indonesia waters for higher charter rates -- or sold.  • Meanwhile, read excerpts of Maybank Kim Eng's investment case for its top picks of small-mid caps for 2025 ... |

Excerpts of Maybank Kim Eng's report

Analyst: Jarick Seet

| Top picks are SingPost, CSE Global, LHN and Marco Polo Marine |

SingPost – Asset monetisation play  Jarick Seet, analystWith the sale of its Australian business, we believe that the roadmap going forward to return shareholder value is strengthened and shareholders could potentially get up to SGD0.86/share if all its assets are monetised.

Jarick Seet, analystWith the sale of its Australian business, we believe that the roadmap going forward to return shareholder value is strengthened and shareholders could potentially get up to SGD0.86/share if all its assets are monetised.

We think the downside risk is now limited and maintain a conviction BUY on SingPost over its asset monetisation story.

Its key shareholders are also monetising non-core assets to return to its own shareholders.

The recent sacking of the CEO and other senior management following their handling of a whistleblowing case is unlikely to derail the board-driven restructuring strategy of SingPost, in our view.

CSE Global – All stars aligning

With Trump advocating for lower energy prices and boosting production in the US, this may be hugely beneficial for CSE.

While CSE has switched its focus more towards electrification projects, revival of activities in the O&G space may mean all 3 of CSE’s segments are firing, which could potentially propel CSE’s orderbook and profitability further.

As of 9M24, orders from the energy sector declined 3.7% YoY to SGD237m, but this could drastically rebound during the Trump administration.

We remain optimistic about CSE’s prospects and maintain BUY and a TP of SGD0.60.

| Marco Polo Marine – Exciting times ahead Going forward, we reckon that exciting times are just starting for MPM. Its CSOV is 91% completed and should likely start operating by 25 Mar-25. We also expect utilisation for the first 2 years to be close to 95% with average rates of around USD50k/day.  Charter rates are expected to increase by 5-10% next year. The manpower shortage issue has also improved with 3rd party repairs likely to rebound in FY25E. We also expect orders for 1-2 CTV in 2025. We retain our BUY rating and SGD0.08 TP based on 10.5x FY25E P/E. |

LHN Group – Co-living growth FY24 was driven by strong demand for its co-living segment, which achieved a high occupancy rate of 97.5%, coupled with stable rental rates. LHN targets to add about 800 new rooms every year via master lease or selective acquisition. LHN will further expand its co-living portfolio with new developments such as the launch of 48 and 50 Arab Street, the GSM Building at 141 Middle Road and 260 Upper Bukit Timah Road. These properties will add over 250 keys to its current operations. In line with its capital recycling initiative, the group’s 40% associated company recently sold its car park at Bukit Timah Shopping Centre for SGD22m and reinvested in a 50% JV which acquired Wilmar Place at 50 Armenian Street for SGD26.5m that will be operated under its Coliwoo brand. The Group declared a final DPS and special DPS of 1.0 cent each, taking total payout to 3.0 cents, translating into an attractive yield of 7.0%. Our TP of SGDD0.55 is based on 7x FY25E P/E. |

Risks

Key risks remain with geopolitical tensions, especially between the US and China. Any global conflicts could also hinder economic growth which will lead to likely softer demand.

Maybank KE's full report is here.